The Residual Income Model (RIM), similar to the Dividend Discount Model (DDM) or the Discounted Cash Flow (DCF) approach, is a method of company valuation. Unlike these models, the RIM focuses on whether a company earns profits that exceed its cost of equity.

This shows whether a company truly creates value for its shareholders and helps investors assess whether a stock is overvalued or undervalued.

The Residual Income Model (RIM) is used to determine the intrinsic value of a company’s equity. It is based on the concept of residual income, the portion of profit that remains after deducting the cost of equity.

The cost of equity reflects the return investors expect as compensation for the risk of owning the company’s shares. Residual income helps assess whether a company earns more than its cost of capital and therefore creates real value for its shareholders.

The calculation follows two steps. The first step is to determine the residual income for each year.

The formula for the Residual Income Model is: Residual Income = Net Income – Equity Charge Where: Equity Charge = BV of Equity × Cost of Equity

Net income refers to the company’s profit after taxes, taken directly from the income statement

The book value of equity is taken from the balance sheet and serves as the model’s starting point

The cost of equity represents the minimum rate of return investors expect for holding the company’s stock. It is usually estimated using the Capital Asset Pricing Model (CAPM)

The equity charge refers to the total amount of profit the company must generate to meet that required return. It is calculated by multiplying the cost of equity by the book value of equity

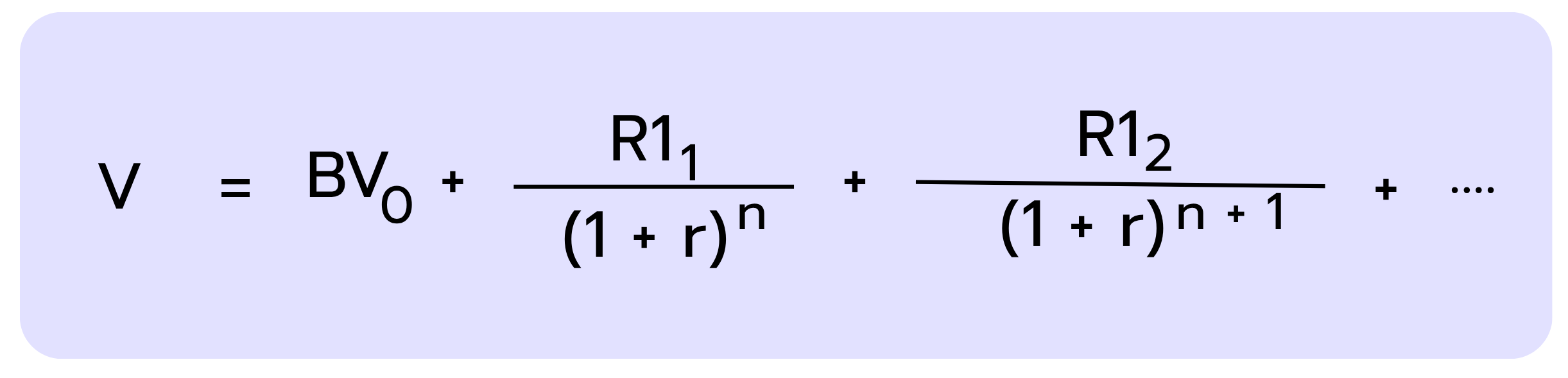

Once the residual incomes for each period have been calculated, the value of equity (V) can be determined. The Residual Income Model (RIM) assumes that this value equals the book value of equity plus the present value of all future residual incomes.

The following formula summarizes this concept:

Where:

BV= Present book value of equity

RI= Future residual income

r = Cost of equity

n= Number of periods in the future

Example: Calculating Intrinsic Equity Value with RIM

The following example illustrates how the Residual Income Model (RIM) is applied in practice. Step by step, it shows how the company’s equity value is derived from the book value of equity and the present value of future residual incomes, starting with the cost of equity.

Assume the following data:

BV= $500 M

Expected Net Income (next year)= $80 M

r= 12 %

Residual Income growth rate= 3 % per year

Step 1: Calculate the Equity Charge

In the first step, the required return on the company’s equity is calculated. This amount will later be subtracted from the net income to determine the residual income.

Step 2: Calculate the Residual Income (Year 1)

The residual income shows how much profit remains after subtracting the cost of equity.

Step 3: Estimate the Value of Residual Income

To calculate the total value, future residual incomes are discounted back to their present value.

Instead of forecasting each year separately, it is assumed that the residual incomes grow by 3 % per year. This assumption represents a simplified yet common approach in practice, as constant growth makes the calculation much easier and is frequently used in valuation models. Using a growth formula, the value of all future residual incomes can be determined at once:

Step 4: Add Book Value and Residual Incomes

The current book value and the present value of residual incomes together make up the estimated intrinsic equity value of the company.

The company’s intrinsic equity value is therefore $722.2 M.

When to Use the Residual Income Model

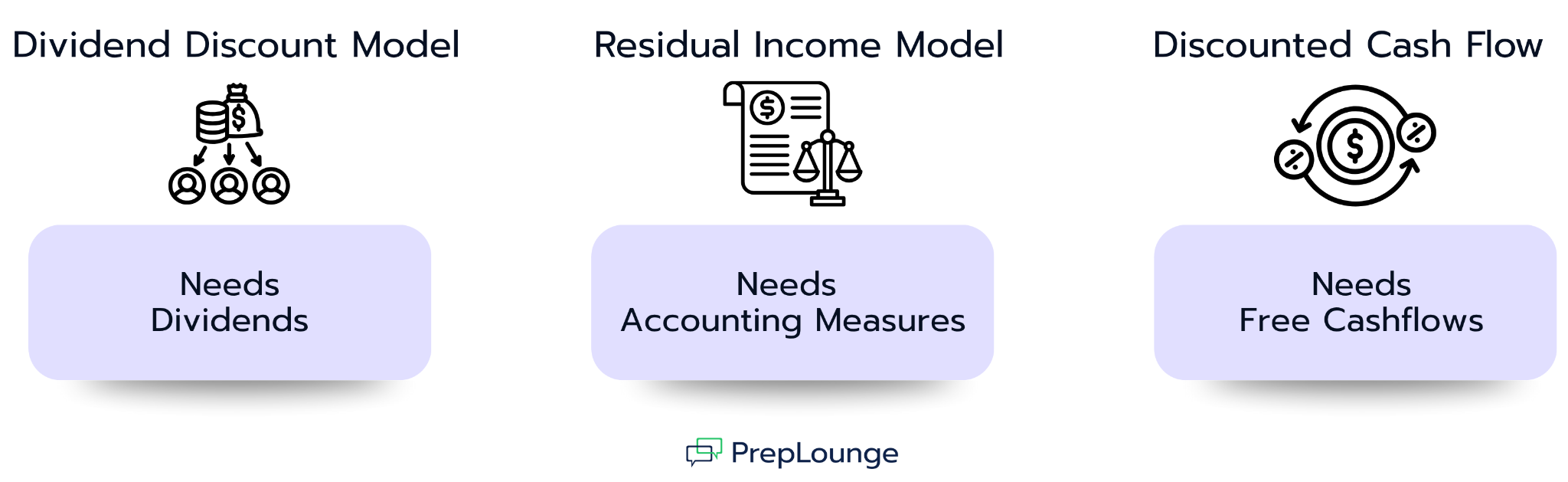

The Residual Income Model (RIM) is particularly useful when a company does not pay dividends or when future cash flows are difficult to forecast. In such cases, it provides a practical way to determine a company’s value.

While the Dividend Discount Model (DDM) is based on dividends and the Discounted Cash Flow (DCF) approach relies on long-term cash flow projections, the RIM uses accounting figures such as the book value of equity and net income.

The following chart illustrates this difference:

A major advantage of the Residual Income Model (RIM) is that it is less sensitive to uncertain forecasts. The model can be applied even when future cash flows are difficult to predict, for example in companies with volatile earnings or a strong dependence on economic conditions.

However, this requires reliable and transparent financial statements Because the valuation is based on the book value of equity, its accuracy strongly depends on the quality of the reported data.

The Residual Income Model (RIM) is particularly common in the banking and insurance industries, where financial statements tend to be highly reliable due to strict regulation and regular audits. These sectors rely heavily on measurable indicators such as equity and net income, while dividends and cash flows often fluctuate and are harder to predict. As a result, the RIM offers a stable and practical way to assess value, especially when traditional methods like DDM or DCF are less reliable.

Strengths and Weaknesses of the Residual Income Model

Like any valuation tool, the Residual Income Model has distinct advantages and limitations.

Strengths of the RIM

Weaknesses of the RIM

Works well even when dividends or cash flows are hard to forecast

Dependent on accounting numbers, which can be manipulated

Relies on information from financial statements, usually easy to access

Requires estimating the cost of equity, which is subjective

Explicitly factors in the cost of equity and shows whether a company is creating value for shareholders

Less effective for asset-light firms with significant intangibles

Common Interview Questions on the Residual Income Model

Here are some of the most common interview questions about the Residual Income Model to help you practice.

1. What is Residual Income, and how is it different from Net Income?

Residual income shows how much profit a company earns after subtracting the return expected by investors. In other words, it measures the value created beyond the required minimum return.

In contrast, net income is the company’s total profit for the year and does not take into account that shareholders’ equity also carries an expected return.

2. Why might you use the Residual Income Model for a bank or insurance company?

Industries such as banking and insurance are particularly well suited for the Residual Income Model (RIM), as their balance sheet data are highly regulated, transparent, and reliable. Their business models are based on clearly measurable financial indicators such as equity and profit, while cash flows and dividends often fluctuate and are difficult to predict. This makes it possible to estimate a company’s value using the RIM more accurately and consistently than with other valuation approaches.

3. When would you prefer the Residual Income Model over a DCF analysis?

The Residual Income Model (RIM) is particularly useful when cash flows or dividends are difficult to forecast or fluctuate significantly over time. In such cases, DCF or DDM analyses often produce unstable results, as they depend on reliable projections of distributions or cash flows.

The RIM provides a more practical alternative, since it relies on book values and earnings, which are generally easier to predict and more readily available.

4. What does the result of a Residual Income Model valuation show?

The result of the Residual Income Model (RIM) represents the intrinsic value of a company’s equity. This value can be compared to the current market price to assess whether a stock is overvalued or undervalued. If the calculated intrinsic value is higher than the market price, the stock may be undervalued; if it is lower, the stock could be overvalued.

👉 Want to practice more valuation questions? You’ll find a full set in our case library.

You’re working on a DCF valuation for CloudCore Inc., a publicly traded cloud computing company. You’ve built a standard unlevered DCF model using a WACC of 10% and based on your 5-year forecast, the Enterprise Value (EV) currently comes out to $200 million.

This question set helps you strengthen your valuation fundamentals by covering core techniques used in public and private company valuation, tax asset treatment, and sector-specific approaches. You'll explore how to estimate acquisition premiums, work with Net Operating Losses, and understand how valuation frameworks shift for financial institutions and resource-based companies like oil & gas firms.

You should expect to spend 25–35 minutes on the full set. Use the model answers to check your understanding, refine your technical explanations, and practice communicating complex valuation topics clearly and confidently in interview settings.

You’re advising FreshHarvest AG, a fast-growing food distribution company based in Germany. They operate on tight margins, high volumes, and have recently secured several new retail partners. The CFO wants to better understand how working capital decisions and seasonal dynamics impact their free cash flow profile and ultimately their valuation.

Your task is to assess how working capital evolves over the forecast period, how payment term shifts affect cash flow, and how to reflect seasonality in a dynamic forecasting model.

This case will test your analytical skills, cash flow understanding, and judgment around operational finance levers.

The Residual Income Model (RIM) estimates the intrinsic value of a company’s equity by adding the present value of future residual incomes to the current book value of equity. Residual income is calculated as net income minus the cost of equity and shows whether a company earns more than the minimum return expected by investors.

The model is particularly useful when no dividends are paid, when cash flows are difficult to forecast, or when reliable balance sheet data are available - for example, in the banking and insurance sectors.

One advantage of the RIM is that it relies on accounting figures that are easy to obtain and makes value creation beyond net income visible. However, its accuracy depends on the quality of financial statements and on the assumptions regarding the cost of equity and long-term growth.