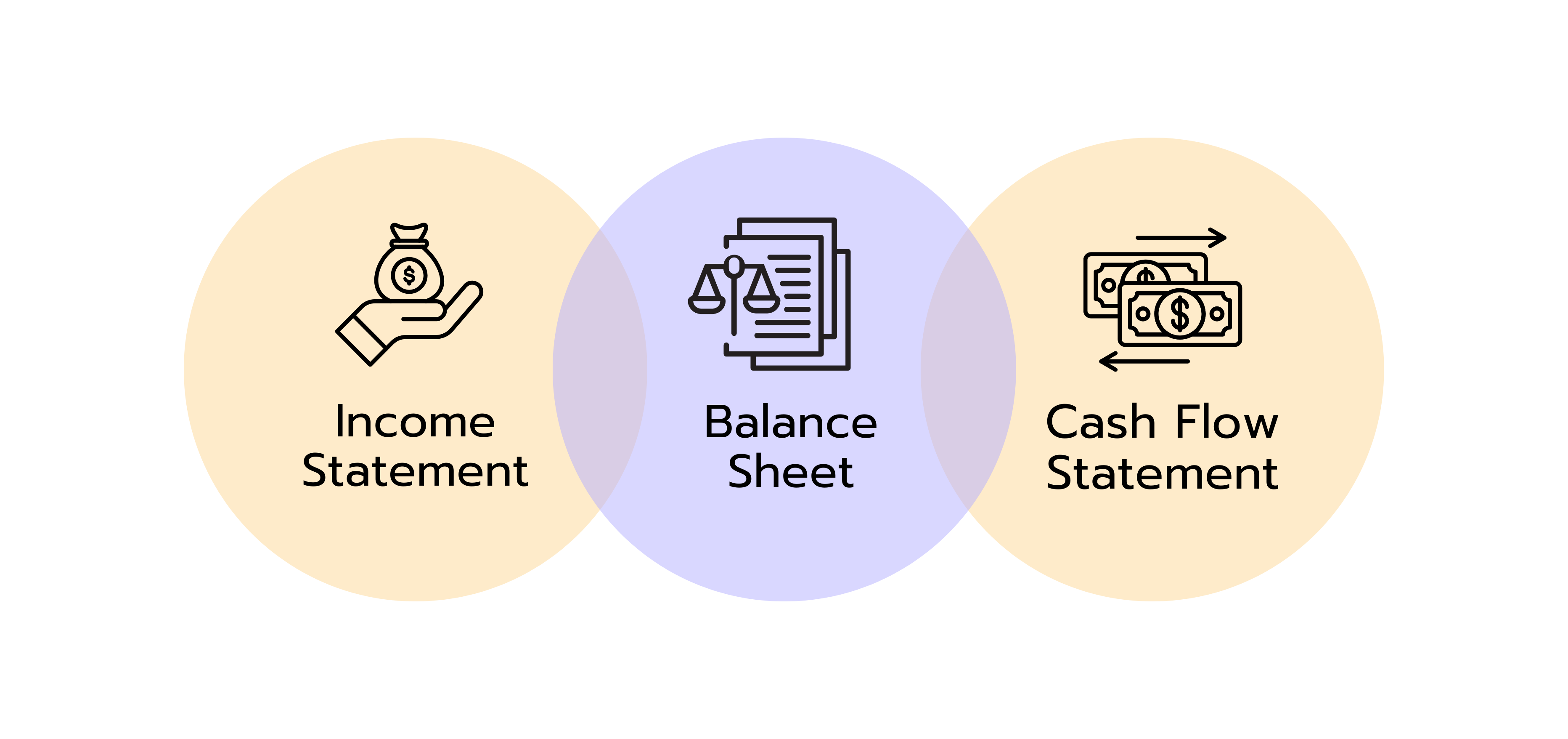

The balance sheet, also known as a statement of financial position, is one of the three most important financial statements. The other two are the income statement and statement of cash flow. Each has its purpose, but together they reveal the profitability, financial stability, and cash flow sustainability of a company.

As for the balance sheet, it gives you a clear view of what the company owns, what it owes, and what belongs to its owners. If you’re preparing for finance interviews, it’s important to understand the parts of a balance sheet, how to read and interpret it, and the common interview questions around it. Read on to learn everything you’ll need to be well-prepared and confident.

The balance sheet is a financial statement that shows a company’s assets, liabilities, and shareholders equity at a specific point in time. It’s usually prepared at the end of each month to provide a clear summary of a company’s financial health or position.

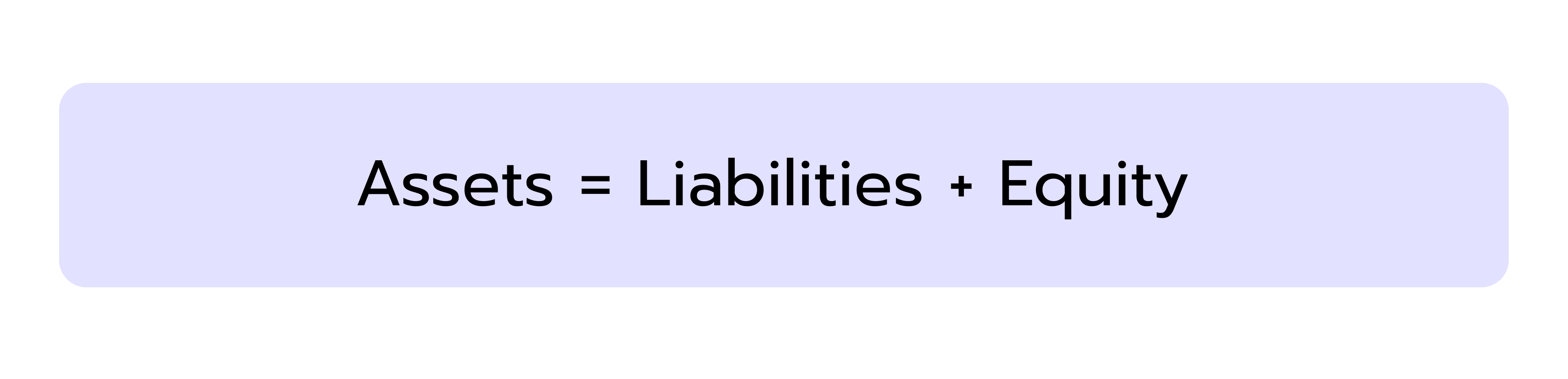

As the name suggests, a balance sheet should always be balanced. This means that the total value of what the company owns (assets) must always equal the combined total of what it owes to others (liabilities) plus what belongs to the owners (shareholders' equity). Therefore, the balance sheet equation is:

This equation comes from the basic principle that everything a company owns (its assets) is financed either by money it has borrowed (liabilities) or money invested by its owners (equity). If it’s balanced, the company’s accounts are accurate and it’s easier to see how stable or risky the organization’s finances are.

What Are the Most Important Elements in the Balance Sheet?

From the definition and balance sheet equation, you can pick up its main categories which are assets, liabilities, and equity. The details or exact line items for these parts may vary slightly from one company to another. However, if you understand what each section represents, you can read and analyze any balance sheet hassle-free.

Assets

The assets section in a balance sheet shows everything the company owns or controls that has economic value. These are divided into current and non-current assets. Current assets are those resources that can be converted into cash or used up within one year. Hence, they’re useful for funding daily operations and providing liquidity. They include:

Cash and cash equivalents

Accounts receivable (money owed by customers)

Inventory (goods available for sale)

Marketable securities (investments easily converted to cash)

Prepaid expenses (payments made in advance for services or goods)

Non-current assets are expected to provide value for more than one year as they support business operations and growth. Example include:

Property, Plant, and Equipment (PP&E), such as buildings and machinery

Intangible assets like patents, trademarks, and goodwill

Long-term investments

Deferred tax assets

On the balance sheet, assets are listed on the left side or top section depending on the structure. They’re arranged from most liquid, easily converted to cash, to least liquid. Current assets like cash and inventory appear first, followed by fixed assets like buildings and equipment.

Liabilities

These are everything the company owes to others. Like assets, liabilities are categorized as current and non-current. Current liabilities are short-term obligations due within one year, such as:

Accounts payable (money owed to suppliers)

Short-term loans or lines of credit

Accrued expenses (expenses incurred but not yet paid, like wages or utilities)

Unearned revenue (money received before delivering goods/services)

Non-current liabilities are debts or obligations due after one year, meaning longer-term financing and commitments. Examples include:

Long-term loans or bonds payable

Deferred tax liabilities

Pension obligations

Lease liabilities

The liability section reveals how much the company depends on external financing and what financial pressures it faces in the near and long term.

Shareholders’ Equity

Also known as owners’ equity, this is the value left over for the owners after all liabilities have been subtracted from assets. It’s what would be left for shareholders if the company were to liquidate all its assets and pay off all its liabilities. Equity includes:

Share Capital or Common Stock: The value of shares issued to investors.

Retained Earnings: The total amount of net income that has been retained in the business rather than distributed as dividends. It is accumulated profits reinvested in the company.

Additional Paid-In Capital: Capital received from shareholders above the nominal value of shares.

Treasury Stock: Shares the company has repurchased from shareholders (a contra equity account).

Accumulated Other Comprehensive Income: Gains or losses not included in net income but accounted for directly in equity, for instance foreign currency translation adjustments.

How to Read and Interpret the Balance Sheet

Once you understand the main elements of a balance sheet and how they’re structured, you’ll have an easy time reading any. However, interpreting it requires an understanding of the relationships between different elements and what they reveal about the company's financial strategy and health.

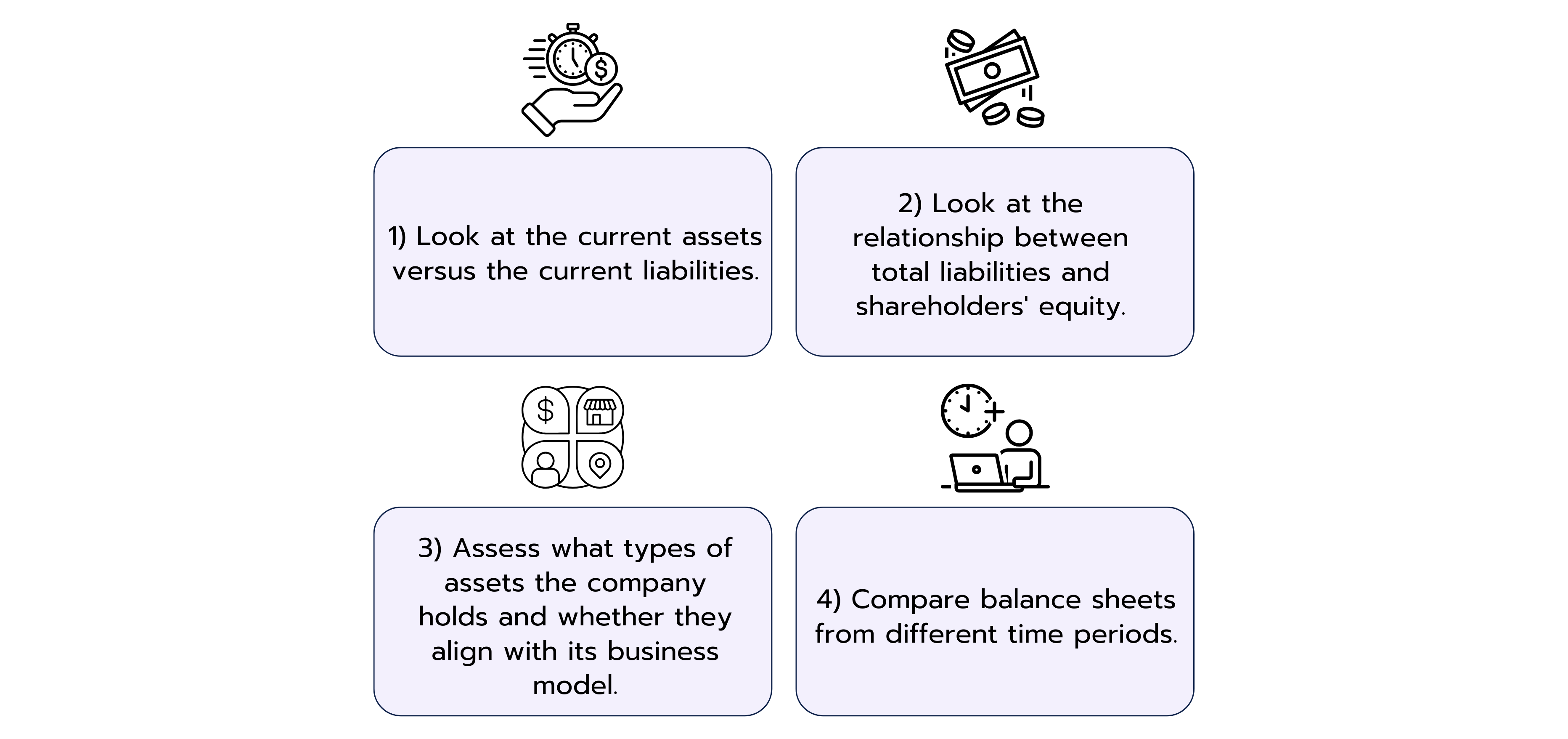

Start by looking at the current assets versus current liabilities to assess the company's ability to meet immediate obligations. If an organization has more current assets than current liabilities, then it has good short-term financial health. Pay special attention to cash levels, as this represents the company's most flexible resource for handling unexpected challenges or opportunities.

Then look at the relationship between total liabilities and shareholders' equity to understand how the company finances its operations. A company with high debt relative to equity may be taking on a huge financial risk, but it could also be using leverage strategically to fuel growth. Consider the types of debt as well. Short-term debt creates more immediate pressure than long-term financing.

You can also assess what types of assets the company holds and whether they align with its business model. A manufacturing company should have substantial equipment and inventory, while a service company might have more cash and receivables. Look for signs that assets are being used productively rather than sitting idle.

To get the full picture of a company’s financial position, compare balance sheets from different periods, for example, month to month or year to year. This shows trends, like whether the company is accumulating more assets, paying down debt, or increasing its equity.

In addition, you should make sure to also take the income statement and the cash flow statement into account in order to gain a comprehensive understanding of the company’s financial health.

Common Interview Questions About the Balance Statement

Most of the finance interview questions about the balance statement test your understanding of the financial statement including how the different elements interact with each other. Here are some interview questions about the balance statement to help you practice.

1. Walk me through the balance sheet.

The balance sheet is a financial statement that lists the company’s assets, liabilities, and equity. It follows the accounting equation:

Assets = Liabilities + Equity

Assets are what the company owns, liabilities are what it owes, and equity is the owners’ remaining interest after liabilities are deducted. Assets and liabilities are subdivided into current and non-current while equity consists of common stock, retained earnings, and sometimes treasury stock.

The assets are placed on the left side or top section of the balance sheet starting with the most liquid to the least liquid. Liabilities and equity appear on the right side or bottom, with current liabilities listed before long-term debt, and shareholders' equity at the end. This statement helps us understand financial health, liquidity, and capitalization.

2. How do you determine if a company is financially healthy just by looking at its balance sheet?

To determine if a company is financially healthy from the balance sheet, one should look at:

The proportion of current assets to current liabilities, which indicates liquidity and the company’s ability to meet short-term obligations without raising additional capital. A ratio above 1 typically suggests that the company has more readily available resources than near-term debts, while a low ratio could signal potential cash flow issues.

The total debt compared to equity, showing leverage and financial risk. A high debt-to-equity ratio may mean the company is heavily reliant on borrowed funds, increasing interest obligations and financial vulnerability, whereas a lower ratio often points to a more conservative capital structure.

Trends in equity over time, suggesting whether the company is building value for its shareholders. Consistently increasing equity can be a sign of profitable operations and reinvestment, while a declining trend may raise concerns about losses, dividend policies, or capital management.

A strong asset base, manageable debt, and growing equity, which together generally indicate good financial health. Tangible assets such as property, equipment, or inventory should be productive and aligned with the company’s business model, while debt should be structured in a way that supports growth without overleveraging.

However, it is also important to consider that the income statement and the cash flow statement are necessary for a complete assessment of a company’s financial health.

3. What is the difference between current and non-current assets/liabilities?

Current assets and liabilities are expected to be used, sold, or settled within one year, such as cash or accounts payable. Non-current or long-term assets and liabilities are those that will be held or owed for more than a year, like property, equipment, or long-term loans.

4. Why must a balance sheet always balance?

A balance sheet must balance because it is prepared under the double-entry accounting system, a fundamental principle in financial reporting that ensures every business transaction is recorded in at least two accounts, one as a debit and the other as a credit. This dual impact maintains the integrity of the accounting equation:

Assets = Liabilities + Shareholders’ Equity

The equation reflects that all the resources a company owns (assets) are financed either through borrowed funds (liabilities) or through the owners’ investments and retained earnings (equity). If the two sides of the balance sheet are not equal, it signals an error in the recording or classification of transactions, such as an omitted entry, a miscalculation, or a posting to the wrong account.

Balancing the statement is not just a mathematical requirement but also a validation of accuracy and completeness. It assures stakeholders that the company’s books are in order and that the reported financial position is reliable. A balanced sheet also facilitates better analysis of a company’s liquidity, solvency, and overall financial stability by providing a consistent, trustworthy snapshot at a specific point in time.

5. If a company purchases new equipment, how does that affect the balance sheet?

When a company buys new equipment, assets increase under property, plant, and equipment. If the purchase is made with cash, cash decreases by the same amount, keeping the balance sheet balanced. If it’s financed with a loan, liabilities increase instead of reducing cash.

6. What does negative shareholders’ equity mean?

Negative shareholders’ equity means the company’s liabilities exceed its assets. This can be a warning sign of financial distress or accumulated losses over time and may indicate that the company is at risk of insolvency if not addressed.

7. How would you use the balance sheet to assess a company’s liquidity or solvency?

To assess liquidity, one should look at the current ratio, current assets divided by current liabilities, to see if the company can cover short-term obligations. For solvency, the debt-to-equity ratio has to be examined to evaluate long-term financial stability and the company’s ability to meet its long-term debts.

8. What is working capital and why is it important?

Working capital is defined as current assets minus current liabilities. It’s a measure of a company’s short-term financial health and operational efficiency, indicating whether it has enough liquid assets to cover short-term liabilities. Positive working capital suggests good liquidity, which is essential for smooth day-to-day business operations.

9. How would a $10 increase in depreciation affect the three financial statements?

A $10 increase in depreciation expense reduces net income by $10 on the income statement because depreciation is an operating expense. On the cash flow statement, since depreciation is a non-cash charge, we add back the $10 to net income under operating activities, so cash flow is unaffected by this expense directly.

On the balance sheet, property, plant, and equipment (PP&E) is reduced by $10 due to accumulated depreciation, and retained earnings decrease by $10 due to lower net income.

10. Generally, Goodwill remains constant on the Balance Sheet. Why would it be impaired and what does Goodwill Impairment mean?

Goodwill is an intangible asset that arises when a company acquires another company for a purchase price that exceeds the fair value of its identifiable assets minus its liabilities. It reflects the added value the acquired company possesses beyond its tangible net assets. This may include brand recognition, customer relationships, a loyal customer base, skilled employees, technical know-how, or a strong market position.

Example: If a company pays €10 million to acquire another business whose identifiable net assets have a fair value of €8 million, the goodwill amounts to €2 million.

In the balance sheet, goodwill generally remains unchanged because it is not amortized under common accounting standards such as US GAAP or IFRS. Instead, companies perform regular impairment tests (Goodwill Impairment Tests). Goodwill impairment occurs when the carrying amount of goodwill on the balance sheet exceeds its current fair value.

Causes for impairment may include declining revenues of the acquired business, economic downturns in the industry, or a loss of market share.

👉 For more practice, check out our Case Library! There, you’ll find a wide range of practice questions to help you sharpen your finance skills.

Case Library

Discover more than 200 practice cases for every level and case type.

How Does the Balance Sheet Connect with the Income Statement and Cash Flow Statement?

The income statement shows profitability over a period, and its net income figure flows into the equity section of the balance sheet as retained earnings. The cash flow statement starts with net income and adjusts for non-cash items and changes in working capital from the balance sheet to show actual cash movement. Changes in balance sheet accounts influence the cash flow statement, and ending cash from the cash flow statement feeds back into the balance sheet as cash and cash equivalents.

Key Takeaways

The balance sheet is a financial statement that lists a company’s assets, liabilities, and equity. It tells you about the financial position, not performance. So you'll need to combine this information with income statements and cash flow statements to get the complete picture of how well the company is actually performing.

To assess a company's financial health from its balance sheet, focus on liquidity, solvency, and asset quality. Liquidity involves comparing current assets to current liabilities and calculating working capital to ensure short-term obligations can be met, while solvency is all about reviewing debt-to-equity ratios and total liabilities relative to shareholders' equity to evaluate long-term stability. Asset quality entails ensuring assets align with the business model, are being used productively, and tracking trends across multiple periods to identify improving or deteriorating patterns.

The key ratios and metrics from the balance sheet are:

Current Ratio: Current assets ÷ current liabilities (liquidity measure)

Working Capital: Current assets - current liabilities

Debt-to-Equity Ratio: Total debt ÷ shareholders' equity

The red flags to watch for when analyzing a balance sheet are negative shareholder equity, poor liquidity, and excessive debt compared to equity.

Let's Move On With the Next Articles:

Cash Flow Statement

Financial Statements

The cash flow statement is one of the three most important financial reports used by companies, alongside the balance sheet and the income statement. It shows how actual cash flows develop within a business, so when and how much money flows in or out of the company. This provides direct insight into a company’s liquidity and its ability to meet financial obligations.

Unlike the cash flow statement, the balance sheet and income statement are based on the accrual accounting principle. Under this approach, revenues and expenses are not recorded when cash changes hands but are instead assigned to the accounting period in which they are economically incurred.

In contrast, the cash flow statement is based on actual cash movements, therefore serving as a powerful tool in financial analysis. By focusing on real cash flows, it enables analysts to cut through the complexity of accounting and assess whether a company is truly generating cash or rather burning it.

In finance, Mergers & Acquisitions (M&A) refers to the process of mergers and corporate takeovers, where companies are combined or acquired to achieve strategic growth, greater efficiency, or competitive advantages.

In mergers and acquisitions (M&A), every deal has two sides: the sell-side and the buy-side. The sell-side team represents the seller and supports them in preparing the business for sale, reaching out to potential buyers, and negotiating the best possible price and terms. On the other side, the buy-side team works with the acquirer to identify attractive targets, evaluate them, and execute the purchase.

Investment banks and advisory firms often act on either side of a transaction. Most firms work on both buy-side and sell-side assignments across different deals, but never on both sides of the same transaction as that would create a conflict of interest. This guide will focus on the sell-side M&A process and provide sample interview questions to help you prepare for investment banking interviews.

In finance, Mergers & Acquisitions (M&A) refers to the process where companies are combined or acquired to achieve strategic growth, efficiency, or market advantages.

Mergers and acquisitions (M&A) transactions have a buy-side and a sell-side. The sell-side team represents the seller and works to market the business to potential buyers, while the buy-side team represents the acquirer. For the buyers or acquirers, the focus is on acquiring the right target with minimal risk and maximum strategic or financial upside. So it requires a lot of due diligence, valuation analysis, and strategic assessment.

Read on to understand the entire buy-side M&A process and get some practice questions to prepare for finance interviews.