Merger Model: How It Works, Example & Interview Questions

M&A transactions require a thorough analysis of how merging companies will affect the financial health of the combined business once a deal closes. To do such analysis, bankers use a merger model. It covers standalone forecasts of income statements, total deal costs, transaction structure, and combined financials to find out whether the acquirer ends up in a stronger or weaker financial position than before.

Read on to understand the key components of an M&A merger model, get a step-by-step breakdown of how to build a merger model, and walk through a simple merger model example.

A merger model is a financial tool that analyzes what happens to a buyer's earnings per share (EPS) when it acquires another company. EPS is generally used because it’s a critical profitability metric that measures how much profit each share generates.

Once an M&A deal closes, the acquirer's EPS either goes up or down depending on what it paid, how it funded the deal, and what the combined business earns. The deal is accretive if EPS increases, and dilutive if it falls. The merger model helps determine which outcome the deal produces and why.

Why Is a Merger Model Important for You?

If you're targeting an investment banking role, especially M&A IB divisions, chances of getting questions about merger models during technical interviews are high. Interviewers use them to assess whether you understand why companies acquire, what makes a deal attractive, and how financial decisions translate into shareholder value.

Beyond interviews, merger models are the day-to-day tools IB bankers use to advise clients on live deals. Both buyers and sellers seek advice from M&A bankers when considering a merger or acquisition. So, knowing how to build a merger model and how to interpret what it's telling you is a core skill on the job from day one.

Key Components of a Merger Model

Before building the model, it helps to understand the key components you’ll work with. They include:

Financial Profiles of Both Companies: A key component of a merger model is projected income statements for the acquirer and target. At minimum, the statements must have revenue, operating income, net income, and share count.

Purchase Price and Premium: What the acquirer is paying per share, and at what premium to the target's current share price.

Financing Structure: An idea of how the deal is funded – cash, new debt, newly issued stock, or a mix. The transaction structure determines interest costs, share dilution, and ultimately which direction EPS moves.

Synergies: The expected cost savings and revenue gains from combining the two businesses. Cost synergies are more reliable while revenue synergies are speculative.

Purchase Accounting Adjustments: When a deal closes, the target's assets get revalued. That process creates goodwill and generates incremental depreciation and amortization (D&A) both of which affect the combined financials.

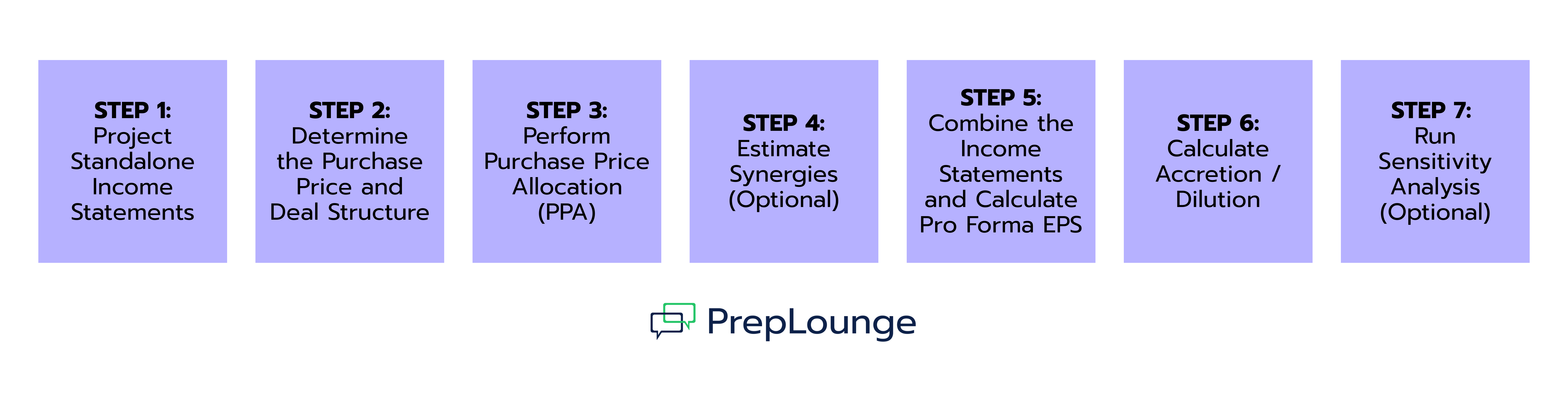

How Does a Merger Model Work? Step-by-step Guide

Here’s how to build a merger model step by step.

STEP 1: Project Standalone Income Statements for Both Companies

You can build a full 3-statement model (income statement, balance sheet, cash flow) but it isn't strictly required. What you must have is the projected income statements for the acquirer and target, ideally covering 3–5 years.

STEP 2: Determine the Purchase Price and Deal Structure

Next, make assumptions about the purchase consideration (buying price). In merger models the purchase price is the equity value, and it tells you how much the buyer needs to raise to buy out the target’s shareholders.

Start by determining the offer price per share. Then multiply that by diluted shares outstanding to get the total equity.

Equity Value = Offer Price Per Share x Target's Diluted Shares Outstanding

Once the purchase price is known, decide how much will be funded with cash, newly issued debt, and newly issued stock. The buyer and the seller must agree on the deal structure or financing mix for the deal to proceed.

STEP 3: Perform Purchase Price Allocation (PPA)

Purchase price allocation (PPA) is an accounting process that breaks down the purchase price to see what the buyer is actually paying for. Start with the target's book value of equity. Then write up its identifiable assets, such as PP&E and intangibles like customer lists or patents, to fair market value.

The gap between the total purchase price and those revalued net assets is goodwill, and it goes onto the consolidated balance sheet post deal. But what matters most for the merger model is the asset write-ups. They generate incremental depreciation and amortization (D&A), which flows through the combined income statement in later steps and directly affects the accretion/dilution result.

STEP 4: Estimate Synergies (Optional)

Another input you may need for the merger model is synergies. That is, the incremental value the deal creates that wouldn't exist for either company alone. There are two main types of synergies:

Cost Synergies: These come from eliminating duplicate headcount, consolidating facilities, and renegotiating supplier contracts.

Revenue Synergies: These come from cross-selling, geographic expansion, or new product access. They're harder to model and slower to materialise.

Simple merger models use a single net synergy number. But detailed ones phase them in over 2–3 years and offset with integration costs like restructuring charges, system migration, and severance.

STEP 5: Combine the Income Statements and Calculate Pro Forma EPS

This is one of the most critical steps in a merger model. Add the buyer's and seller's income statements line by line. That is, Revenue + Revenue, and Expenses + Expenses. Then make the following adjustments to account for the costs of financing the deal:

Add synergies (after tax)

Subtract incremental Depreciation/Amortization (D&A) from PPA write-ups (after tax)

Subtract interest expense on new debt (after tax)

Subtract lost interest income on cash used to fund the deal (after tax)

The result is the pro forma combined net income. That is, the combined net income of both companies after accounting for deal adjustments. Take the acquirer's diluted shares outstanding and add any new shares issued as stock consideration. Then divide the combined net income by the new share count to get pro forma EPS.

Pro forma EPS = Combined Net Income / New Share Count

STEP 6: Calculate Accretion / Dilution

Compare the acquirer's pro forma EPS to its standalone EPS.

Accretion/Dilution = (Pro Forma EPS / Standalone EPS) -1

A positive result means the deal is accretive or the acquirer's EPS increases post-deal. On the other hand, a negative result means it is dilutive or that buyer’s EPS falls. Dilution isn't automatically a bad deal, but it requires a stronger strategic justification, since the market tends to react negatively.

STEP 7: Run Sensitivity Analysis (Optional)

Lastly, you can build sensitivity tables that show how accretion/dilution changes under different merger model assumptions. Bankers mostly vary the purchase price premium and the level of synergies. You can also sensitise for % cash vs. stock consideration, interest rates, or revenue growth assumptions.

Merger Model vs. Accretion/Dilution Analysis

These terms are often used interchangeably, but they're not exactly the same thing. A merger model is the comprehensive M&A valuation tool used to combine the financial statements of two companies, analyze their financial profiles, and forecast the financial impact of a transaction.

But of all the things a merger model reveals, the question that tends to dominate is how the deal affects the acquirer's Earnings Per Share (EPS). To find out, bankers use an accretion/dilution analysis, which is the specific test that measures if EPS will go up (accrete) or down (dilute).

Accretion vs. Dilution in a Merger Model

Once you have a complete merger model, you can tell whether a deal is accretive or dilutive. But to ace IB interviews, you need to be able to explain the why behind that result.

Funding mix is one of the major factors. An all-cash or all-debt deal doesn't increase the share count, so EPS only absorbs the interest cost. An all-stock deal issues new shares, which increases the share count and puts immediate downward pressure on EPS. But whether the target's added earnings offset that depends on relative valuations. If the acquirer trades at a higher P/E than the target, its stock is more expensive, so it issues fewer shares to fund the transaction, and the deal still tends to be accretive.

Another factor is purchase premium, and it typically works against accretion. The more a buyer overpays, the harder it is for the target's earnings to compensate. Then there’s synergies which work in favour of accretion. Cost savings and revenue gains flow directly into combined net income, and can turn an otherwise dilutive deal accretive.

Most importantly, it’s worth noting that accretion/dilution measures EPS impact, not value creation. So, a deal can be accretive and still be a terrible deal. For instance, if the acquirer paid a massive premium for a business whose earnings are about to decline. Likewise, a dilutive deal can still be a good deal if there's justification like a target that brings strategic assets — technology, market access, talent — whose value doesn't yet show up in current earnings.

Merger Model Example

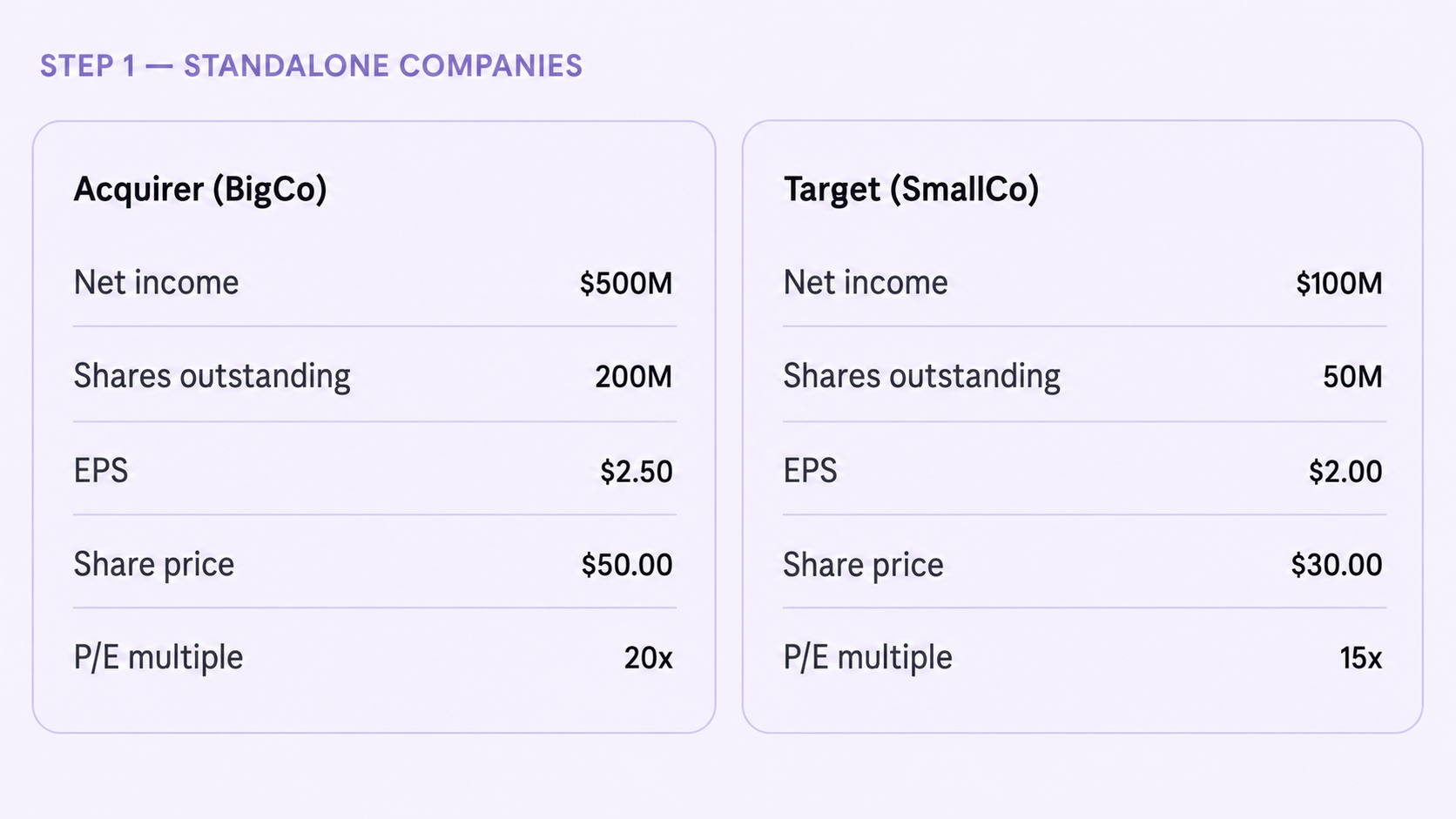

To see how all the merger model steps connect, let's walk through a simple merger model example. BigCo is the acquirer buying SmallCo, the target. The first step is to get the standalone forecasts of each company’s income statement.

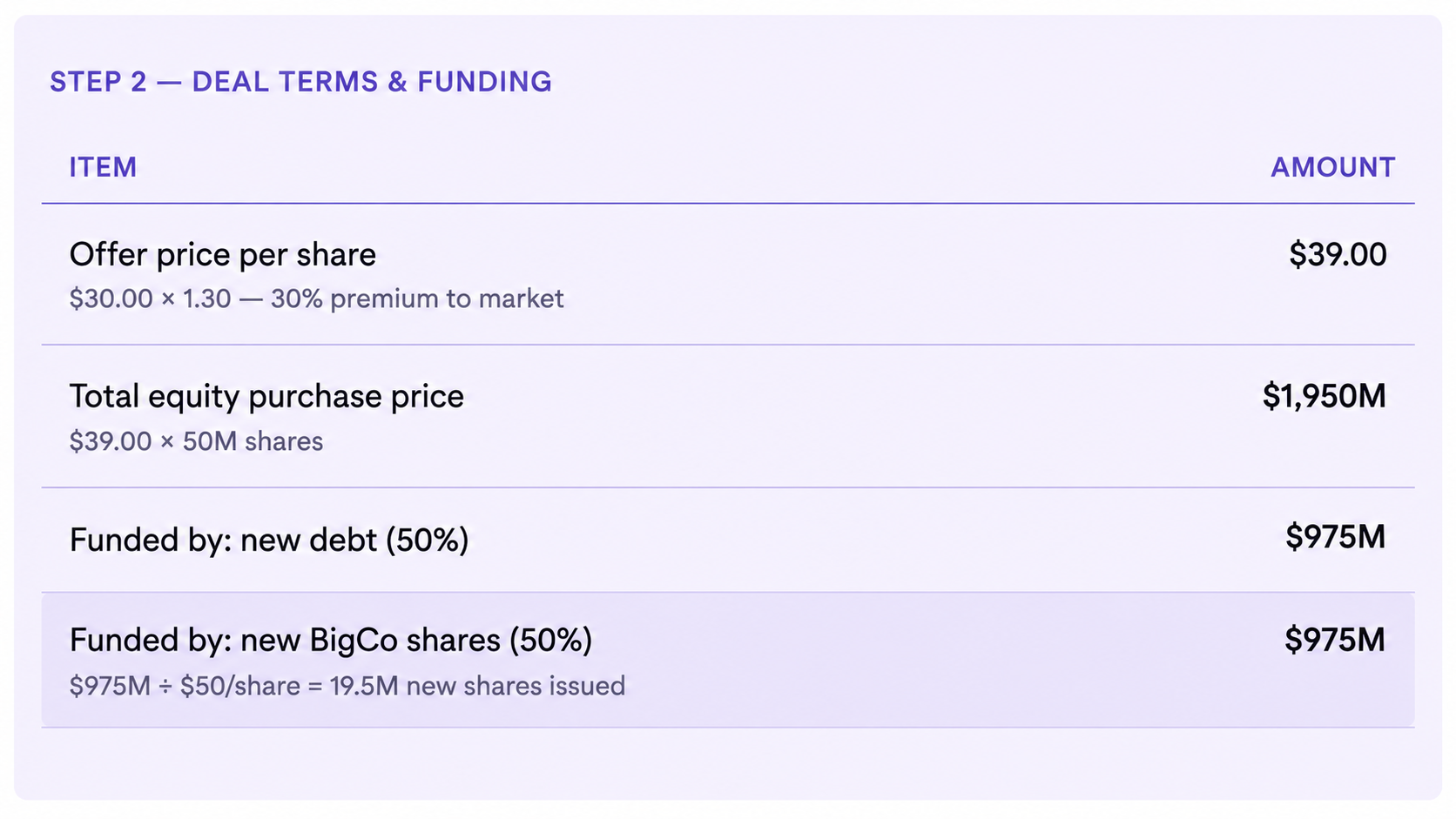

Then determine the deal terms and structure. BigCo offers $39 per share which is a 30% premium to SmallCo's actual $30 share price and the number of outstanding shares is 50M. Hence, the total purchase price is $1,950M and the acquirer funds the deal half in new debt, half in newly issued BigCo shares. The debt costs 5% annually and BigCo pays a 25% tax rate.

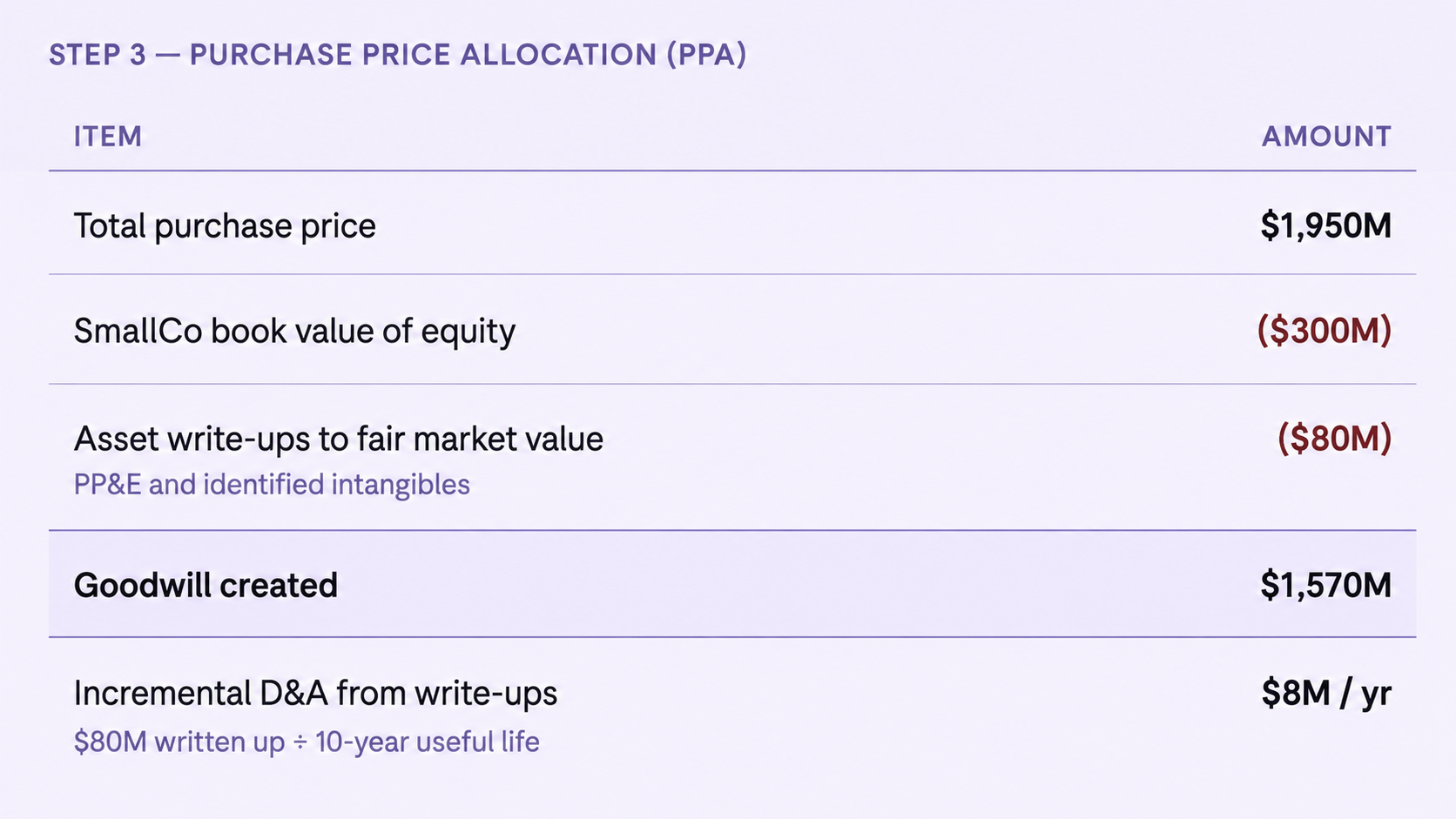

For the PPA step, SmallCo's book value is $300M. After writing up identifiable assets by $80M to fair market value, $1,570M is left over as goodwill. The write-ups also generate $8M in incremental D&A annually, which will reduce combined pre-tax income.

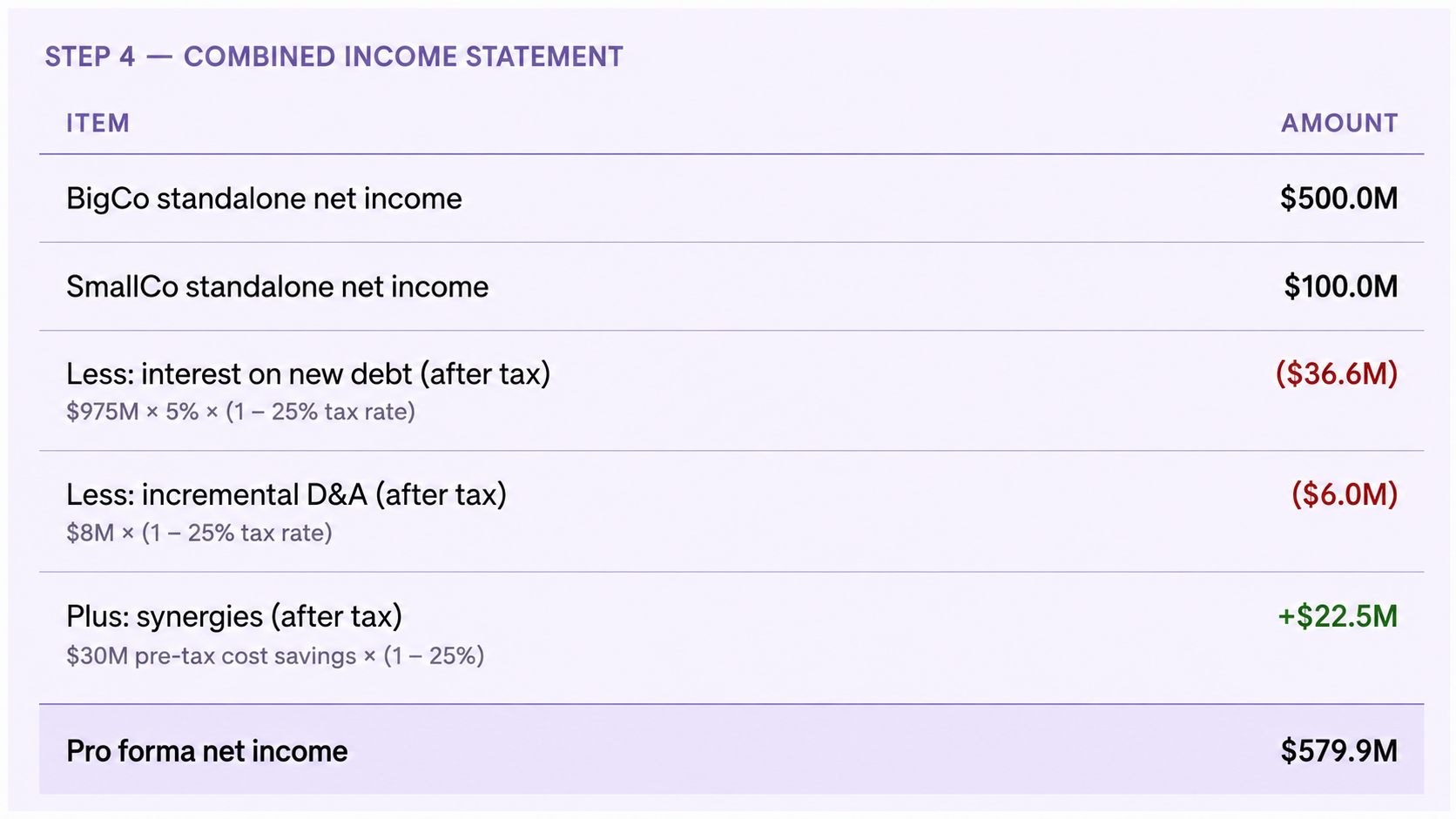

Now add both companies' net incomes together, then apply the deal's three main adjustments:

Subtract after-tax interest on the new debt (−$36.6M),

Subtract after-tax incremental D&A (−$6.0M)

Add after-tax synergies (+$22.5M).

The result is a pro forma net income of $579.9M.

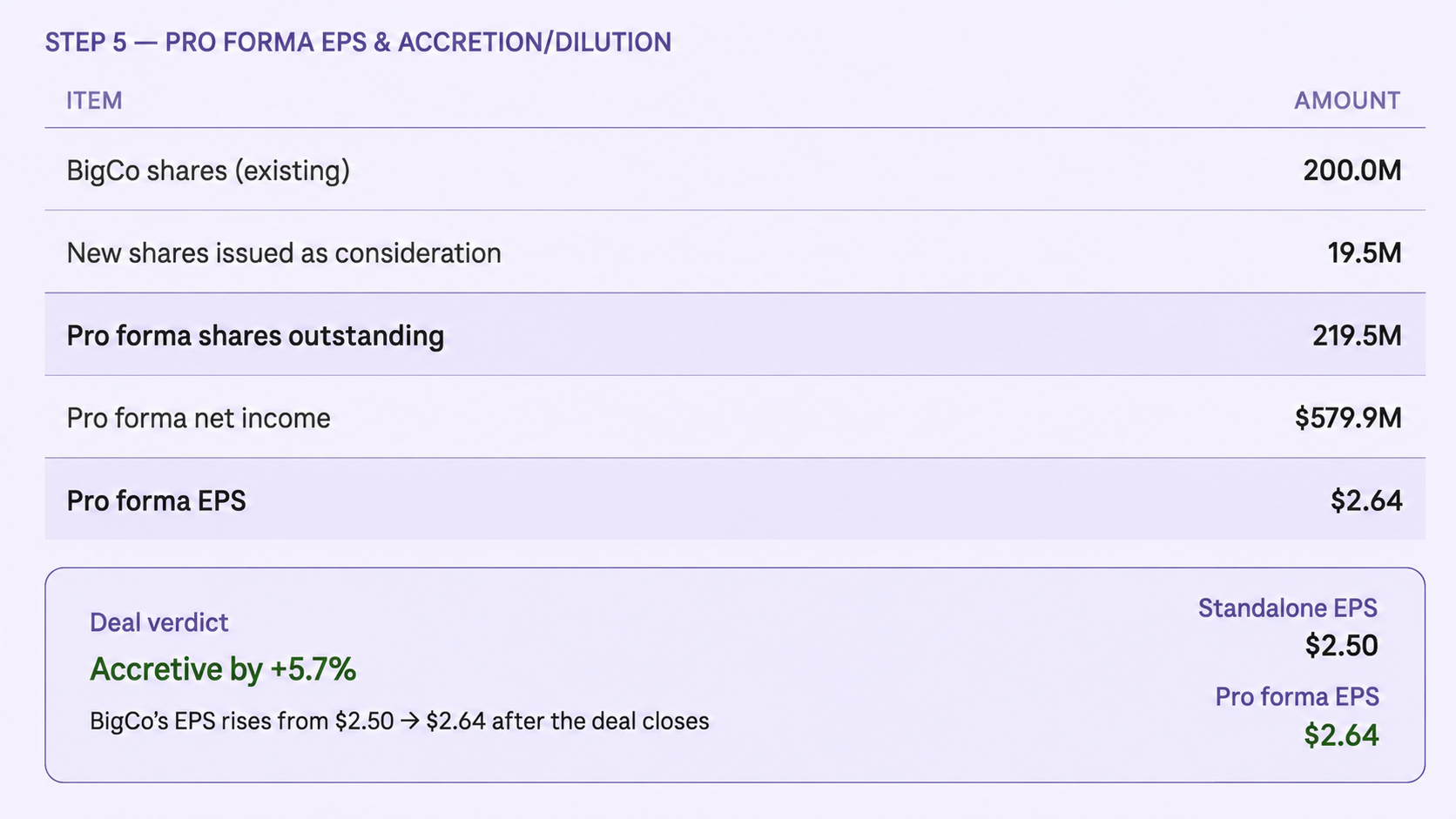

Then calculate pro forma EPS. BigCo issued 19.5M new shares as stock consideration, bringing total shares to 219.5M. Dividing $579.9M by 219.5M gives a pro forma EPS of $2.64. While BigCo's standalone EPS is $2.50.

So, the outcome is that the deal is +5.7% accretive. Three things made it work in BigCo's favour including its higher P/E (20x vs SmallCo's 15x) which meant the stock consideration wasn't too dilutive, the synergies more than offset the incremental D&A cost, and the mixed funding avoided issuing too many new shares.

Common Merger Model Interview Questions

Here are some of the most common merger model interview questions, along with what a strong answer looks like.

1. Walk me through a merger model.

I'd start by projecting standalone financials for both the acquirer and the target. Then determine the purchase price and financing structure. If stock is used, I'd calculate new shares issued. If debt is used, I'd calculate incremental interest expense.

I’d combine the two income statements, add synergies, subtract incremental D&A from purchase price allocation, and adjust for the financing costs, all on an after-tax basis. Then divide combined net income by new shares to get pro forma EPS, and compare that to the acquirer's standalone EPS to determine accretion or dilution.

2. What are the main ways to make a dilutive deal accretive?

Some of the ways to make a dilutive deal accretive include:

Increasing synergies, which adds to combined net income

Lowering the purchase price, which reduces the financing cost

Shifting the financing mix toward cheaper debt and away from equity

Structuring the deal so the stock component is smaller, reducing share dilution

3. If an acquirer has a higher P/E than the target, is an all-stock deal accretive?

Generally yes. A higher P/E means the acquirer's stock is more expensive. So the buyer will need to issue fewer shares to fund the deal. That means less dilution to the share count, and the target's contributed earnings offset those new shares. So, pro forma EPS ends up higher than before and the deal is accretive.

Common Merger Model Mistakes

Below are some of the common pitfalls to avoid when building a merger model:

Over-Optimistic Synergies. Stacking aggressive cost and revenue synergies on top of already-optimistic projections is the most common error. Synergies are speculative, take time to materialise, and carry real execution risk. Always keep estimates low and phase them in over 2–3 years.

Forgetting to Tax-Effect Income Statement Adjustments. Interest expense, incremental D&A, and lost interest on cash all hit above the tax line. So, apply the appropriate tax rate before they flow into net income to avoid overstating the cost of the deal and distorting the accretion/dilution result.

Using the Wrong Share Count. Always use diluted shares outstanding, not basic shares. If stock consideration is involved in the financing mix, add the new shares issued to the acquirer's existing diluted count.

Ignoring Mid-Year Close Timing. Deals rarely close on December 31st. If a deal closes mid-year, only a partial year of the target's earnings and financing costs hit the income statement in year one. Assuming a full year overstates accretion.

Confusing Equity Value and Enterprise Value. The purchase price paid to shareholders is equity value. Enterprise value adjusts for the target's debt and cash, and is used for transaction multiple comparisons like EV/EBITDA. Mixing them up leads to incorrect deal pricing and broken multiple analysis.

Conclusion

A merger model is a decision tool in the M&A deal process. It forces you to convert the strategic logic of a deal, such as why these two companies, at this price, and funded this way, into numbers that either hold up or don't. Accretion is an encouraging output, but it’s not a verdict without a strong why behind it. Likewise, a dilution isn’t outright bad unless it drastically lowers the acquirers EPS or there’s no strategic justification.

Expect interviewers to assess if you understand how changes in assumptions like interest rates, a higher purchase price, or a cash vs stock deal changes the final outcome in a merger model.