A Leveraged Buyout (LBO) is a type of acquisition where a buyer chooses to finance the purchase using borrowed money or debt and some cash investment, known as equity. So, the "leverage" in leveraged buyout refers to this heavy use of debt financing. In most LBOs, 60-90% of the purchase price comes from borrowed money, while only 10-40% comes from the buyer's own cash.

The buyer uses the future cash flows and assets of the company being acquired as collateral for the loans. They can also use the assets of the acquiring company if necessary. Over time, the debt is paid back using the cash that the target company generates. The buyers aim to exit profitably through a sale, merger, or public offering after improving the company's performance and paying down the debt.

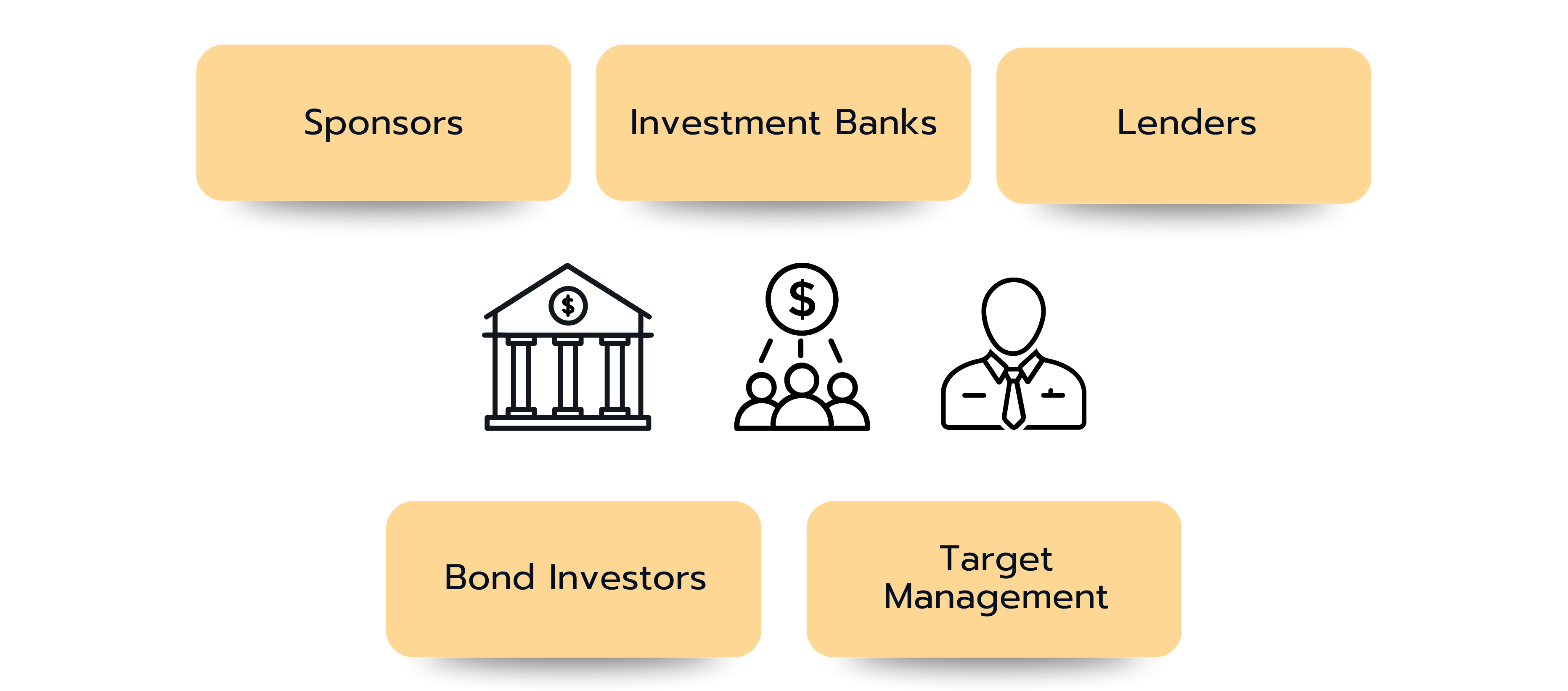

LBO transactions are complex and involve several participants such as sponsors, investment banks, lenders, bond investors, and target management.

To help you see the role of each participant clearly, we will use the largest LBO ever as an example. This was the 2007 acquisition of TXU, later renamed Energy Future Holdings, by KKR, TPG, and Goldman Sachs Capital Partners for about $45 billion.

Sponsors (Private Equity Firms)

The primary participants in an LBO are sponsors or private equity firms. These are the firms that want to acquire a company using huge debt. They put in equity, arrange financing, and ultimately aim to sell the company at a profit.

In the TXU acquisition case, the sponsors were KKR, TPG, and Goldman Sachs Capital Partners who put in the equity portion. Their goal, as with any LBO, was to improve operations and later sell the company at a profit.

Investment Banks

Working alongside the sponsors are investment banks, which advise on valuation, help structure the deal, and often assist in raising the necessary debt.

For the TXU acquisition, Credit Suisse and Lazard were the advisors to the buyers while Citigroup, Goldman Sachs, and JP Morgan committed to providing the debt necessary for the deal. These investment banks helped arrange the $40 billion in debt used to finance the majority of the $45 billion acquisition.

Lenders

Another key player in a leveraged buyout (LBO) is the lenders, typically commercial banks or specialized credit funds. They provide debt capital and expect regular interest payments as well as the repayment of the principal. Various types of loans with different maturities, interest rates, and risk profiles are used in the process. The general rule is: the more subordinated and unsecured a loan is, the higher the risk and interest rate.

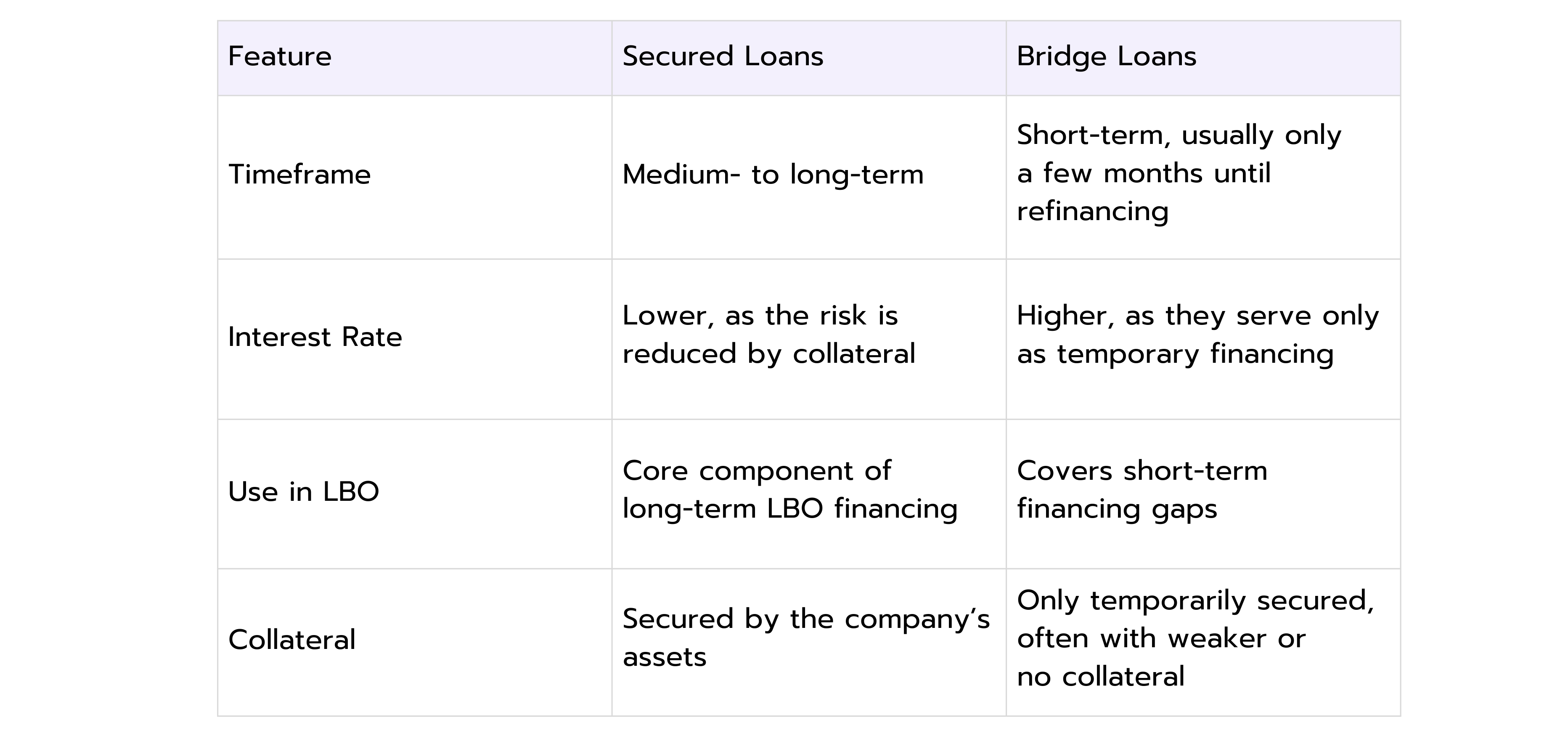

In the 2007 TXU acquisition, the debt financing consisted of two main types of loans:

Secured bank loans (approx. $24.5 billion): These loans were backed by TXU's assets, such as real estate and operating assets. If something went wrong, the banks could sell these assets to recover their money. This made the loans safer for lenders and resulted in lower interest rates. Secured loans thus formed the stable foundation of the LBO financing.

Bridge loans (approx. $11.25 billion): These so-called bridge loans were provided on a short-term basis to ensure the deal could close immediately. They acted as an advance until the company could later secure long-term loans or issue bonds on the capital markets. Because they are only a temporary solution and riskier for banks, they come with higher interest rates. They may be secured but are often less well-collateralized than long-term bank loans.

The following overview illustrates the exact difference between secured loans and bridge loans:

Bond Investors

In some cases, especially larger LBOs, sponsors often issue high-yield bonds, also called "junk bonds", to institutional investors like pension funds, insurance companies, and hedge funds. These investors buy bonds that pay higher interest rates because they're taking on more risk by lending to a highly leveraged company.

Target Management

The management team of the company being acquired plays a crucial role as well. Sometimes they partner with the private equity sponsor in what is called a "management buyout" or MBO. In such a case, they invest their own money alongside the private equity sponsor. At other times the management team is retained post-acquisition to run the business. Their intimate knowledge of the company's operations is invaluable for both executing the deal and creating value afterward.

Characteristics of a Strong LBO Candidate

Not every company is a good fit for an LBO. A strong candidate has stable and predictable cash flows, because those cash flows are what will be used to repay the heavy debt burden. Companies that already have high levels of debt are less attractive, since there is less room to add new borrowing. A solid asset base is also useful, as assets can sometimes be used as collateral to secure loans.

Having low capital requirements is attractive as well because more of the cash flow can be directed toward debt repayment and value creation initiatives.

Another important characteristic of a strong LBO candidate is the potential for improvement. Private equity firms look for businesses where they can reduce costs, grow revenue, or otherwise increase efficiency. Also, having a capable and experienced management team is critical, since they are the ones who might execute the operational improvements needed to create value.

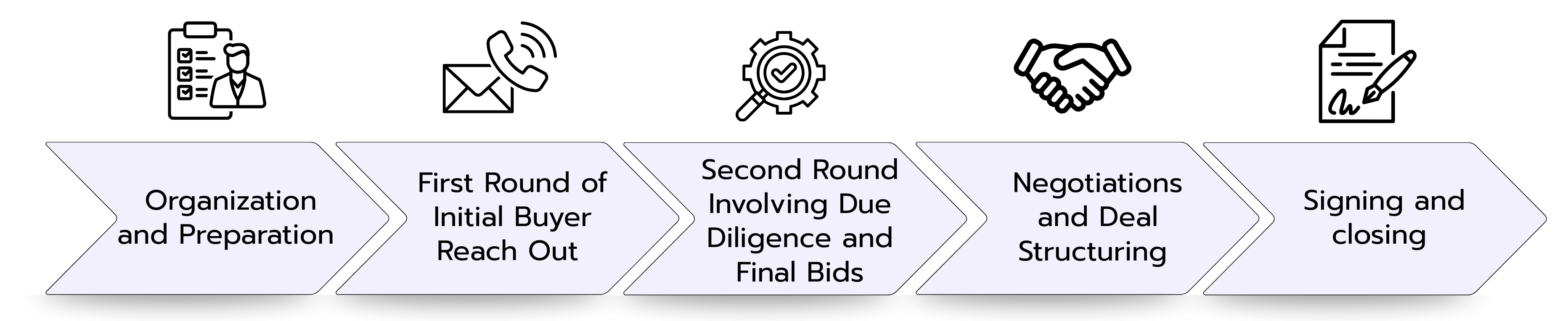

The LBO Deal Process

The process of executing an LBO follows structured steps. These include deal sourcing, target screening, initial valuation, due diligence, financing arrangement, negotiations, and deal closing.

Deal Origination and Screening in the LBO Process

The LBO process begins with deal sourcing, where private equity firms identify a potential target company. This can happen through various means like their own networks, or via auctions run by investment banks.

Once they identify a potential target, the sponsor submits an initial letter of interest which is non-binding. This is followed by management presentations where the target company's leadership presents their business, strategy, and financial projections to potential buyers.

With that information, the buyer’s team conducts an initial screening to see whether the company is a realistic candidate for an LBO. At this stage, they are checking for stable cash flows, manageable debt capacity, and the possibility of generating attractive returns. Most PE firms work with investment banks as their advisors throughout the LBO process.

Initial Valuation and Due Diligence in LBO

If the target passes the initial screen, the sponsor’s team builds a preliminary LBO model, which is a financial model that estimates how much debt the company can handle and what kind of returns might be achieved.

If the model looks promising, they move the deal into the due diligence phase, where the buyer’s team examines the financial statements, operations, legal risks, and the company’s competitive position in detail.

👉 In our case library, you’ll find numerous exercises on company valuation.

This set of questions is designed to help you prepare for the most common valuation topics in finance interviews. It covers the basics (like DCF, comparables, and multiples) but also includes practical scenarios that test whether you can apply these concepts in context.

Set aside about 30–35 minutes to go through everything. For each question, you’ll find a clear model answer to check your reasoning and deepen your technical knowledge.

This question set helps you go beyond the basics of valuation by comparing key methodologies and exploring when and how to use each one effectively. You’ll review core approaches like DCF, comparables, and precedent transactions, and build on that with LBO analysis, liquidation valuation, and industry-specific multiples.

You should expect to spend 30–40 minutes on the full set. Use the model answers to check your reasoning and refine your technical knowledge.

This question set helps you strengthen your valuation fundamentals by covering core techniques used in public and private company valuation, tax asset treatment, and sector-specific approaches. You'll explore how to estimate acquisition premiums, work with Net Operating Losses, and understand how valuation frameworks shift for financial institutions and resource-based companies like oil & gas firms.

You should expect to spend 25–35 minutes on the full set. Use the model answers to check your understanding, refine your technical explanations, and practice communicating complex valuation topics clearly and confidently in interview settings.

This set of questions focuses on IPO valuation using Stripe as an example. It tests your understanding of core valuation methods and your ability to apply them in realistic, interview-style scenarios.

Set aside 30–35 minutes for the whole set. Each question includes a model answer to check your approach and improve your technicals.

Meanwhile, the buyer’s team begins financing discussions with lenders and investment banks to determine how much debt they can raise and on what terms. This stage involves preparing detailed financial projections, negotiating loan terms, and sometimes pre-marketing high-yield bonds to investors.

Once the financing arrangements are in place, the sponsor submits a formal bid to acquire the company. Multiple PE firms and strategic buyers may submit bids in a competitive process, driving up the purchase price.

LBO Negotiations

After bidding, the sponsor enters negotiations with the seller to finalize details such as financing structure, deal terms, warranties, governance, and management incentives.

Signing and Closing of a Leveraged Buyout

When everything is agreed, the deal moves to signing and closing, where legal documents are executed, funds are transferred, and ownership officially changes hands. For the sponsor, this isn’t the end but the beginning of their work to improve the company and create value over their typical 3-7 year holding period.

Financing and Transaction Structure of a Leveraged Buyout

The financing of an LBO is usually a layered mix of debt and equity. At the top of the capital structure is senior debt, which is the safest type of loan for lenders and therefore carries the lowest interest rate. Senior debt has the highest priority for repayment and is usually secured by the company's assets.

Below that is subordinated or mezzanine debt, which is more expensive because it is riskier. This debt is "subordinated" because it gets repaid only after senior debt is satisfied. To compensate lenders for this additional risk, subordinated debt carries higher interest rates.

In some deals, the sponsor issues high-yield bonds, which are essentially loans from investors who expect higher interest payments in exchange for taking on more risk. These bonds have fixed interest rates higher than senior debt and longer maturities.

At the bottom of the LBO capital structure sits equity, provided primarily by the private equity sponsor. It represents 10-40% of the total financing and bears the highest risk. If the target company struggles, equity holders get paid last. However, equity also offers the highest potential returns if the investment succeeds.

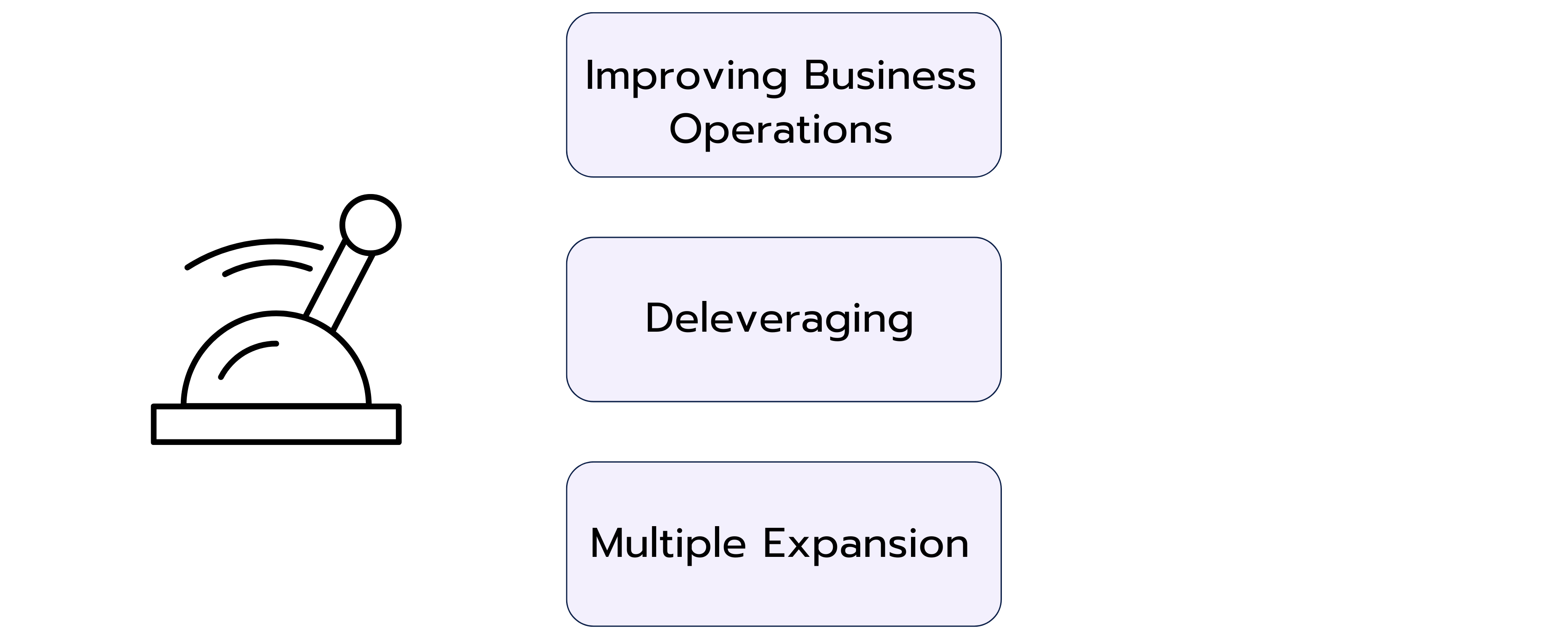

Economics and Value Creation in LBOs

LBOs continue to happen because private equity sponsors often make money. There are three primary sources of value creation that make this possible, often called the "three levers" of LBO returns.

The first and most sustainable source of value comes from actually improving the business operations. It might include cutting costs, improving efficiency, expanding into new markets, making strategic acquisitions, or implementing better management practices. When a private equity sponsor improves a company's EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) from $100 million to $150 million, they've created real, fundamental value.

The second lever is deleveraging, or paying down the debt over time. As the company reduces its debt, the equity ownership stake becomes more valuable. For instance, if a sponsor buys a company for $1 billion using $800 million of debt and $200 million of equity, and later sells it for $1.2 billion after paying down $100 million of debt, their equity has grown from $200 million to $400 million. That’s a 100% return, even though the company's value only increased by 20%.

The third is multiple expansion. It involves selling the company at a higher valuation multiple than the purchase price. For instance, if a PE firm buys a company at 8x EBITDA and sells it at 10x EBITDA, maybe because market conditions improved or they’ve made the company more attractive, they create value through this multiple expansion.

Ideally, all three levers should work together. In such a case, LBOs can generate returns of 20-30% annually for private equity sponsors, making them attractive investments despite the risks involved.

Common Interview Questions on LBO Transactions

LBO questions are quite common in investment banking and private equity interviews. It’s also important to understand the LBO model as a good number of questions center on it. Here are some of the most common LBO interview questions to help you practice and prepare.

1. What is an LBO (Leveraged Buyout)?

A Leveraged Buyout (LBO) is an acquisition in which most of the purchase price is financed with debt rather than equity. The target company itself serves as collateral for the loans: its assets can secure the debt, and its future cash flows are used to repay the borrowings over time. For private equity firms, this structure is attractive because it reduces the upfront equity required and significantly increases the potential return on their invested capital.

2. How does a simple LBO model work?

An LBO model is a financial model that simulates the entire leveraged acquisition process.

It begins with the purchase price of the company.

Then the “Sources and Uses” section shows where the money comes from (equity, bank loans, bonds) and how it is spent (purchase price, fees, refinancing existing debt).

Next, the model projects the company’s future cash flows to estimate how quickly debt can be repaid.

Finally, an exit is modeled, typically through a sale or IPO after several years.

The model outputs key metrics such as the Internal Rate of Return (IRR) and the Equity Multiple, which measure how profitable the deal would be for private equity investors.

3. What makes a company a good LBO target?

A strong LBO candidate usually has the following characteristics:

Stable and predictable cash flows, ensuring the company can service its debt.

Low capital expenditure (CAPEX) requirements, so more free cash flow is available for debt repayment.

Strong market position or competitive advantage, providing resilience against downturns.

Moderate existing leverage, so the company can handle additional debt.

Operational improvement potential, for example through cost savings, efficiency gains, or revenue growth.

4. Why do private equity firms use debt instead of paying entirely in cash?

Private equity firms deliberately use debt because it provides several advantages:

Return enhancement (leverage effect): With less equity invested upfront, even moderate improvements in company performance can translate into high equity returns.

Tax benefits: Interest payments on debt are tax-deductible, which lowers the company’s effective tax burden.

Risk sharing: A portion of the financial risk is transferred to the lenders.

By contrast, strategic buyers (such as industrial corporations) typically rely less on debt financing. Instead, they focus on synergies – opportunities to create value through cost savings, integration, or new revenue streams.

5. What factors drive returns in an LBO?

There are three main levers that determine returns in an LBO:

Operational improvements: Enhancing profitability by reducing costs, improving efficiency, or growing revenues increases both cash flow and company value.

Debt paydown (Deleveraging): Each year that debt is reduced, the equity portion of the company’s capital structure grows, giving investors a larger share of the company’s value at exit.

Multiple expansion: If the company can be sold at a higher valuation multiple (e.g., EV/EBITDA) than at entry, the exit price rises, boosting returns for investors.

👉 You are looking for more questions to get ready for your finance interviews? Check out our case library!

Case Library

Discover more than 200 practice cases for every level and case type.

An LBO is an acquisition strategy where a huge portion of the acquisition costs come from debt and a smaller portion from equity. The LBO process involves various steps like deal sourcing, target screening, initial valuation, due diligence, financing arrangement, negotiations, and deal closing.

Due to the complexity of the process, multiple parties work together over several months. Sponsors initiate and drive the deal, investment banks advise and help raise financing, lenders and bondholders provide capital, and the target’s management helps with the operations. The objective of an LBO is to enhance the value of the acquired company through operational improvements, cost-cutting, and financial restructuring. Then sponsors can exit profitably through a sale, merger, or public offering.

Let's Move On With the Next Articles:

EBIT

Key Figures & Terms

EBIT stands for Earnings Before Interest and Taxes.

Depending on the company or language, EBIT may also be referred to as:

- Operating Income or Operating Profit

- Earnings before Interest and Taxes (in German reports)

- Betriebsergebnis (commonly used in German-speaking regions

This metric shows how much a company has earned from its core operations before taking into account financing costs (interest) and taxes.

EBIT can also be described as operating result or operating profit. The aim is to assess a company’s operational performance on its own, without distortion from different financing methods or tax rates.

Why is this important? Because it allows you to compare companies independently of one another. Whether a company has taken out many loans or benefits from a particularly low tax rate does not affect its EBIT.

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It reflects a company’s earnings before taking into account interest payments, tax expenses, and non-cash items like depreciation and amortization. You can think of it as an extended version of EBIT that excludes all depreciation-related costs.

The idea behind this: depreciation and amortization are non-cash expenses and often influenced by accounting methods, assumptions, or company policies. By stripping them out, EBITDA aims to provide a clearer picture of a company’s ongoing operational performance, regardless of how much has been invested or how assets are accounted for.

Imagine someone offers you 100€, and you can choose: Do you want it today or one year from now? Most people would pick today. Why? Because you could already use the money now – spend it, invest it, or just keep it in your bank account. That simple idea is what the concept of Present Value is all about.

The Present Value helps you figure out how much a future payment is worth in today’s money. It shows you what a future amount would be worth if you had it right now.