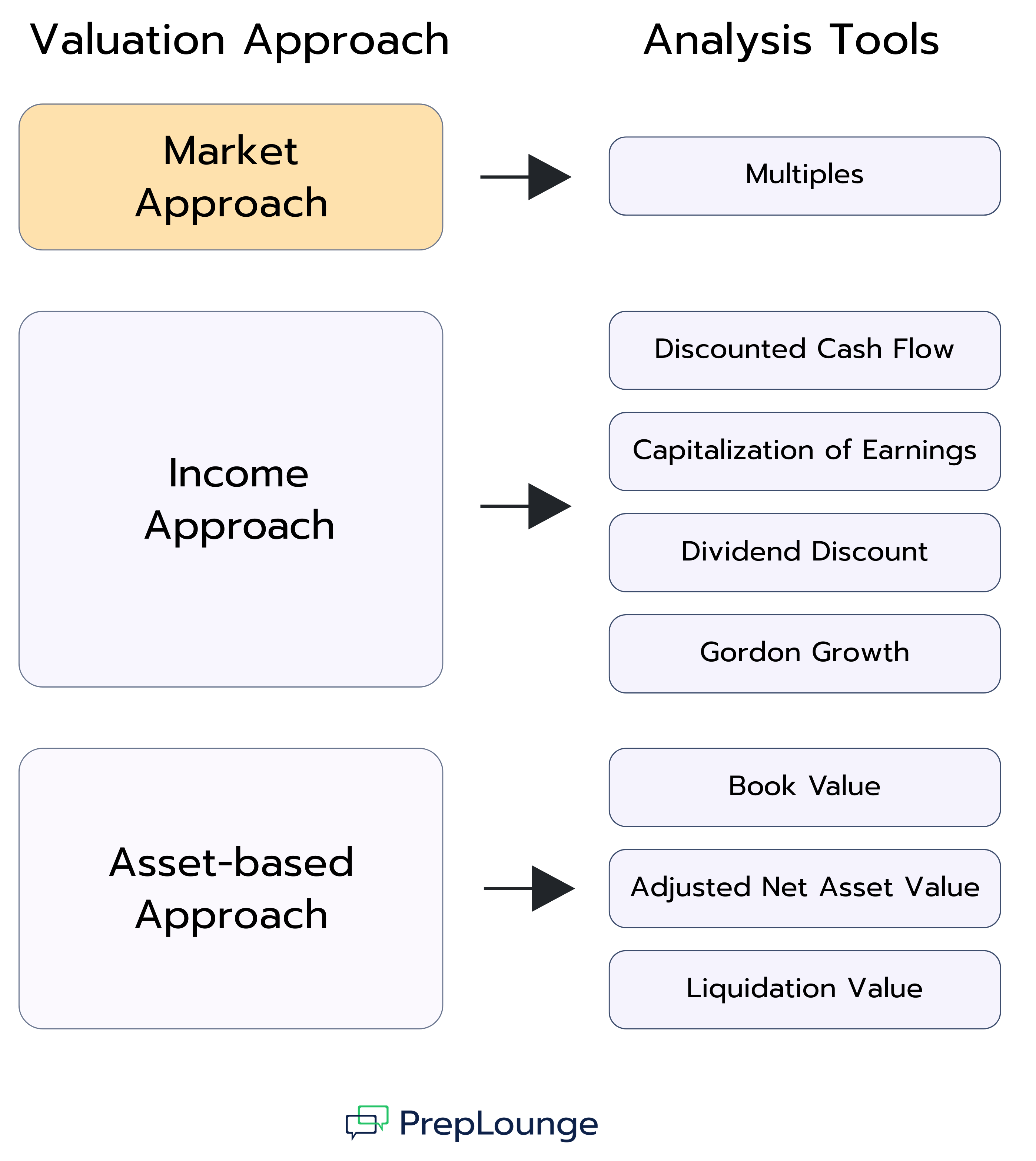

The market-based approach is one of the three primary methods of business valuation, alongside the income approach and the asset-based approach. Instead of projecting future earnings or adjusting balance sheet values, it determines value by comparing a company to similar businesses (Comparable Company Analysis) or transactions (Precedent Transactions Analysis) in the market. The underlying idea is straightforward: the market prices paid for comparable firms provide a benchmark for what the target company should be worth.

This approach typically relies on valuation multiples such as EV/EBITDA, P/E, or EV/Sales, derived from public company data or recent M&A deals. By applying these multiples to the target’s financials, analysts can estimate its market value under real-world conditions. The challenge lies in carefully selecting and interpreting the peer group, since differences in growth, risk, and profitability can significantly affect the outcome.

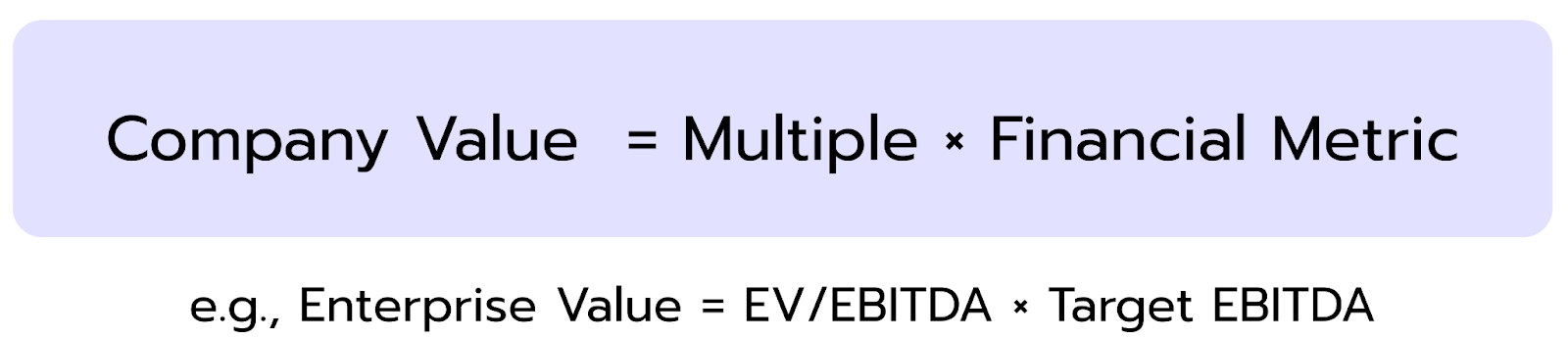

If comparable companies are valued at a certain multiple of revenue or earnings, then the target company should be worth approximately the same.

Analysts often adjust for differences in growth, profitability, size, or risk profile to improve accuracy.

Formula:

The market approach is implemented through two main methods:

Comparable Company Analysis (CCA): based on trading data from public companies

Precedent Transactions Analysis (PTA): based on acquisition prices from previous M&A deals

Both methods rely on the same principle but use different data sources. Analysts must carefully select relevant peers, normalize financial metrics when needed, and interpret the results in the context of control premiums, market sentiment, and outliers.

Comparable Company Analysis (CCA)

Comparable Company Analysis (CCA) estimates the value of a business by comparing it to publicly traded companies with similar characteristics. These peers are selected based on similarities in size, industry, region, and growth profile.

Once the peer group is defined, analysts calculate key valuation multiples such as EV/EBITDA, P/E, or EV/Sales. These multiples express the relationship between a peer company’s market value and its financial performance. A representative multiple, typically the median or average, is then applied to the target company’s financials.

For example, if the peer group has a median P/E (price-to-earnings) ratio of 10x and the target company’s net income is €20 million, the implied market value would be €200 million.

Precedent Transactions Analysis (PTA)

Precedent Transactions Analysis (PTA) estimates a company’s value based on prices paid in previous M&A transactions involving similar businesses. It uses the same types of multiples as CCA but draws them from completed deals instead of current stock prices.

Because these prices reflect what buyers actually paid, they often include control premiums and expectations of synergies. This typically results in higher valuation estimates compared to CCA.

When to Use Comparable Company Analysis vs. Precedent Transactions Analysis

While both CCA and PTA rely on market-based multiples, they differ significantly in their data sources and application context.

Comparable Company Analysis is typically used when valuing a company under ongoing operations or for benchmarking purposes. It is based on real-time trading data and reflects how the market currently values similar public companies. This method is especially useful when reliable peer data is available and there is no immediate M&A event. CCA is also preferred when consistent, up-to-date information is needed, for example, in equity research, fairness opinions, or internal corporate planning.

Precedent Transactions Analysis, on the other hand, is best suited for M&A scenarios. It helps estimate what buyers have historically paid for comparable businesses and provides insight into actual deal-making behavior, often including control premiums and expected synergies. However, PTA depends on access to reliable transaction data, and analysts must carefully consider deal-specific factors like timing, deal structure, and market conditions.

In short, CCA provides a snapshot of public market sentiment, whereas PTA offers insight into dealmaking behavior and acquisition pricing.

Reasons Why You Should Know the Market Approach

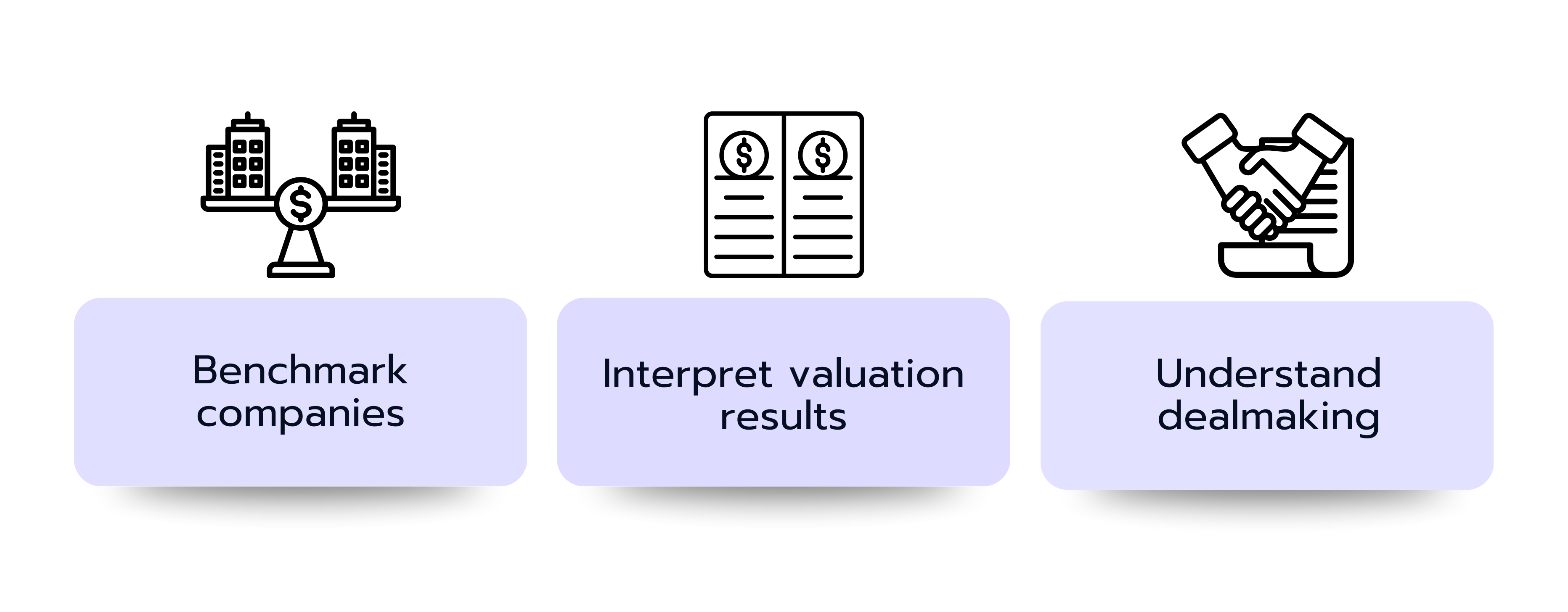

In finance interviews, you’re often expected to value a company without building a full model. That’s where the market approach comes in. Knowing how to use it gives you a real edge:

You can benchmark companies quickly using public data.

You can explain valuation outcomes without relying on forecasts.

You can show that you understand what drives real-world dealmaking.

Common Interview Questions About the Market Approach

We’ve selected three typical questions you might face in interviews, with short and simple answers to help you feel confident and well-prepared.

1. What is the market approach in company valuation?

The market approach estimates value by comparing a company to similar businesses. It uses valuation multiples like EV/EBITDA, P/E, or EV/Sales, taken from public peers (CCA) or past M&A deals (PTA).

2. What’s the difference between Comparable Company Analysis (CCA) and Precedent Transactions Analysis (PTA)?

CCA is based on real-time trading data from public companies and reflects investor sentiment. PTA uses actual deal prices and includes control premiums, so it often results in higher valuations.

3. When is the market approach especially useful?

It’s most helpful when reliable market data is available and internal forecasts are uncertain, for example, during M&A transactions, IPO planning, or benchmarking exercises.

👉 Want to practice more valuation questions? You’ll find a full set in our case library.

This set of questions is designed to help you prepare for the most common valuation topics in finance interviews. It covers the basics (like DCF, comparables, and multiples) but also includes practical scenarios that test whether you can apply these concepts in context.

Set aside about 30–35 minutes to go through everything. For each question, you’ll find a clear model answer to check your reasoning and deepen your technical knowledge.

This question set helps you go beyond the basics of valuation by comparing key methodologies and exploring when and how to use each one effectively. You’ll review core approaches like DCF, comparables, and precedent transactions, and build on that with LBO analysis, liquidation valuation, and industry-specific multiples.

You should expect to spend 30–40 minutes on the full set. Use the model answers to check your reasoning and refine your technical knowledge.

This question set helps you strengthen your valuation fundamentals by covering core techniques used in public and private company valuation, tax asset treatment, and sector-specific approaches. You'll explore how to estimate acquisition premiums, work with Net Operating Losses, and understand how valuation frameworks shift for financial institutions and resource-based companies like oil & gas firms.

You should expect to spend 25–35 minutes on the full set. Use the model answers to check your understanding, refine your technical explanations, and practice communicating complex valuation topics clearly and confidently in interview settings.

The market approach offers a practical and objective method to estimate a company’s valuation by comparing it with how similar firms are priced in real-world markets. It uses valuation multiples, such as EV/EBITDA, P/E, or EV/Sales, which are either derived from trading data of publicly listed peers (Comparable Company Analysis, CCA) or from actual transaction prices in completed M&A deals (Precedent Transactions Analysis, PTA).

CCA provides insight into how investors currently value similar businesses, offering a live reflection of market sentiment. PTA, on the other hand, illustrates what strategic buyers have been willing to pay in the past, often including control premiums and synergies. This makes PTA especially useful in acquisition or exit scenarios.

The reliability of the market approach hinges on selecting truly comparable peers, interpreting multiples accurately, and adjusting for differences in size, risk, or growth potential. This makes it especially valuable in situations where internal forecasts are uncertain, but reliable market data is available, such as in IPO planning, M&A transactions, or internal performance benchmarking.

Let's Move On With the Next Articles:

Income Approach

Valuation Models

The income approach is one of the three primary asset and company valuation methods. The other two are market approach and asset-based approach. These categories are based on the sources of inputs and valuation processes.

Within each of these major categories, there are several valuation methods professionals use. This guide will focus on the income approach, including related sample interview questions.

[Diagram showing valuation approaches and related analysis tools. Market-based approach links to Multiples. Income-based approach links to Discounted Cash Flow (DCF), Capitalization of Earnings, Dividend Discount Model (DDM), and Gordon Growth Model (GGM). Asset-based approach is listed but not linked to a specific tool.]

The asset-based approach to company valuation is one of the three primary methods used in finance, alongside the income approach and the market approach. While the income approach values a business based on future cash flows and the market approach relies on valuation multiples to compare companies, the asset-based approach looks directly at the balance sheet. It adjusts a company’s assets and liabilities to their current fair market value, with the difference representing the company’s net asset value (NAV).

This guide explains how the asset-based approach works, outlines its main variants such as book value, adjusted net asset value, and liquidation value, and shows in which situations it is most relevant. You will also find examples of common finance interview questions on this valuation method, as the asset-based approach frequently appears in interviews and assessments for roles in investment banking and corporate finance.

[Graphic showing three main valuation approaches with their corresponding analysis tools. The Market Approach leads to Multiples. The Income Approach leads to Discounted Cash Flow, Capitalization of Earnings, Dividend Discount, and Gordon Growth. The Asset-based Approach leads to Book Value, Adjusted Net Asset Value, and Liquidation Value. The layout displays each approach on the left and its tools on the right, connected by arrows. PrepLounge branding appears at the bottom]

Multiples are a key analysis tool within the market-based valuation approach. Instead of projecting a company’s future cash flows, this method determines value by comparing a business to similar companies or past transactions. The idea is simple: if comparable firms trade at certain valuation ratios, such as EV/EBITDA or P/E, the target company should trade at a similar level.

This makes multiples a relative valuation method, in contrast to income-based approaches like the Discounted Cash Flow (DCF) analysis, which estimate intrinsic value by discounting future cash flows. By focusing on observable market data, multiples provide a quick and practical way to assess value, but they also depend heavily on finding truly comparable companies or deals.

[Diagram showing valuation approaches and related analysis tools. Market-based approach links to Multiples. Income-based approach links to Discounted Cash Flow (DCF), Capitalization of Earnings, Dividend Discount Model (DDM), and Gordon Growth Model (GGM). Asset-based approach is listed but not linked to a specific tool.]