In finance, Mergers & Acquisitions (M&A) refers to the process of mergers and corporate takeovers, where companies are combined or acquired to achieve strategic growth, greater efficiency, or competitive advantages.

In mergers and acquisitions (M&A), every deal has two sides: the sell-side and the buy-side. The sell-side team represents the seller and supports them in preparing the business for sale, reaching out to potential buyers, and negotiating the best possible price and terms. On the other side, the buy-side team works with the acquirer to identify attractive targets, evaluate them, and execute the purchase.

Investment banks and advisory firms often act on either side of a transaction. Most firms work on both buy-side and sell-side assignments across different deals, but never on both sides of the same transaction as that would create a conflict of interest. This guide will focus on the sell-side M&A process and provide sample interview questions to help you prepare for investment banking interviews.

A sell-side M&A process refers to the sequence of steps a company or business owner takes when they decide to sell their company or a business unit, usually with the assistance of advisors like investment bankers. The goal is to attract competitive offers, maximize value, and ensure a smooth transaction outcome for the seller. Here's an overview of the general sell-side M&A process:

Let’s cover each of these steps in detail below.

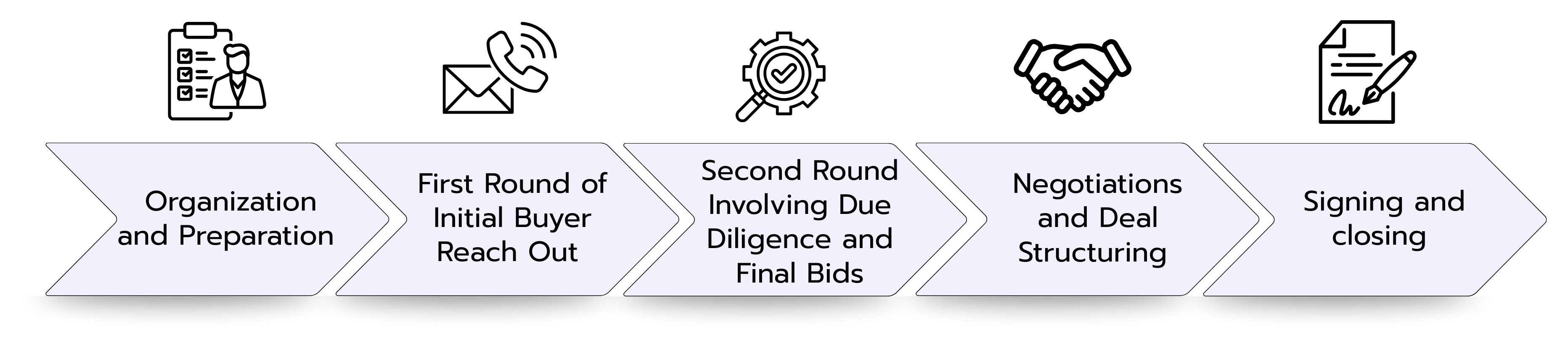

1. Organization and Preparation

The sell-side M&A process usually begins with choosing an advisor. Sometimes the seller reaches out to investment banks after deciding to explore a sale, and sometimes banks proactively approach potential sellers to pitch their services.

To win the mandate, banks prepare a pitch book: a presentation that outlines the company’s market position, a valuation range, a list of potential buyers, and a proposed deal strategy. It also explains why that particular bank is the best fit to lead the transaction. Once the seller selects an advisor and signs a formal agreement, the bank officially represents them in the process.

From there, the preparation stage is all about building the foundation for a smooth sale. This includes creating:

A Teaser: A short, anonymous summary of the business used to generate initial interest without revealing its identity

Confidential Information Memorandum (CIM): A longer document that tells the company’s story in detail, including its financials, operations, market position, and growth opportunities.

During this stage, the bank also performs a valuation to estimate what the company is worth, using methods like Discounted Cash Flow (DCF) or comparable company analysis. They also compile a targeted buyer list. A good list mixes both strategic buyers, which are companies in the same industry, and financial buyers such as private equity firms. Let us briefly compare strategic buyers and financial buyers:

Another preparation effort in this early phase is creating a secure online data room that contains all the documents buyers will eventually need to review. A clear timeline is also set to keep the process moving and maintain competitive tension. Once all this is ready, the bank can move into the first round of outreach.

2. First Round: Initial Buyer Outreach

The first round focuses on generating interest and filtering out less suitable buyers. The bank begins by sending the teaser to selected buyers. If they want to learn more, they must sign a Non-Disclosure Agreement (NDA), which legally prevents them from sharing sensitive information. After the NDA is signed, the CIM is provided, giving them a comprehensive view of the business.

As buyers digest the CIM, they often submit written questions, and the bank coordinates responses from the seller. At the end of this stage, interested parties submit an Indication of Interest (IOI) – a non-binding letter stating a preliminary valuation range and proposed terms. The bank and seller then review these IOIs, screening for buyers who are credible, financially capable, and aligned on price expectations. The most promising candidates are invited to the second round.

3. Second Round: Due Diligence and Final Bids

In the second round, buyers take a much deeper look at the business. They meet with the management team to understand the company’s strategy, culture, and growth plans. They also gain expanded access to the data room, allowing them to review detailed financial records, contracts, and operational information. In some deals, site visits are arranged so buyers can see the facilities in person.

Buyers who want to move forward submit a Letter of Intent (LOI), which is more detailed than an IOI and outlines the proposed purchase price, structure, and key terms. Although still non-binding in most areas, the LOI signals a serious commitment to proceed if due diligence confirms the buyer’s assumptions. From here, the seller usually selects a preferred bidder.

4. Negotiations and Deal Structuring

Once a preferred bidder is chosen, the focus shifts to finalizing the commercial and legal terms. This involves negotiating the purchase price, payment structure, and purchase price mechanics. The common payment structures are all cash, shares, or an earn-out, and simply define how the buyer will pay the seller. The purchase price mechanics are detailed financial rules that ensure the final price fairly reflects the company’s actual financial position at the time of closing the deal. They determine how the final amount will be adjusted for factors like working capital, debt, or cash at closing.

The parties also agree to exclusivity, meaning the seller will negotiate only with this buyer for a set period. This allows both sides to work toward a final agreement without the distraction of other bidders. These negotiations ultimately lead to the drafting of the main legal contract.

5. Signing and Closing

If the parties agree on the deal structure terms, they go ahead to sign and execute the Sale and Purchase Agreement (SPA), which sets out the legal obligations of each side. However, closing or the actual transfer of ownership and payment may be delayed until certain closing conditions are met. These could include regulatory approvals, financing arrangements, or other contractual requirements.

At closing, the buyer compiles a funds flow statement which lists every source of money for the acquisition such as buyer's own funds, loans, ormezzanine financing and every use or recipient of the money like seller payment, repayment of seller’s debts, payments to advisors and legal teams, and escrow accounts. Once the funds are transferred according to the agreed funds flow, the buyer takes legal ownership of the company. Transition steps, such as introducing new management or integrating operations, may then begin.

Common Interview Questions on Sell-Side M&As

The common interview questions about sell-side M&A test your understanding of the process, strategic thinking, and communication skills in explaining complex deal details clearly. Here are sample questions to help you practice.

1. What is the difference between a merger and an acquisition?

In a merger, two companies of roughly equal size combine to form a new entity. An acquisition is when one company purchases and absorbs another, with the buyer retaining control.

2. Walk me through the sell-side M&A process.

The sell-side M&A process usually starts with selecting an advisor. Either the seller reaches out to banks, or banks pitch their services through a pitch book outlining valuation, potential buyers, and strategy. Once a bank wins the mandate, it formally represents the seller in the transaction. Once an engagement letter is signed, the rest of the process includes:

Preparation: Gather financials, draft the Confidential Information Memorandum (CIM), and build a buyer list.

Marketing: Send out teasers, execute NDAs, and share the CIM with interested buyers.

Bidding: Collect Indications of Interest (IOIs), hold management presentations, and receive Letters of Intent (LOIs).

Due Diligence: Provide data room access for buyers to review financial, legal, and operational details.

Closing: Negotiate the purchase agreement and finalize the transaction.

3. What does an M&A pitchbook include?

An M&A pitchbook is a presentation prepared by investment bankers to pitch their advisory services to a potential client. It outlines the banker’s credentials, the market opportunity, the client’s positioning, and proposed strategies for selling the business or executing a deal.

4. How would you value a company?

To value a company there are three main methodologies:

Comparable Companies Analysis looks at valuation multiples of similar publicly traded firms.

Precedent Transactions analyzes multiples paid in recent M&A deals within the same sector.

Discounted Cash Flow (DCF) values the business based on projected free cash flows discounted back to present value.

5. From the seller’s perspective in an M&A deal, is it better to receive cash (often from debt financing) or stock as consideration?

From a seller’s view, cash from debt financing is preferable. It gives certainty of value and avoids exposure to the buyer’s future performance.

6. Between a strategic buyer and a financial buyer, who would generally offer a higher purchase premium?

Strategic buyers typically offer higher premiums because they can realize revenue and cost synergies that financial buyers cannot. Strategics value operational improvements, market expansion, and economies of scale.

Financial buyers are more disciplined about price, focusing primarily on financial returns and requiring deals to meet specific IRR thresholds, usually limiting their ability to pay premium prices.

7. What are the three common sale process structures in M&A?

Broad Auction: Wide marketing to many potential buyers for maximum competition and price discovery.

Limited/Targeted Auction: Selective process with 5-10 qualified buyers, balancing competitive tension with confidentiality.

Negotiated Sale: Direct negotiations with one preferred buyer, often used when speed, certainty, or strategic fit are priorities over maximizing price.

8. What is purchase consideration in M&A?

Purchase consideration is the total compensation paid to the seller's shareholders, including:

All Cash: Full payment in cash upon closing.

Stock / Shares: Payment partially or fully through the buyer's shares.

Earn-Out: A contingent payment based on future company performance.

Often a combination of these methods is used to balance risk and reward between buyer and seller.

9. When would a joint venture make more sense compared to a full acquisition?

A joint venture usually makes more sense compared to a full acquisition when parties want shared risk, limited capital commitment, market testing, or regulatory ease before full integration.

10. How would you ensure confidentiality in a competitive bidding process?

Confidentiality is maintained through a mix of legal safeguards and strict process controls. Robust NDAs with specific provisions and penalties are signed by all potential bidders. Information is released in stages through a secure data room with access controls and audit trails, and code names are used for the target and the process. Finally, management exposure is limited until later stages, with legal oversight ensuring compliance throughout.

👉 Want to practice typical M&A questions in a real interview format? Check out our Case Library for hands-on examples and detailed solutions.

Case Library

Discover more than 200 practice cases for every level and case type.

The sell-side M&A process follows a clear structure that helps sellers maximize value and ensure a smooth transaction. It begins with careful preparation, including the selection of an advisor, creation of marketing materials such as a teaser and CIM, and development of a targeted buyer list. The process then moves into two rounds of outreach, where initial interest is tested through NDAs, CIMs, and IOIs, followed by more detailed due diligence, management meetings, and LOIs from serious bidders.

Once a preferred buyer is selected, negotiations focus on price, payment structure, and purchase price adjustments, eventually leading to the drafting and signing of the Sale and Purchase Agreement. Closing finalizes the transaction through the transfer of funds and ownership. For your interviews in finance, be ready to walk through these steps clearly, explain valuation methods, compare strategic and financial buyers, and discuss deal structures with confidence.

Let's Move On With the Next Articles:

Buy‑Side M&A

Processes in Finance

In finance, Mergers & Acquisitions (M&A) refers to the process where companies are combined or acquired to achieve strategic growth, efficiency, or market advantages.

Mergers and acquisitions (M&A) transactions have a buy-side and a sell-side. The sell-side team represents the seller and works to market the business to potential buyers, while the buy-side team represents the acquirer. For the buyers or acquirers, the focus is on acquiring the right target with minimal risk and maximum strategic or financial upside. So it requires a lot of due diligence, valuation analysis, and strategic assessment.

Read on to understand the entire buy-side M&A process and get some practice questions to prepare for finance interviews.

A Leveraged Buyout (LBO) is a type of acquisition where a buyer chooses to finance the purchase using borrowed money or debt and some cash investment, known as equity. So, the "leverage" in leveraged buyout refers to this heavy use of debt financing. In most LBOs, 60-90% of the purchase price comes from borrowed money, while only 10-40% comes from the buyer's own cash.

The buyer uses the future cash flows and assets of the company being acquired as collateral for the loans. They can also use the assets of the acquiring company if necessary. Over time, the debt is paid back using the cash that the target company generates. The buyers aim to exit profitably through a sale, merger, or public offering after improving the company's performance and paying down the debt.

EBIT stands for Earnings Before Interest and Taxes.

Depending on the company or language, EBIT may also be referred to as:

- Operating Income or Operating Profit

- Earnings before Interest and Taxes (in German reports)

- Betriebsergebnis (commonly used in German-speaking regions

This metric shows how much a company has earned from its core operations before taking into account financing costs (interest) and taxes.

EBIT can also be described as operating result or operating profit. The aim is to assess a company’s operational performance on its own, without distortion from different financing methods or tax rates.

Why is this important? Because it allows you to compare companies independently of one another. Whether a company has taken out many loans or benefits from a particularly low tax rate does not affect its EBIT.