Retained earnings are the portion of a company’s net income that is not distributed to shareholders as dividends, but instead reinvested in the business. This process, often called retaining earnings, allows profits to accumulate over time. On the balance sheet, these accumulated profits appear in the shareholders’ equity section as retained earnings.

By keeping profits inside the company, management can finance growth, reduce debt, or build reserves for future investments. In company valuation, retained earnings are important because they connect profitability, dividend policy, and long-term growth potential.

For a finance interview, you should be able to explain both perspectives: retained earnings as an ongoing process of reinvesting profits and as a balance sheet item that reflects a company’s internal financing capacity.

At the end of each year, a company generates net income. Management decides how much of this profit is paid out as dividends and how much is kept as retained earnings. The retained portion is added to the retained earnings balance in the shareholders’ equity section of the balance sheet.

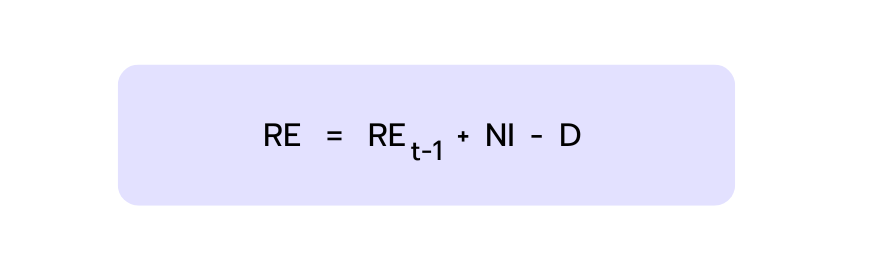

Retained Earnings Formula:

Example calculation:

RE (t-1)(Previous Retained Earnings): $100M

NI (Net Income): $50M

D (Dividends): $20M

At the end of the year, the company has $130 million in retained earnings.

In simple terms: companies can either pay out profits to shareholders or keep them to support future growth.

Why Retained Earnings Matter in Finance

Retained earnings show how a company allocates its profits: either by rewarding shareholders through dividends or by reinvesting in future growth. High retained earnings signal strong internal financing capacity and financial flexibility, while low or negative retained earnings (accumulated losses) may indicate weak profitability and reliance on external funding.

For investors and financial analysts, retained earnings are also a measure of capital allocation. They help assess whether management is using profits effectively to create long-term value or simply holding on to cash.

At their core, retained earnings illustrate how companies balance short-term shareholder payouts with long-term reinvestment and value creation.

Retained Earnings in Valuation Models

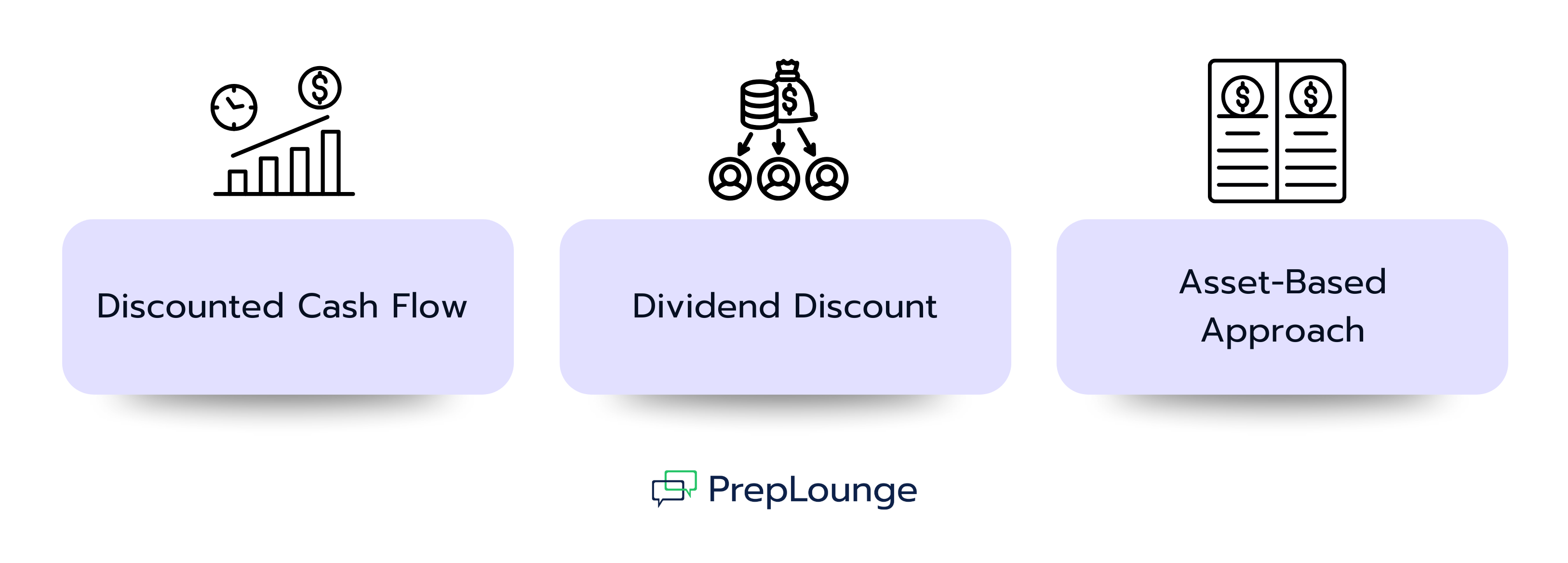

Retained earnings are not a standalone valuation method, but they play a key role in how common models are applied.

In the Dividend Discount Model (DDM), payout policy is central. If a company retains more profits, current dividends are smaller, but future dividends can grow faster because more capital is reinvested.

In the Discounted Cash Flow (DCF) model, retained earnings provide internal financing for reinvestments. Instead of raising new equity or debt, the company uses retained profits to expand operations, which increases future free cash flows.

In the Asset-Based Approach, retained earnings appear in the equity section of the balance sheet. Over time, accumulated retained earnings raise book value, which forms the foundation of this valuation method.

These examples show that retained earnings influence multiple aspects of company valuation. By determining how profits are allocated and how much capital stays inside the business, retained earnings directly shape assumptions about growth, financing, and long-term value creation.

Common Interview Questions About Retained Earnings

Below are typical finance interview questions related to retained earnings, including short answers to help you prepare effectively.

1. What Are Retained Earnings?

Retained earnings are the accumulated portion of a company’s net income that is kept instead of being paid out as dividends. For example, if a firm reports $50m in net income and distributes $20m as dividends, the remaining $30m goes into retained earnings. Over time, this balance builds up under shareholders’ equity on the balance sheet.

2. How Do Retained Earnings Affect Valuation?

Retained earnings play a central role in company valuation because they determine how profits are used - either distributed as dividends or reinvested - and thereby directly shape a firm’s long-term growth potential.

In the Dividend Discount Model (DDM), higher retention reduces current dividends but can lead to larger future payouts, since more capital remains within the company.

In the Discounted Cash Flow (DCF) model, retained earnings serve as an internal source of financing for reinvestments. By funding growth without raising new debt or equity, they increase future free cash flows and have a direct impact on the estimated company value.

In an Asset-Based Approach, retained earnings are reflected in the equity section of the balance sheet. Each time profits are retained, reported equity rises, which in turn increases the company’s book value. Since this approach is heavily grounded in accounting values, retained earnings become a key driver: they add to the company’s substance and can significantly influence the valuation outcome.

These examples illustrate that while retained earnings are not a standalone valuation method, they affect the assumptions behind dividend policy, growth, and capital structure in all major models and thus play a critical role in valuation overall.

3. Why Are Retained Earnings Important for Investors and Analysts?

For investors and financial analysts, retained earnings show how management makes use of profits:

Positive signal: A steady increase indicates that the company can finance growth internally, which is a strong sign of financial health.

Negative signal: Negative retained earnings (accumulated losses) suggest weak profitability or dependence on external financing, raising concerns about financial stability and risk.

You’re advising FreshHarvest AG, a fast-growing food distribution company based in Germany. They operate on tight margins, high volumes, and have recently secured several new retail partners. The CFO wants to better understand how working capital decisions and seasonal dynamics impact their free cash flow profile and ultimately their valuation.

Your task is to assess how working capital evolves over the forecast period, how payment term shifts affect cash flow, and how to reflect seasonality in a dynamic forecasting model.

This case will test your analytical skills, cash flow understanding, and judgment around operational finance levers.

You’re working on a DCF valuation for CloudCore Inc., a publicly traded cloud computing company. You’ve built a standard unlevered DCF model using a WACC of 10% and based on your 5-year forecast, the Enterprise Value (EV) currently comes out to $200 million.

This set of questions is designed to help you prepare for the most common valuation topics in finance interviews. It covers the basics (like DCF, comparables, and multiples) but also includes practical scenarios that test whether you can apply these concepts in context.

Set aside about 30–35 minutes to go through everything. For each question, you’ll find a clear model answer to check your reasoning and deepen your technical knowledge.

Retained earnings are the portion of company profits that are kept instead of being paid out as dividends. Over time, they accumulate in shareholders’ equity on the balance sheet and act as an important source of internal financing. Companies rely on retained earnings to reinvest in growth, reduce debt, or build financial stability.

In valuation, retained earnings influence both dividend policy and reinvestment decisions, which directly shape models such as the Dividend Discount Model (DDM) and the Discounted Cash Flow (DCF) approach. By connecting basic accounting concepts with long-term value creation, retained earnings show how profitability translates into financial flexibility and company valuation.

For finance interviews, being able to explain retained earnings clearly demonstrates an understanding of how profits flow through the balance sheet and how they affect both short-term shareholder returns and long-term corporate value.

Let's Move On With the Next Articles:

Working Capital

Key Figures & Terms

Working capitalis an important metric that is frequently tested in investment banking interviews, especially in the context of the three financial statements (income statement, balance sheet, and cash flow statement).

It is calculated using balance sheet items and shows how much capital a company has available for its day-to-day operations after short-term liabilities have been settled.

🔎 In this article, you’ll learn:

- what net working capital is,

- how it is calculated,

- what it is used for, and

- which typical interview questions are asked about it.

Did you know that companies can raise money not only through bank loans or equity, but also through the capital market? One important way to do this is through corporate bonds. Investors lend money to a company, receive regular interest payments called coupons, and get their money back at maturity.

Besides regular corporate bonds, there is another type called High Yield Debt, also known as Junk Bonds. These bonds offer higher interest rates because they are riskier for investors. For this reason, they are often used to finance large projects such as leveraged buyouts, growth investments, or restructurings. Let us now look at how High Yield Bonds work in more detail. 🔎

In finance, the tax shield refers to the tax savings a company achieves by deducting certain expenses from its taxable income. The most common examples are interest payments on debt and depreciation of assets. These deductions reduce taxable income, which lowers the company’s tax bill. As a result, more cash flow is left over for shareholders or for reinvestment.

The idea of the tax shield is simple but powerful: by lowering taxes, companies can increase their value. That’s why the tax shield is often tested in finance interviews, especially in connection with valuation, capital structure, and leveraged buyouts (LBOs).