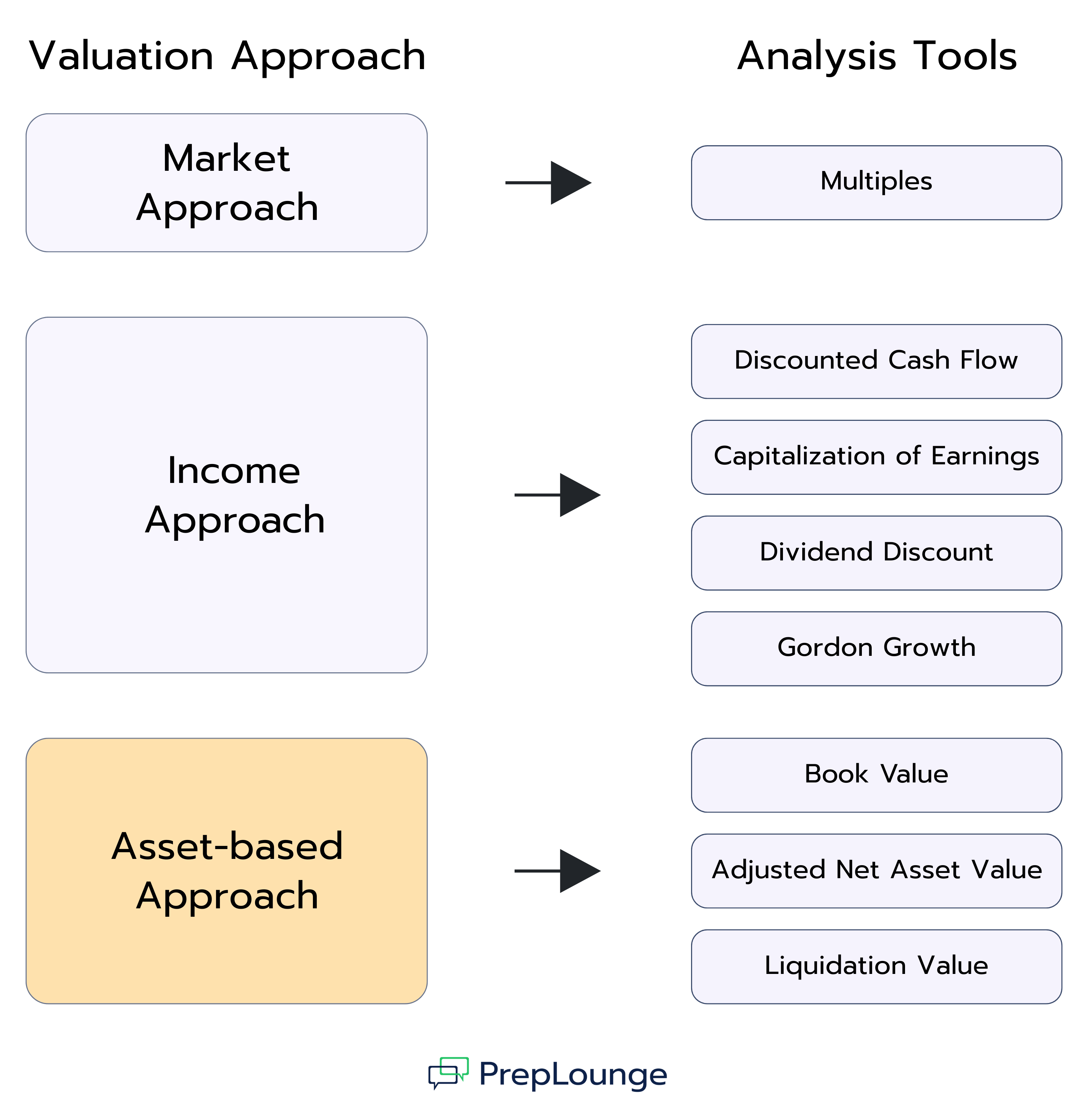

The asset-based approach to company valuation is one of the three primary methods used in finance, alongside the income approach and the market approach. While the income approach values a business based on future cash flows and the market approach relies on valuation multiples to compare companies, the asset-based approach looks directly at the balance sheet. It adjusts a company’s assets and liabilities to their current fair market value, with the difference representing the company’s net asset value (NAV).

This guide explains how the asset-based approach works, outlines its main variants such as book value, adjusted net asset value, and liquidation value, and shows in which situations it is most relevant. You will also find examples of common finance interview questions on this valuation method, as the asset-based approach frequently appears in interviews and assessments for roles in investment banking and corporate finance.

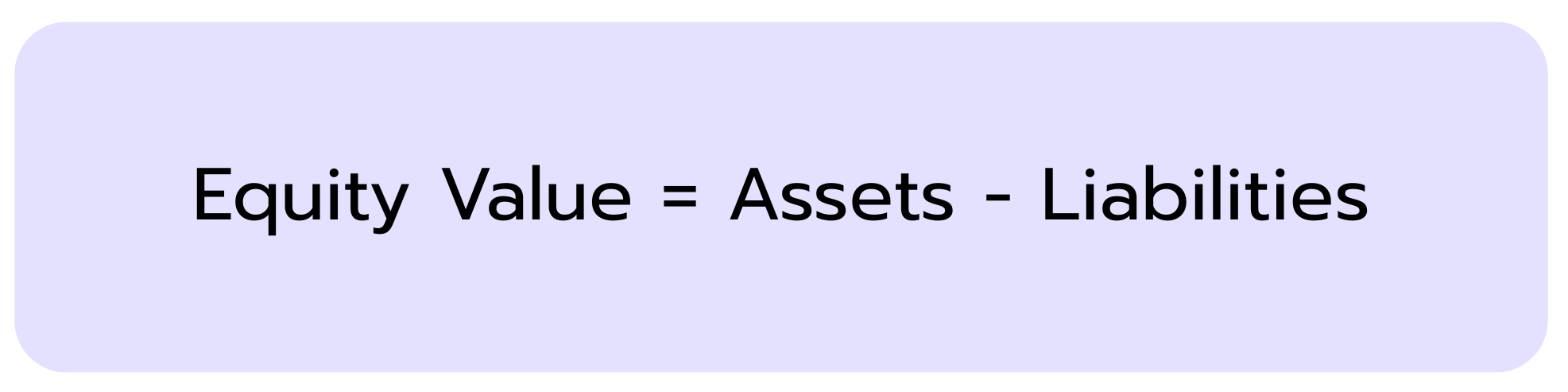

The asset-based approach to valuation follows a straightforward principle: the value of a company equals what it owns minus what it owes. This relationship is often expressed with the formula:

Equity Value is the residual amount that remains for shareholders once liabilities are deducted from assets.

Assets represent everything the company owns that has value, such as property, machinery, inventory, cash, or financial investments.

Liabilities are all obligations the company must settle, including loans, leases, or trade payables.

In practice, analysts do not simply use the book values reported on the balance sheet. Historical cost accounting often does not reflect the true economic situation. Instead, assets and liabilities are restated to fair market value – the price that informed, independent parties would agree upon in a transaction.

Asset-Based Valuation Example:

A company shows the following on its balance sheet:

Assets worth $15m (including a building recorded at its historical cost of $5m)

Liabilities of $5m

Based on book values, equity would be:

$15m – $5m = $10m

In reality, the building has increased in value and could be sold for $15m instead of the $5m shown in the books. This raises total assets to $25m. After subtracting the same $5m in liabilities, the adjusted equity value comes to $20m.

This example makes it clear how rising asset values are often not reflected in book numbers and why fair value adjustments give a more realistic picture of a company’s true worth.

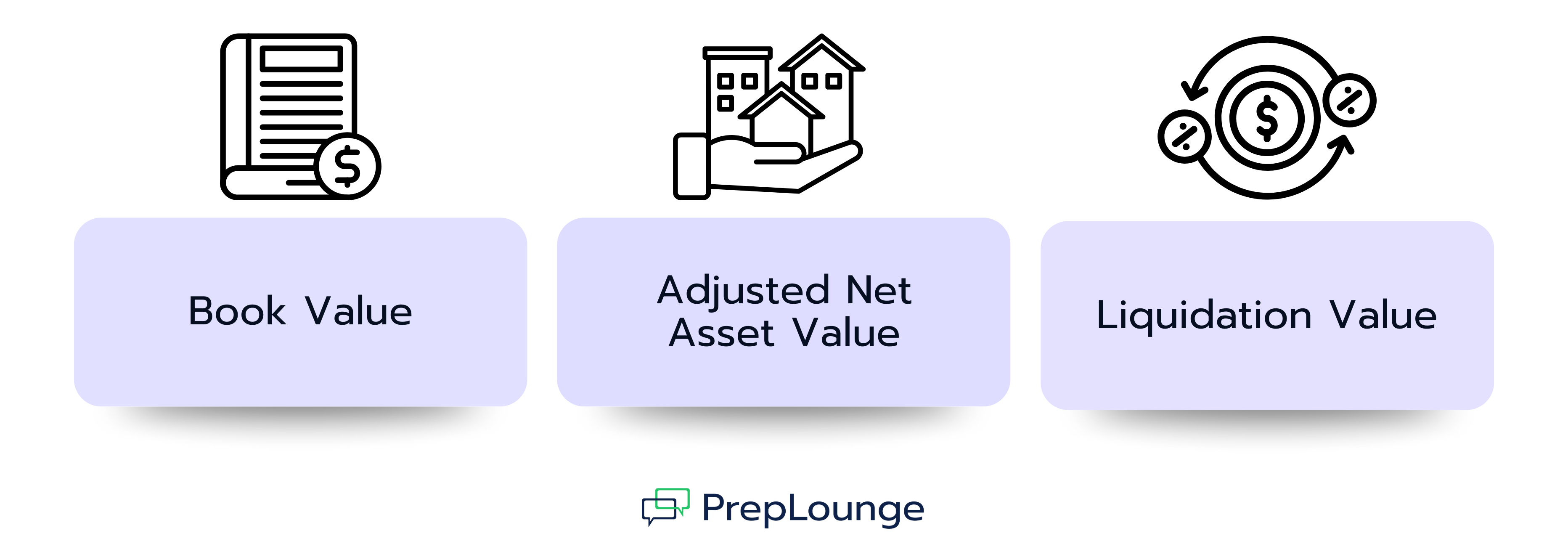

Asset-Based Valuation Methods: Book Value, ANAV, and Liquidation Value Explained

The asset-based approach can be applied in different ways, depending on how assets and liabilities are valued.

Book Value Method in Asset-Based Valuation

The book value method is the simplest form of the asset-based approach to valuation. It takes the figures directly from the company’s balance sheet, which makes it quick and straightforward to calculate. However, this approach can be misleading because assets are recorded at historical cost instead of their current fair market value. As a result, book value often differs significantly from the company’s actual economic value.

Adjusted Net Asset Value (ANAV) Method in Asset-Based Valuation

The Adjusted Net Asset Value method (ANAV) is the most common variant of the asset-based approach to company valuation. Unlike the simple book value, this method adjusts all assets and liabilities to their current fair market value. For example, real estate can be revalued, outdated inventory may be written down, and hidden obligations such as pensions or lease liabilities are included. Intangible assets are usually excluded unless their value can be measured reliably, making ANAV a more realistic way to assess the true net worth of a company.

Liquidation Value in Asset-Based Valuation

The liquidation value method estimates how much could be recovered if all company assets were sold in a distressed sale, for example during bankruptcy or insolvency proceedings. Because such sales are forced and buyers expect discounts, the recovery prices are usually far below normal market levels. Intangible assets such as goodwill, brand names, or intellectual property are often excluded, which is why liquidation value is typically the lowest valuation outcome among asset-based approaches.

When to Use the Asset-Based Approach to Valuation

The asset-based approach to valuation is not always the first choice, but it is highly useful in specific situations. It works well in asset-heavy industries such as real estate, manufacturing, or shipping, where physical assets make up most of the company’s value. It is also commonly applied in distressed valuation and bankruptcy cases, where the recovery value of assets is more important than future growth potential.

In addition, the asset-based approach provides a conservative valuation floor that can be compared with results from other valuation methods. It can also be more informative than the income approach or the market approach when future earnings are too uncertain to model reliably, making it a practical baseline in uncertain or volatile markets.

Common Interview Questions About the Asset-based Approach

To prepare effectively for finance interviews, it is important to practice typical technical questions on the Asset-Based Approach. The following interview questions cover key aspects such as application, limitations and main variants of the method, and highlight what interviewers usually focus on.

1. What is the asset-based approach in company valuation?

The asset-based approach values a company by subtracting liabilities from the fair market value of its assets. Unlike forward-looking methods such as the income approach, it provides a snapshot of what the company is worth today based on what it owns and owes.

Assets include tangible items like property, machinery, or inventory, while liabilities cover obligations such as loans or leases. By adjusting book values to current market values, the method often delivers a more realistic picture of a company’s net worth.

2. When would you use the asset-based approach to company valuation?

The asset-based approach is most useful in asset-heavy industries such as real estate, manufacturing, or shipping. It also plays a key role in distressed or bankruptcy cases, where the recovery value of assets matters more than long-term growth potential.

Analysts may also rely on it when future earnings are too uncertain to forecast, for example in volatile markets. In these cases, the method provides a conservative valuation floor that can be compared with other approaches like DCF or trading multiples.

3. What are the main limitations of the asset-based approach to valuation?

A major limitation is that the asset-based approach ignores a company’s ability to generate future earnings, which is often the primary driver of value. This means the method typically undervalues companies with high intangible assets, such as technology or service firms that rely on brand strength, intellectual property, or customer relationships.

Another drawback is that fair market value adjustments can be subjective when no active market exists for certain assets. As a result, the approach is less reliable in growth-oriented sectors where value is tied to intangible factors.

4. What are the main variants of the asset-based approach?

There are three main variants of the asset-based approach.

Book Value uses unadjusted balance sheet numbers, which makes it quick but often inaccurate since assets are recorded at historical cost.

Adjusted Net Asset Value (ANAV) is the most common form, as it restates assets and liabilities at fair market value, offering a more accurate estimate of equity.

Liquidation Value shows how much capital could be recovered if all assets were sold, for example in the case of bankruptcy. It often serves as a floor valuation, as it represents the minimum value of a company.

5. Why does the ANAV approach adjust book values to fair market value?

Because book values are based on historical cost, they often do not reflect the current market value of assets and liabilities. For example, a building bought 20 years ago may be listed at its original purchase price, even though its market value is much higher today.

By adjusting values, analysts ensure the company’s equity value reflects what informed buyers and sellers would realistically agree on. This makes the valuation more accurate and relevant for transactions, investments, or restructuring decisions.

👉 Want to practice more valuation questions? You’ll find a full set in our Case Library.

This set of questions is designed to help you master the fundamentals of Enterprise Value (EV) and Equity Value. The questions start with basic concepts, such as the difference between EV and Equity Value, and progress to key topics like calculating EV, the impact of diluted shares, and understanding the Treasury Stock Method.

In total, walking through this set in an interview would take approximately 30 minutes, making up around 60% of a typical 45-minute interview. Below, you’ll find model answers for each question, along with tips for the interviewer on what to look for in candidate responses.

This set of questions helps you apply key LBO concepts in practical, realistic interview scenarios. You'll explore how leveraged buyout logic is used to assess deal structures, compare financing options, and evaluate the impact of working capital changes, covenants, and dividend recapitalizations on investor returns.

In total, walking through this set in an interview would take approximately 35 minutes, making up around 70% of a typical 45-minute interview. Below, you’ll find model answers for each question, along with tips for the interviewer on what to look for in candidate responses.

This set of questions is designed to help you prepare for the most common valuation topics in finance interviews. It covers the basics (like DCF, comparables, and multiples) but also includes practical scenarios that test whether you can apply these concepts in context.

Set aside about 30–35 minutes to go through everything. For each question, you’ll find a clear model answer to check your reasoning and deepen your technical knowledge.

The asset-based approach to valuation determines a company’s worth by comparing the fair market value of its assets with its liabilities. It is particularly relevant in asset-heavy industries such as real estate, manufacturing, and shipping, as well as in distressed or bankruptcy situations where the recovery value of assets matters more than future growth potential.

In finance interviews, you should be able to explain the basic asset-based valuation formula, describe the three main variants (book value, adjusted net asset value, and liquidation value), and outline both the strengths and limitations of this method. While it does not account for future earnings, the asset-based approach provides a conservative valuation floor and acts as a useful complement to the income approach and the market approach.

Move on with the next articles:

Multiples

Valuation Models

Multiples are a key analysis tool within the market-based valuation approach. Instead of projecting a company’s future cash flows, this method determines value by comparing a business to similar companies or past transactions. The idea is simple: if comparable firms trade at certain valuation ratios, such as EV/EBITDA or P/E, the target company should trade at a similar level.

This makes multiples a relative valuation method, in contrast to income-based approaches like the Discounted Cash Flow (DCF) analysis, which estimate intrinsic value by discounting future cash flows. By focusing on observable market data, multiples provide a quick and practical way to assess value, but they also depend heavily on finding truly comparable companies or deals.

[Diagram showing valuation approaches and related analysis tools. Market-based approach links to Multiples. Income-based approach links to Discounted Cash Flow (DCF), Capitalization of Earnings, Dividend Discount Model (DDM), and Gordon Growth Model (GGM). Asset-based approach is listed but not linked to a specific tool.]

A Leveraged Buyout (LBO) Model is a popular financial analysis tool for private equity firms, typically built in Excel. It’s used to assess whether a company is worth acquiring primarily with debt. In an LBO, private equity firms or investors purchase a company by combining equity, or their money, with debt. The model projects the target company's financial performance, including revenue, expenses, and cash flow, post-acquisition to show how its cash flow will be used to service and pay down the large amount of debt taken on.

The main purpose of building an LBO model is to determine the potential returns for the equity investors, like the private equity firm, by calculating metrics such as Internal Rate of Return (IRR) and Multiple on Invested Capital (MOIC) at the time of an eventual sale or exit. It also helps assess the company's ability to handle the debt burden.

The Dividend Discount Model (DDM) is an income-based valuation method used to estimate the fair value of a company’s stock. It assumes that the value of a stock today equals the sum of all its future dividend payments, discounted back to their present value. By focusing on dividends as the key return to shareholders, the DDM directly links a company’s payout policy to its valuation.

Within the broader landscape of valuation models, the DDM is part of the income approach, alongside methods like the Discounted Cash Flow (DCF) analysis or the Gordon Growth Model (GGM). Unlike market-based valuation approaches that rely on relative comparisons, the DDM seeks to determine a company’s intrinsic value by analyzing fundamentals and the time value of money.

[Dividend discount model]