EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It reflects a company’s earnings before taking into account interest payments, tax expenses, and non-cash items like depreciation and amortization. You can think of it as an extended version of EBIT that excludes all depreciation-related costs.

The idea behind this: depreciation and amortization are non-cash expenses and often influenced by accounting methods, assumptions, or company policies. By stripping them out, EBITDA aims to provide a clearer picture of a company’s ongoing operational performance, regardless of how much has been invested or how assets are accounted for.

EBITDA is commonly used as an indicator of operating performance before investment and financing effects come into play. It helps to:

Compare companies of different sizes, industries, or regions.

Assess how much profit is generated from core operations (before interest, taxes, or capex).

Serve as a base for valuation metrics such as the EV/EBITDA multiple.

Analyze the profitability of business models (especially in capital-intensive industries).

An example: Imagine two companies each report €100 million in EBIT. One of them has €50 million in annual depreciation (due to heavy investments in machinery), while the other only has €10 million. Based on EBITDA, both companies appear equally profitable because depreciation is ignored. This can be both an advantage and a risk: EBITDA shows "adjusted" profitability, but also leaves out real costs.

That’s why in private equity and investment banking, EBITDA is often used as a starting point for valuation models. Just keep in mind: EBITDA is a purely accounting-based figure and not an actual cash flow metric!

Where to Find EBITDA in Financial Statements?

EBITDA, like EBIT, is not always directly listed in the income statement. However, many companies (especially publicly traded ones) disclose it in the notes or the management analysis or discussion.

If you want to calculate it yourself, here's how:

Start with the operating profit (this is usually shown in the income statement).

Add back interest and tax expenses to arrive at EBIT.

Then add back depreciation and amortization, including:

Depreciation of tangible assets

Amortization of intangible assets

You’ll often find the necessary figures in the notes to the income statement or in the cash flow statement. Look for terms like "Depreciation", "Amortization", or "D&A".

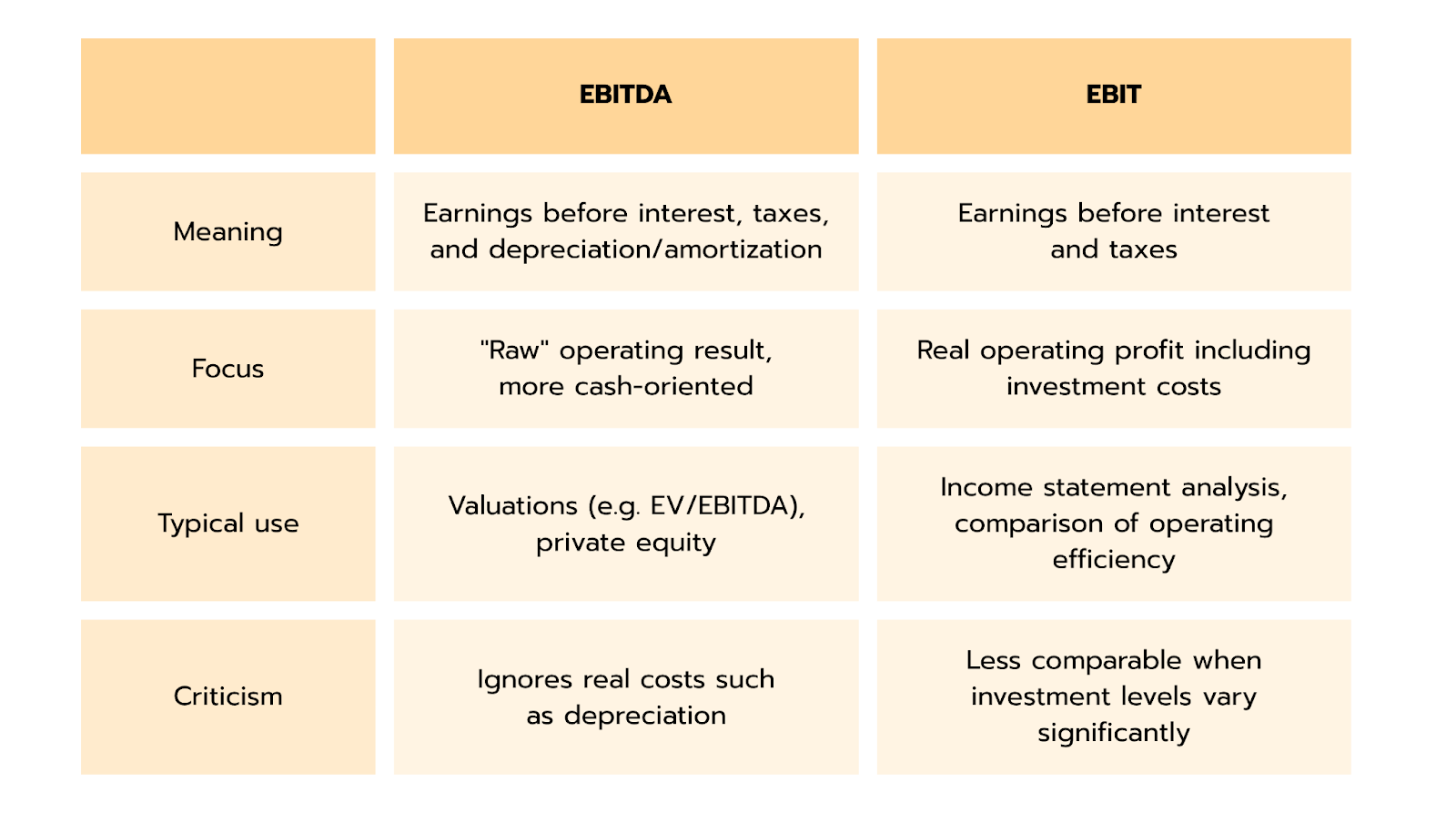

What’s the Difference Between EBIT and EBITDA?

As you now know, EBITDA shows how much a company earns from its core business before interest, taxes, and depreciation. EBIT, on the other hand, already includes depreciation and amortization, so it reflects a more realistic view of the actual operating profit after accounting for investment-related costs.

EBITDA is great when you want a quick, comparable view of operational strength, especially across companies with different investment levels or accounting treatments. But if you want to understand the true profitability, taking into account the wear and tear of assets and other investment costs, EBIT gives you a more complete picture.

To make the comparison even easier, we’ve summarized the key differences in this table:

Common EBITDA Questions in Finance Interviews

If you’re preparing for finance interviews, make sure you understand what EBITDA means, how to calculate it, and where its limitations lie. Typical interview questions include:

Why isn’t EBITDA a real cash flow metric?

Cash flow means actual money moving in or out of a business. EBITDA is just a calculated figure– it doesn’t include things like investments or changes in working capital, so it doesn’t show how much cash is truly left over.

When is EBITDA more useful than EBIT?

EBITDA makes more sense when companies have big differences in investment levels or depreciation. It shows profits without those effects, making it easier to compare businesses across different industries.

What are the risks of using EBITDA?

EBITDA can paint an overly positive picture because it ignores real costs like depreciation of equipment. That’s why it should never be looked at alone – always use other metrics too.

Why is EBITDA often used in private equity?

Private equity investors want to see how profitable a company’s core business is, without being affected by taxes, debt, or investments. EBITDA is a quick way to get that first impression.

Where can I find the data to calculate EBITDA in a financial report?

You’ll usually find depreciation and amortization info in the notes to the income statement or in the cash flow statement. Look for terms like “Depreciation,” “Amortization,” or simply “D&A.”

👉 You can practice these questions with our case question sets. Check them out!

Case Library

Discover more than 200 practice cases for every level and case type.

EBITDA reflects a company’s operational profitability without the distortions caused by depreciation, interest or taxes. It is particularly useful for comparisons and valuations, especially in capital-intensive industries or for companies with high investment activity.

You typically will not find EBITDA directly listed in the income statement, but you can calculate it by adding depreciation and amortization to EBIT. In interviews, you are often asked to explain how EBITDA differs from EBIT and what its strengths and limitations are.

Let's Move On With the Next Articles:

Present Value

Key Figures & Terms

Imagine someone offers you 100€, and you can choose: Do you want it today or one year from now? Most people would pick today. Why? Because you could already use the money now – spend it, invest it, or just keep it in your bank account. That simple idea is what the concept of Present Value is all about.

The Present Value helps you figure out how much a future payment is worth in today’s money. It shows you what a future amount would be worth if you had it right now.

The term Equity Value often comes up when talking about how companies are valued. But what exactly does it mean?

At its core, Equity Value represents the total value of a company’s equity or in other words, how much the ownership in the company is worth from the perspective of the shareholders.

For publicly traded companies, calculating Equity Value is straightforward: you simply multiply the current share price by the number of outstanding shares. For private companies, Equity Value is usually estimated through a business valuation process.

In both cases, the key question is: How much is the company worth to its owners?

If you're getting ready for a finance interview, you'll almost always come across a key term: Enterprise Value (or just EV). It might sound big and complicated at first, but once you understand it, it actually makes a lot of sense.

Put simply: Enterprise Value shows the total value of a company in the way a buyer would look at it if they wanted to purchase the entire business.

Imagine someone is buying a company outright. They wouldn't just look at the stock price. They’d take on the company’s debt but also benefit from its cash assets. That’s exactly what Enterprise Value reflects: Stock value + Debt – Cash balance.