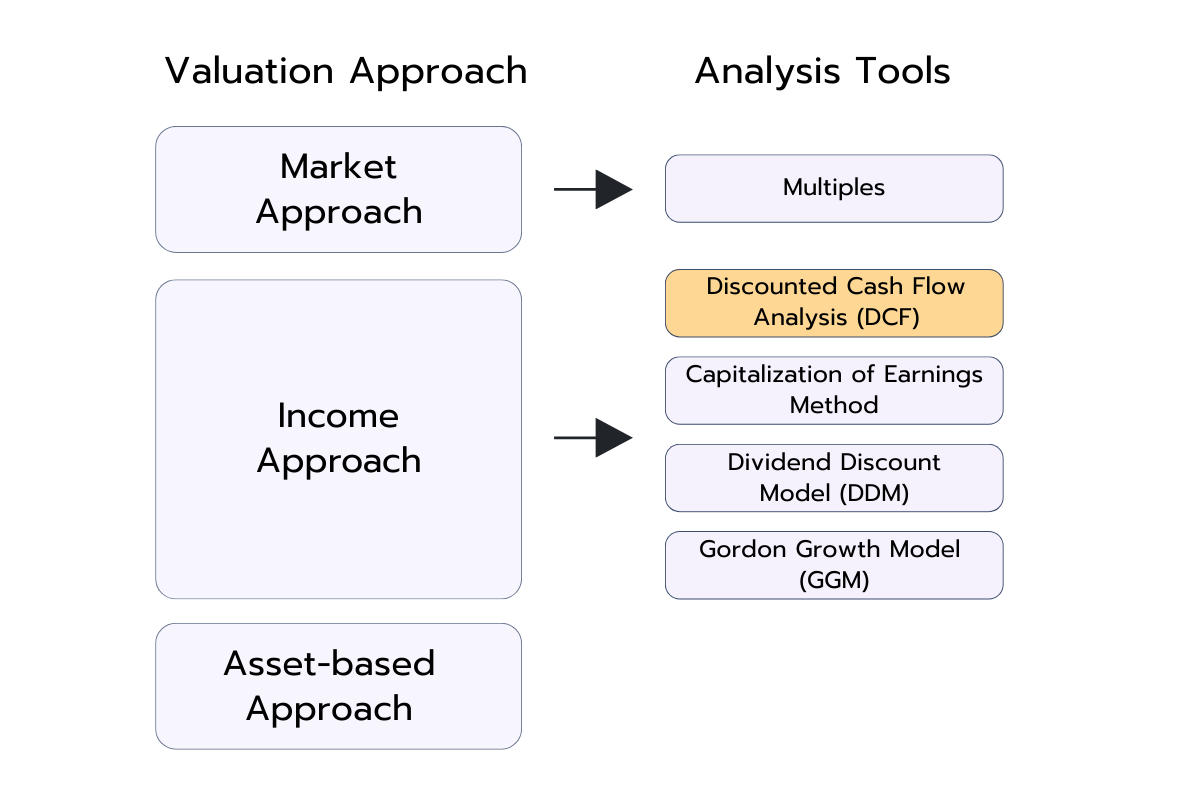

The discounted cash flow (DCF) analysis is one of the most important valuation methods in finance. Among the commonly used valuation models, the DCF method belongs to the income-based approaches.

It complements market-based methods like multiples or transaction analyses as well as asset-based approaches like the net asset value. The DCF method is one of the most frequently used models in practice, especially in investment banking, private equity, and strategic corporate valuation.

The core idea of the DCF analysis is to determine the present value of a company based on the future cash flows it will generate. Instead of relying on past profits, the method uses expected free cash flows as the basis for valuation. These cash flows are discounted to their present value using an appropriate rate, the so-called WACC (Weighted Average Cost of Capital), in order to calculate the enterprise value.

How Does the DCF Method Work?

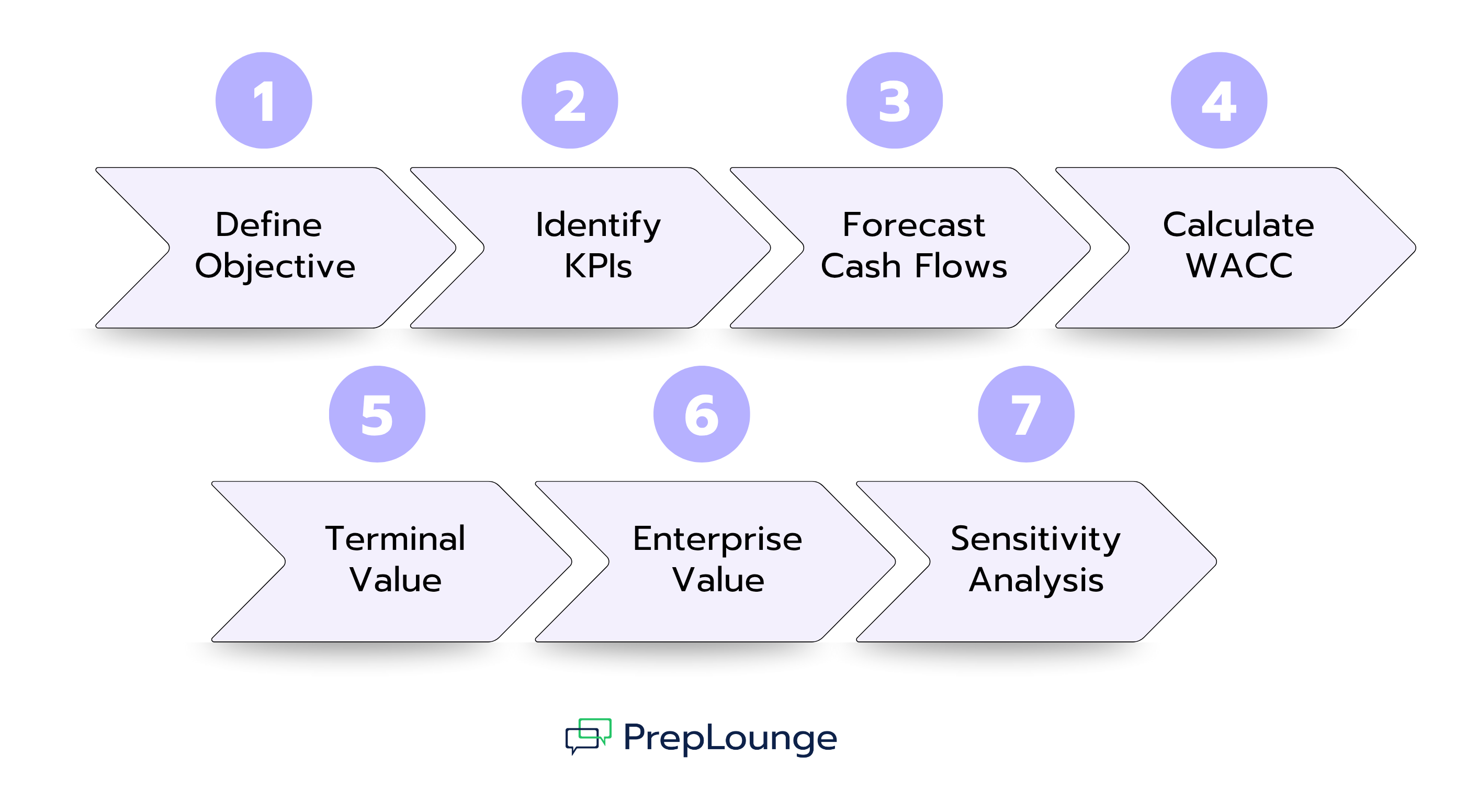

Step 1: Define the Objective.

At the beginning of any DCF analysis, the objective must be clearly defined. Are you valuing the entire company or just a business unit? Is it a single project, an acquisition, or a division? This objective determines which financial metrics must be considered and which cash flows are included.

For example, if you're working for a company considering building a new plant in Southeast Asia, you must first define what exactly is being analyzed:

The whole company? Then you need to incorporate all business units, locations, and financial streams – from marketing expenses to corporate debt.

Just the new plant? Then your focus is only on the project-specific investment costs, ongoing revenues, and expenses.

A business unit? Then isolate the cash flows and KPIs relevant to that region.

This definition is crucial as it determines the relevant financial data and assumptions. Whether you’re valuing a company, a division, or a project, the required inputs differ significantly.

Step 2: Identify Relevant KPIs.

Next, analysts evaluate the financial situation of the target and identify key performance indicators (KPIs) for the cash flow forecast. These KPIs form the backbone of the DCF model. The stronger and more realistic the assumptions, the more reliable the result.

The most important KPIs include:

Revenue growth, to reflect scalability and market development

EBITDA and EBIT margins, to assess operational efficiency and profitability

CapEx, needed to maintain operations or enable growth

Changes in working capital, which affect short-term liquidity

The tax rate, to correctly reflect the net effect on free cash flows

These metrics are often based on a mix of historical financials, internal planning, and market assumptions. Integrated financial models that link P&L, balance sheet, and cash flow statement are commonly used, especially for larger firms or institutional investors.

Depending on the industry, additional KPIs might be critical. In software, for instance, CAC (Customer Acquisition Cost) and CLV (Customer Lifetime Value) are key. In capital-intensive sectors, utilization rates, maintenance costs, or price-volume effects matter more. Other metrics like ARPU (Average Revenue per User), churn rate, or net revenue retention may also be relevant depending on the business model.

It’s also important to align KPIs with strategic value drivers: investments in growth, margin improvements, or working capital optimization all directly impact the cash flow profile. Thinking like an investor means linking metrics to long-term value.

Interviewers often ask how to derive KPIs from the P&L and balance sheet or which assumptions are most sensitive. Plausibility checks are expected: Do forecast margins align with history? Are growth rates realistic for the sector? Do investment plans match revenue expectations?

Step 3: Forecast Free Cash Flows.

After defining the objective and identifying KPIs, the core of the DCF model follows: projecting future free cash flows. This means estimating how much cash the company will have available over the coming years, after paying operating costs, making necessary investments, and adjusting working capital.

Typically, a five- to ten-year forecast period is used. Each year’s free cash flow is estimated based on actual cash movement, not just accounting profits.

What is free cash flow? Free cash flow (FCF) is the cash a company has left after all operating and investing activities. It can be distributed to shareholders or used to pay down debt. The calculation involves several steps:

Start with EBIT (operating profit before interest and taxes, after depreciation)

Adjust for taxes: EBIT × (1 – tax rate)

Add back depreciation (a non-cash expense)

Subtract capital expenditures (CapEx)

Adjust for changes in working capital

This results in the free cash flow for a given year.

Why is this forecast so important? The entire DCF model hinges on future cash flows. The better the forecast, the more reliable the valuation. However, predicting the future is difficult, so assumptions must be well-grounded.

Common questions include:

Is expected revenue growth realistic, based on market analysis or internal goals?

Are margins stable or improving? Are economies of scale achievable?

Do CapEx plans match growth expectations?

How will working capital needs evolve?

Are there one-off or cyclical effects to consider?

Because projections are assumption-driven, transparency is essential. Professional models often include multiple scenarios (e.g., base, growth, and downside) to show a range of possible outcomes.

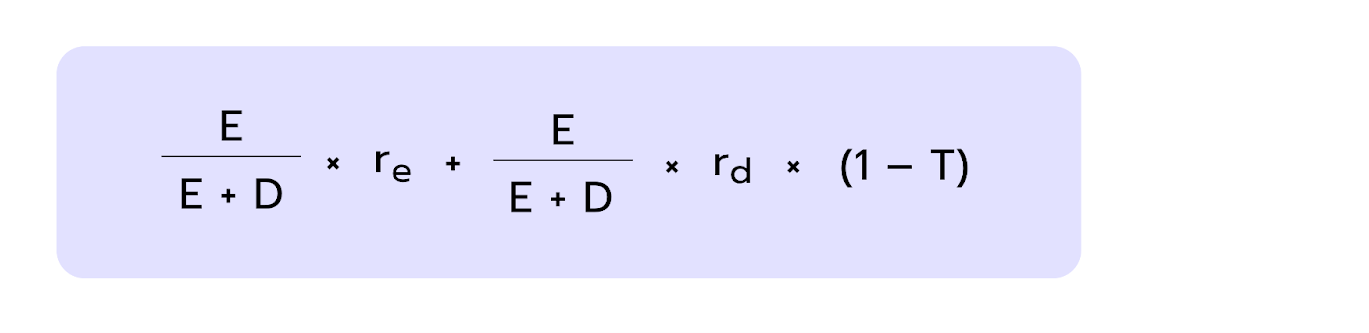

Step 4: Calculate WACC.

Once the future cash flows are projected, the question becomes: what are those cash flows worth today? To find out, they are discounted back to present value using a discount rate – usually the Weighted Average Cost of Capital (WACC).

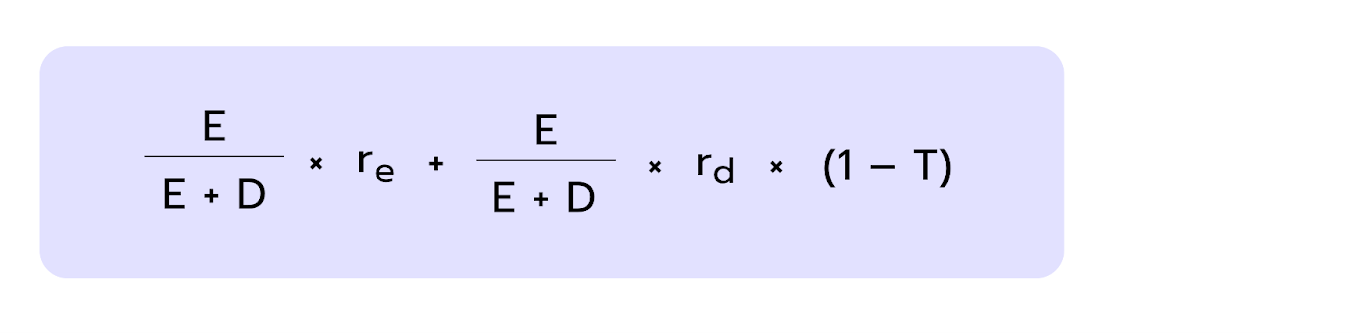

WACC reflects the average cost of capital for a company, combining the required return on equity with the cost of debt, weighted by their respective proportions in the capital structure. The higher the WACC, the lower the present value of future cash flows. Here is how to calculate it:

1. Determine Target Capital Structure

Estimate how the company is typically financed (debt vs. equity). Use historical data, peer comparisons, or strategic targets.

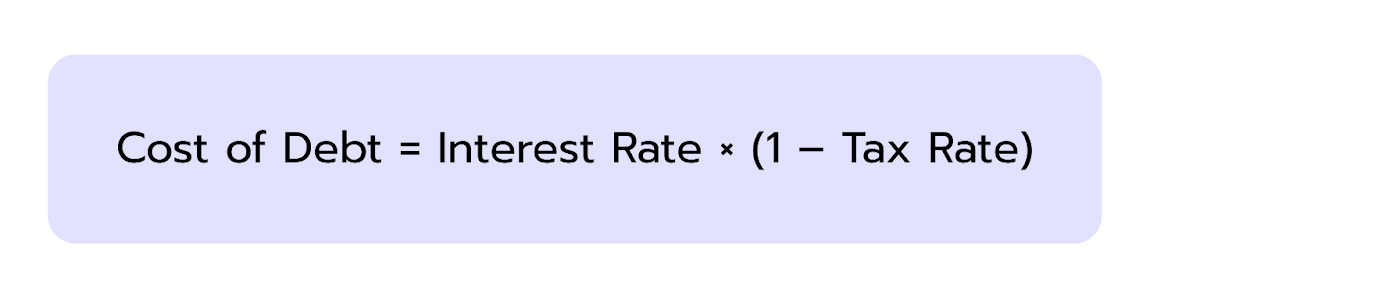

2. Calculate Cost of Debt (After-Tax)

This reflects the interest rates at which the company can borrow, adjusted for tax benefits:

Use current market rates, not historical loan terms.

3. Calculate Cost of Equity Using CAPM

Risk-free rate: usually based on long-term government bonds

Beta: measures the stock’s volatility versus the market

Market risk premium: expected return above the risk-free rate

4. Apply WACC Formula

Where:

E = market value of equity

D = market value of debt

re = cost of equity

rd = cost of debt

T = Tax Rate

Why is WACC important? WACC significantly influences the valuation: a lower WACC increases present value and vice versa. Even a 1% change can shift enterprise value considerably, making precise and reasonable calculation critical.

Step 5: Determine Terminal Value.

After forecasting free cash flows for the explicit forecast period (usually 5 to 10 years), one big question remains: What happens after that? Companies don't just stop operating. That’s where theterminal value (TV) comes in.

The terminal value captures the company’s value beyond the forecast period – often accounting for more than half of the total DCF value. So, calculating it carefully is crucial.

There are two main methods:

1. Exit Multiple Method

Assumes the company is sold at the end of the forecast period, like a private equity exit. The sale price is based on a market multiple (e.g., EV/EBITDA or EV/EBIT).

Example: If EBITDA in the final year is $50 million and the multiple is 10x, terminal value = $500 million.

Important:

Use realistic multiples from trading comps or past deals

Adjust multiples for inflation or market cycles if needed

This method is popular in private equity due to its deal-based logic.

👉 For a step-by-step guide, check our article on multiples.

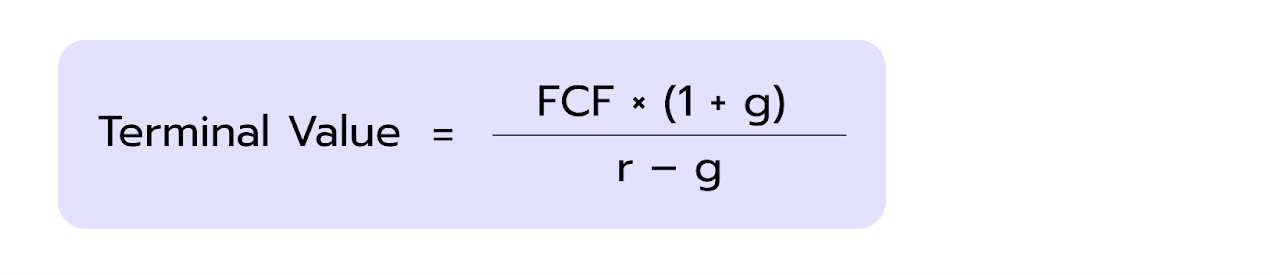

2. Perpetuity Growth Method (Gordon Growth)

Assumes the company continues to operate and grow at a constant rate indefinitely after the forecast period.

Where:

FCF = free cash flow in first year after forecast

r = discount rate (e.g., WACC)

g = perpetual growth rate

What to consider:

g should be conservative, usually between 1–3%, based on inflation, market size, and maturity

Best for stable, mature companies with predictable growth

Small changes in g or r can significantly impact value – run sensitivity analyses

👉 See our Gordon Growth Model article for examples and detailed explanations.

Which method should you choose? Both are valid. It depends on context:

Aspect

Exit Multiple

Perpetuity Growth

Use case

Private equity, exit scenarios

Long-term valuation

Data

Market multiples

FCF growth + WACC

Pros

Market-oriented, practical

Theoretical soundness

Cons

Depends on comparables

Highly sensitive to g and r

Interview tip: If asked which method you prefer, a good answer is: "It depends. If reliable multiples are available, I use the exit method. For stable business models, I prefer the perpetuity growth approach. Ideally, I calculate both and compare."

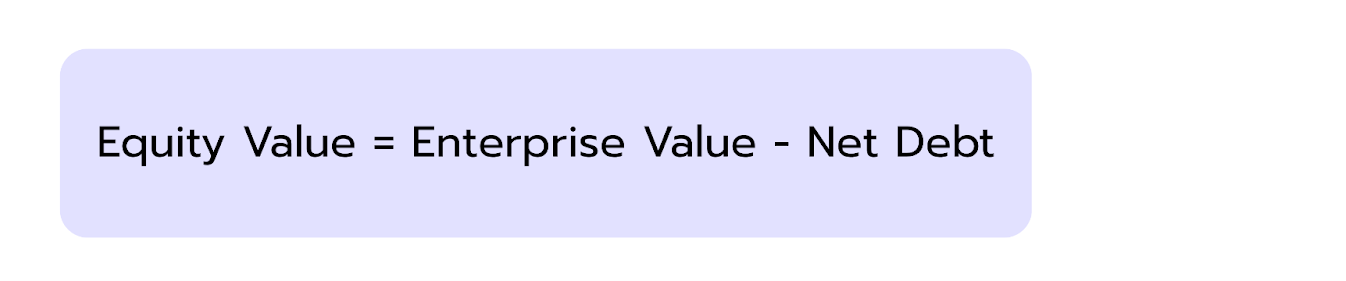

Step 6: Calculate the Enterprise Value.

Once all future free cash flows and the terminal value have been projected and discounted to their present value using the WACC, these values are added together to determine the total value. The result is the Enterprise Value (EV): the total value of the company’s operating business, independent of its capital structure.

The Enterprise Value thus reflects the value available to all capital providers (both equity and debt holders).

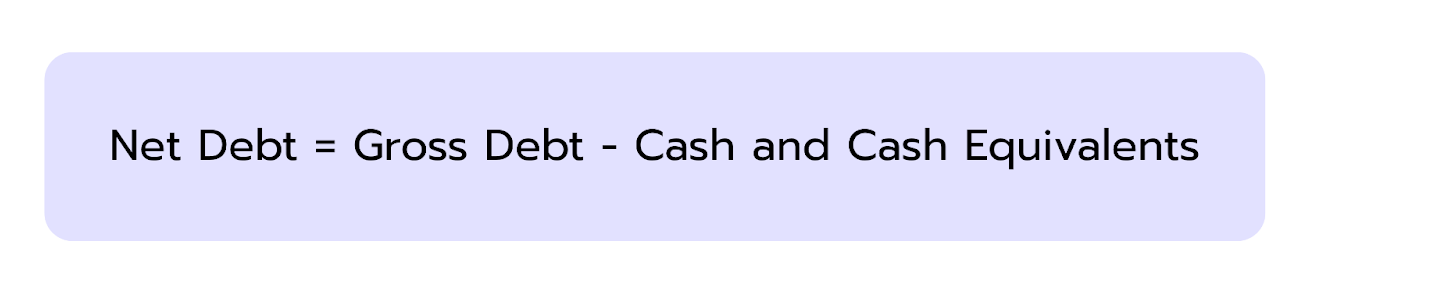

To calculate the Equity Value you subtract the company’s net debt from the Enterprise Value:

Net debt is typically calculated as:

The Equity Value is ultimately the key figure for shareholders or potential investors, as it reflects the portion of the company they “own.”

In professional financial models, the equity value is often shown per share, making it easier to compare to the current share price. For private companies, the value serves as a basis for purchase negotiations, financing decisions, or exit planning.

However, this value is only as reliable as the assumptions behind it. That’s why a final and critical step follows the valuation: the sensitivity analysis.

Step 7: Conduct a Sensitivity Analysis.

The DCF method is a powerful tool, but it stands or falls with the assumptions it’s built on. Even small changes in key parameters, such as the WACC, the terminal growth rate, or margin assumptions can significantly alter the company's valuation.

Because DCF analysis relies on forecasts and estimates, sensitivity analysis is one of the most important final steps. It helps to visualize the effects of uncertainties and shows how robust your valuation really is.

What do you do in a sensitivity analysis?

In a sensitivity analysis, you systematically vary individual input parameters and observe how the calculated company value (typically the equity value) changes. The goal is to identify key value drivers and make potential risks or fluctuations transparent.

Typical formats include:

Two-dimensional tables (sensitivity grids), e.g., WACC on the y-axis and terminal growth rate on the x-axis

One-variable analyses, such as the effect of revenue growth or EBITDA margin on equity value

Scenario comparisons, where multiple assumptions are changed at once:

Base Case: realistic mid-term plan

Best Case: optimistic assumptions

Downside Case: conservative scenario with margin compression or market slowdown

Practical example

In many models, the terminal value accounts for over 60% of the total company value. This means: a seemingly minor change in the assumed terminal growth rate, from, say, 1.5% to 2.5%, can shift the equity value by 15% to 30%.

That’s why you should always test and clearly communicate these assumptions.

Advantages and Disadvantages of the DCF Analysis

The Discounted Cash Flow (DCF) method is one of the most detailed and flexible valuation tools in finance. However, because it relies heavily on assumptions, even small errors can lead to big changes in results.

Advantages of the DCF Analysis

Forward-looking approach: Focuses on future performance rather than past results and is ideal for fast-changing industries or growth companies.

Fundamental valuation: Values a company based on its actual cash flow potential, not on market hype or peer comparisons.

High flexibility: Can easily adapt to different scenarios, from optimistic growth cases to crisis situations.

Detailed understanding of value drivers: Encourages a deep look into key factors like margins, investments, and working capital.

Disadvantages of the DCF Analysis

Strong dependency on assumptions: Small changes in inputs like growth or margins can significantly alter the valuation.

Sensitive to terminal value and WACC: These two factors often drive most of the result but are also the hardest to estimate correctly.

Complex and time-consuming: Building a solid DCF model requires reliable data and solid financial modeling skills.

Low comparability: Since every DCF model is based on unique assumptions, comparing results across companies is difficult.

Practical Example: DCF Analysis for Investment Evaluation

To make the DCF method more tangible, let’s walk through a simple but realistic scenario:

A company is planning to build a new production facility. The planned investment costs amount to 15 million USD, which will be incurred at the start of the project. The facility is expected to operate for six years before being decommissioned or replaced.

The company has estimated the following annual net free cash flows for the operating period:

Year

Expected Free Cash Flow

1

2.5 million USD

2

3.5 million USD

3

4.5 million USD

4

5.5 million USD

5

6.5 million USD

6

7.5 million USD

To value the investment, the company uses a WACC of 8%. This isthe minimum return required to make the project attractive to capital providers.

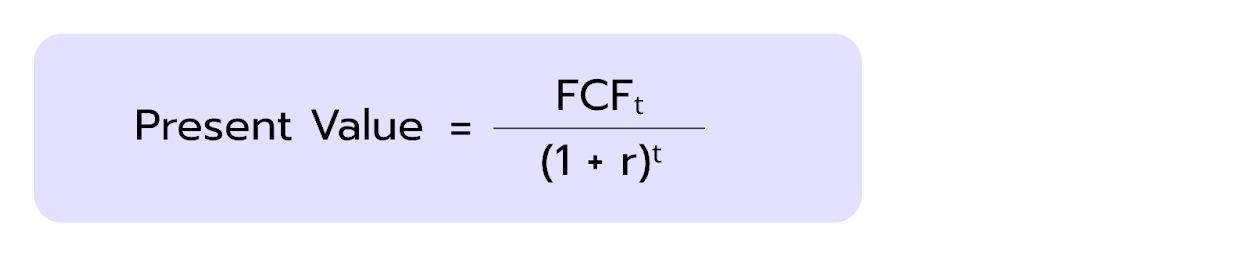

Step 1: Discounting the Free Cash Flows

To determine the present value of future cash flows, we apply the DCF formula to each individual payment:

Where:

FCFₜ = Free Cash Flow in year t

r = Discount rate (here 8%)

Year

Cash Flow (USD)

Discount Factor

Present Value (USD)

1

2,500,000

1.08

2,314,815

2

3,500,000

1.1664

3,000,686

3

4,500,000

1.2597

3,571,800

4

5,500,000

1.3605

4,042,632

5

6,500,000

1.4693

4,423,195

6

7,500,000

1.5869

4,726,196

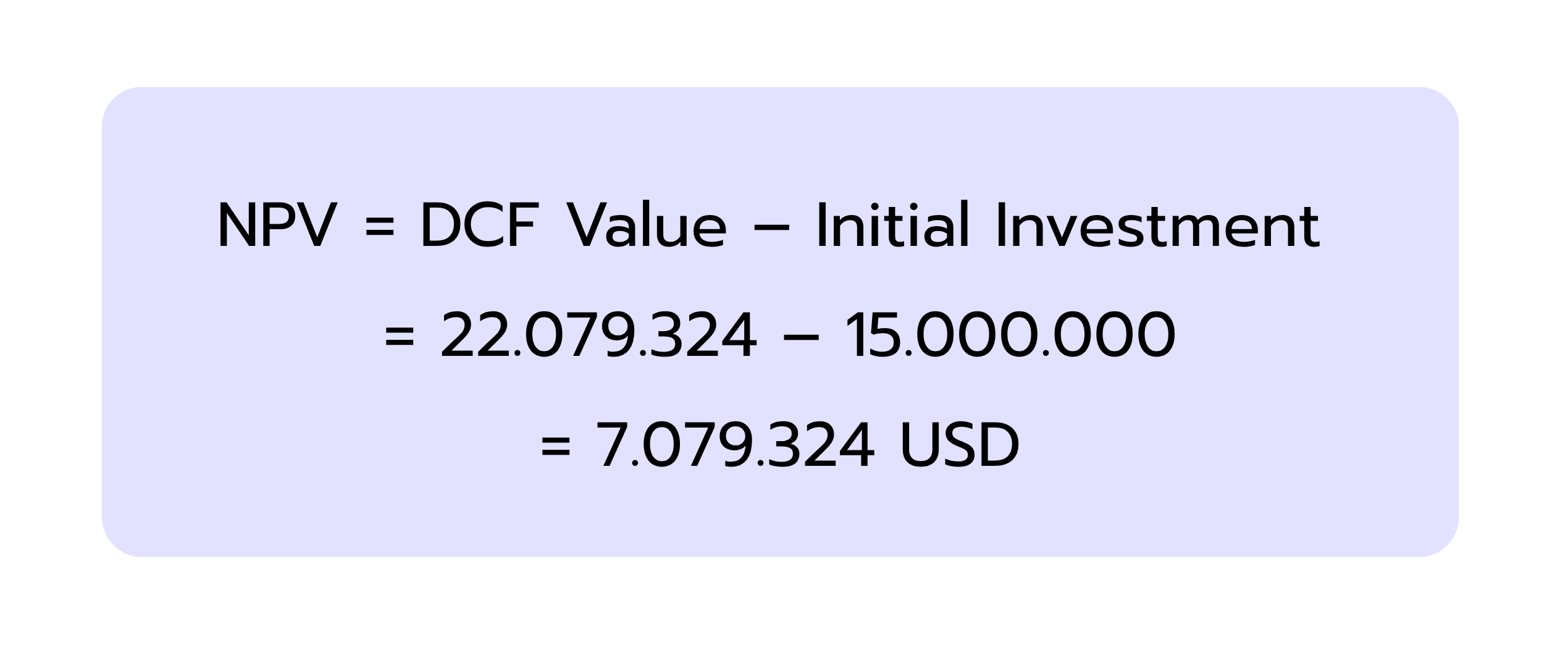

Total DCF Value = 22,079,324 USD

Step 2: Calculating the Net Present Value (NPV)

The DCF value reflects the total present value of future cash flows but doesn’t yet account for the initial investment. To determine the project's profitability, we subtract the initial outlay:

A positive Net Present Value (NPV) of about 7.08 million USD means that the expected cash flows significantly exceed the initial investment. In other words, the project would create value above the required 8% return.

Since the actual return is higher than the WACC, the project generates economic value added from the perspective of capital providers. From the company’s standpoint, this investment contributes to sustainable value creation, a core goal of any sound financial decision.

Common DCF Interview Questions

Questions about the Discounted Cash Flow analysis are standard in interviews for finance roles, especially in investment banking and private equity. Below are some of the most frequently asked DCF-related questions and how you might answer them:

1. Can You Explain How a DCF Valuation Works?

A DCF valuation calculates a company’s value by determining the present value of its expected future cash flows.

Start by creating financial projections based on assumptions like revenue growth, costs, and working capital.

From that, derive the Free Cash Flow (FCF) for each year.

Then, discount these cash flows using a discount rate, usually the WACC (Weighted Average Cost of Capital).

Finally, add up all the discounted cash flows to calculate the Net Present Value (NPV) of the company.

2. How Do You Calculate the WACC?

The formula for WACC is:

Where:

E = market value of equity

D = market value of debt

re = cost of equity

rd = cost of debt

T = Tax Rate

Each component is weighted according to its proportion in the capital structure.

3. What Has a Bigger Impact on a DCF Valuation: a 1% Change in the Discount Rate or a 10% Change in Revenue?

It depends, but in most cases, a 10% change in revenue has a bigger impact.

Why? Because revenue changes affect not only one year’s cash flows but also future years and the Terminal Value, which often makes up the bulk of a DCF valuation.

4. What Are the Pros and Cons of a DCF Valuation?

Pros of DCF Valuation

Cons of DCF Valuation

Provides a fundamental assessment of value based on future expectations.

Heavily reliant on assumptions, small errors can lead to major misvaluations.

Highly flexible and adaptable to different scenarios and assumptions.

Requires deep financial expertise and high-quality data inputs.

👉 You can practice these and many more questions with our cases on the DCF Analysis, so check it out now!

You’re working on a DCF valuation for CloudCore Inc., a publicly traded cloud computing company. You’ve built a standard unlevered DCF model using a WACC of 10% and based on your 5-year forecast, the Enterprise Value (EV) currently comes out to $200 million.

This set of questions is designed to help you prepare for the most common valuation topics in finance interviews. It covers the basics (like DCF, comparables, and multiples) but also includes practical scenarios that test whether you can apply these concepts in context.

Set aside about 30–35 minutes to go through everything. For each question, you’ll find a clear model answer to check your reasoning and deepen your technical knowledge.

This question set helps you go beyond the basics of valuation by comparing key methodologies and exploring when and how to use each one effectively. You’ll review core approaches like DCF, comparables, and precedent transactions, and build on that with LBO analysis, liquidation valuation, and industry-specific multiples.

You should expect to spend 30–40 minutes on the full set. Use the model answers to check your reasoning and refine your technical knowledge.

The Discounted Cash Flow (DCF) method is a powerful way to value a company by looking at its future potential rather than its past performance. Instead of focusing on historical profits or comparing with other firms, it estimates how much cash the company is expected to generate in the future based on factors like revenue growth, profit margins, investments, and working capital.

DCF is especially helpful when you want a valuation that is independent of market mood or short-term trends, such as when making investment decisions, planning acquisitions, or developing long-term strategies.

However, DCF is not a plug-and-play formula. It is a framework that helps you think through a company’s value logically, but its accuracy depends on how realistic your assumptions are.

That’s why it’s important to stay transparent about your inputs, question your assumptions, and perform a sensitivity analysis to see how small changes could affect your results. This way, you can show how reliable your valuation really is.

Let's Move On With the Next Articles:

Terminal Value in DCF: Formula, Methods & Interview Questions

Valuation Models

The Discounted Cash Flow (DCF) model is one of the most widely used valuation methods in finance, and you are almost guaranteed to face questions about it during investment banking interviews. It is built on the premise that a company is worth the sum of all its future free cash flows, discounted back to today's value.

But it's not possible to reliably forecast cash flows year-by-year forever. To solve this without ignoring the company's long-term worth, DCF models forecast in detail for a few years within the explicit forecast period or projection period. Then they bundle everything beyond that forecast horizon into a single figure known as terminal value in DCF.

This comprehensive guide breaks down why terminal value is important in DCF, how it's calculated using the perpetuity growth model vs exit multiple model, how it affects implied enterprise value, common DCF terminal value mistakes, and typical terminal value interview questions.

In finance, strategic frameworks can make a real difference when it comes to understanding a company's position and long-term potential. Among them, the SWOT analysis stands out as a clear and practical method for assessing where a business stands and what factors could shape its future. Whether you're evaluating a target company, preparing for a case interview, or making investment decisions, mastering SWOT can give your analysis more depth and direction.

Porter’s Five Forces is a strategic analysis framework that helps companies and consultants assess the competitive landscape and overall attractiveness of an industry. Developed in 1979 by Harvard professor Michael Porter, the model analyzes five key forces that determine how profitable or challenging a market is.

These five forces evaluate, for example, the bargaining power of suppliers and customers, the ease of market entry for new players, the threat of substitutes, and the intensity of competition among existing firms.

Analyzing these forces helps businesses identify market opportunities, assess potential risks, and build sustainable competitive advantages. The framework also supports strategic decision-making – such as whether to enter a market, how to position a product, or where to allocate resources.