A letter of intent (LoI) is one of the first formal documents in an M&A deal process. It comes up after a buyer and seller have had promising early-stage discussions but nothing is on paper yet. At that point, both parties need a way to move forward together, and the M&A letter of intent provides exactly that by outlining the proposed key deal terms.

Read on to understand what goes into an LoI in M&A, whether it's legally binding, and what comes next in the deal process.

A Letter of Intent (LoI) for business acquisition is a preliminary, written agreement between a buyer and a seller that outlines the primary terms and structure of a proposed transaction. It’s more like a formal, detailed offer that opens the door for the buy-side M&A team to start the due diligence process while also keeping deal terms from drifting before the final definitive purchase agreement.

In most M&A transactions, the buyer initially drafts and presents the LoI to the sell-side M&A team. They use it to say, "Here is exactly how much we are willing to pay for your company, how we plan to structure the payment, what we need to verify, and how long we need to do it." The seller reviews it, pushes back on unfavourable terms, and both sides negotiate to reach a version they're comfortable signing.

In other scenarios, the seller’s advisors might provide a standardized LoI template and require all interested buyers to submit their bids using that exact template to make it easier to compare offers side-by-side.

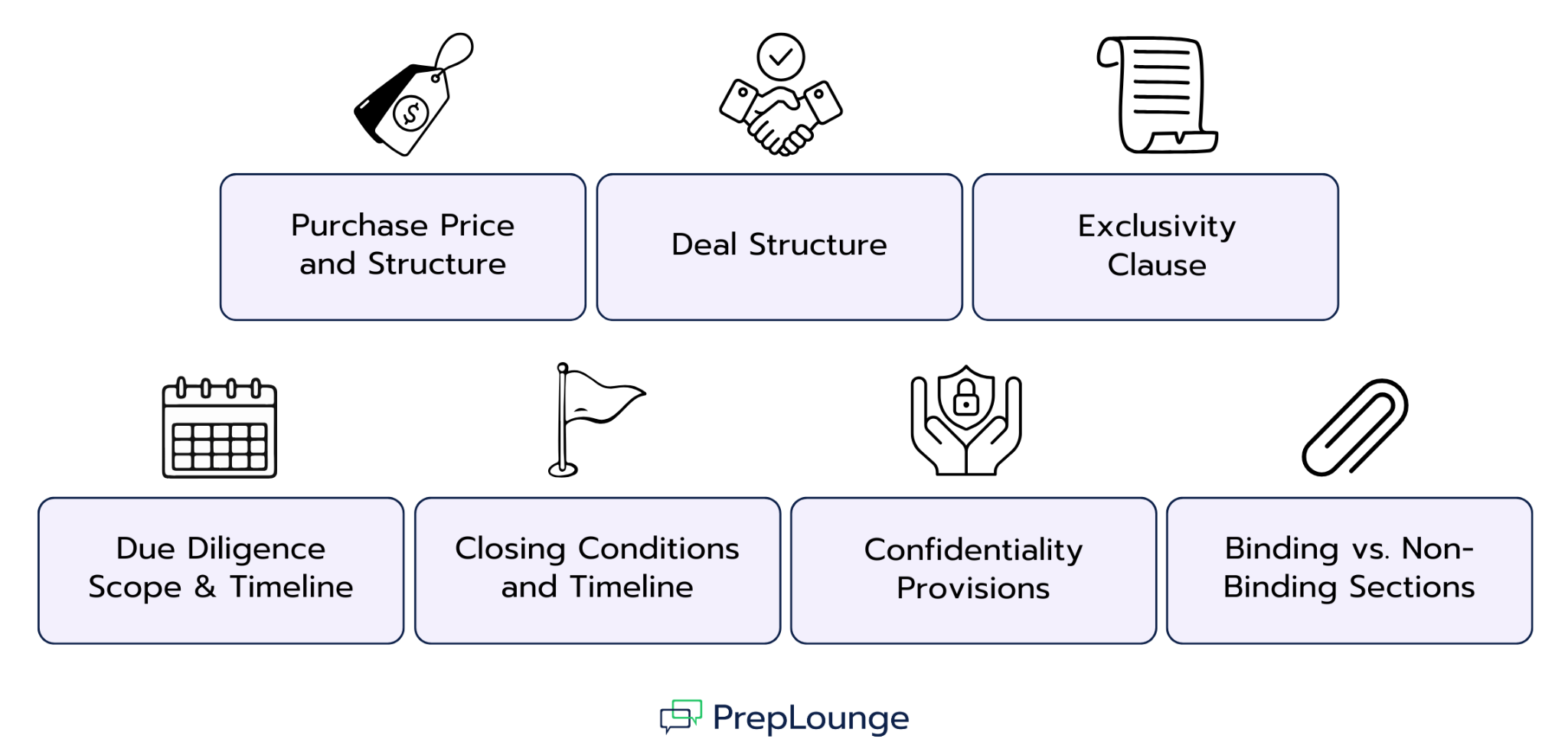

What Does a Letter of Intent Include?

As mentioned above, the main purpose of an M&A letter of intent is to outline the deal structure, and what’s included reflects that. The exact contents vary by deal size, industry, and the preferences of the parties involved. But here are the key components of a LoI for business acquisition:

Purchase Price and Structure: The proposed amount and whether it's cash, stock, earnout, or a combination

Deal Structure: Whether it's an asset purchase or a stock purchase. This has significant tax and liability implications.

Exclusivity Clause: A period during which the seller agrees not to negotiate with other buyers. It gives the buy-side enough time to perform thorough due diligence and negotiate the definitive purchase agreement without the threat of competing bidders.

Due Diligence Scope & Timeline: An outline of what the buyer intends to review (financial records, legal contracts, customer data, employee agreements) and the timeframe they have to do it.

Closing Conditions and Timeline: The target date for closing the deal and a list of any specific milestones that must be met first, such as securing third-party financing or obtaining specific regulatory approvals.

Confidentiality Provisions: Protection for sensitive information shared during negotiations.

Binding vs. Non-Binding Sections: A clear declaration of which parts are enforceable and which aren't.

Binding vs. Non-Binding - Is a Letter of Intent Legally Binding?

An LoI is mostly non-binding, but not entirely. The core commercial terms, like the price, structure, and timeline, are generally non-binding. Either party can walk away if negotiations break down or if due diligence reveals something unexpected.

However, certain clauses within the M&A letter of intent are generally binding. These include confidentiality / non-disclosure obligations, which carry legal weight. Exclusivity provisions that prevent the seller from shopping the deal to other buyers during a defined window are usually enforceable too. So is any agreed cost-sharing or breakup fee arrangement.

Role in the M&A Process - Where Does the Letter of Intent Fit?

Generally, a Letter of Intent (LoI) comes mid-stage / pre-due diligence in the M&A process. Once signed, it acts as a bridge from informal interest to a more formal commitment. A buyer won’t spend significant resources on due diligence, and a seller won’t share sensitive information, without it.

Below is an overview of the typical stages of an M&A transaction and where the LoI sits.

Preparation and Strategy

The seller gets their financial records in order and prepares marketing materials, like a Confidential Information Memorandum (CIM).

Marketing & Initial Offers (IOI)

Once materials are ready, the seller's business is marketed to potential buyers. Interested buyers submit a loose, non-binding Indication of Interest (IOI) suggesting a rough valuation range to see if they can even get in the game.

The Letter of Intent (LoI)

After reviewing the IOIs, the seller selects the best candidate(s) for deeper discussions. The buyer then submits the formal letter of intent. Once both parties negotiate the terms and sign it, the deal officially enters the exclusive zone.

Up until this signature, the seller could talk to anyone. But the seller's hands are tied by the LoI exclusivity period clause, also known as a "no-shop" clause, once signed, and the buyer's clock starts ticking.

Due Diligence

The signed letter of intent allows the buyer and their team of accountants and lawyers to conduct due diligence by accessing the seller's data room. They verify every information they need like tax return, customer contract, and employee record to make sure the business is exactly as advertised.

Definitive Agreements & Closing

If due diligence checks out, the lawyers from both sides draft the final Definitive Purchase Agreement. This binds both parties legally, money changes hands, and the deal is officially closed. The LoI is now superseded by the final contract.

How Do You Write a Letter of Intent?

If you’re wondering how to write an M&A letter of intent, the key is ensuring you include all the major components we listed earlier. Ideally, the LoI should be drafted or reviewed by a lawyer with M&A experience. But here’s how to structure those elements effectively:

1. Start With Parties and Purpose

The LoI should start with a formal business formatting of the date and address. Then open by clearly identifying the buyer and the seller, naming the target business, and stating plainly that this document represents the parties' intent to explore a transaction on the terms that follow.

2. State Valuation and Proposed Deal Terms

The next step is to state what the buyer is willing to pay and how they are going to do so. Begin with the total purchase price. Then break down the proposed deal structure (asset vs. stock) and any payment mechanisms, such as upfront cash, deferred consideration, or earnout.

3. Outline Due Diligence Process

This is where you tell the seller what the buyer wants to look at and how long they need to do it. State that the offer is contingent on a satisfactory review of their financial, legal, and operational records. Then give a reasonable timeframe, typically 30 to 90 days, to complete this investigation.

4. Distinguish Binding Vs Non-Binding Provisions

Include a paragraph that explicitly mentions which provisions are intended to be legally enforceable and which are not. For instance:

Non-Binding: The purchase price, the deal structure, and the closing conditions.

Binding: Exclusivity (no-shop clause), confidentiality, governing law, breakup fee, and the expiration date of the LoI.

5. Address Exclusivity

Add a LoI exclusivity period clause. Explicitly state that for a period of X days (normally 30 to 90 days), the seller cannot solicit, negotiate, or accept offers from other potential buyers. Be specific with the period and seller prohibitions.

If a separate NDA isn't already in place, add confidentiality agreement terms in the LoI. These establish the obligations of both parties to protect sensitive information shared during the process.

6. Close With Deadline For Acceptance

If you send an LoI, give the seller a timeline to accept it. Otherwise you may invite delays if no expiry date is set.

Who Signs a Letter of Intent?

In a standard M&A transaction, the letter of intent is signed by authorized representatives from both the sell side and buy side teams. For the buyer, that’s either the individual or an executive signing on behalf of the acquiring company. For the seller it’s the business owner or an officer representing the company being sold.

If the business has multiple owners, buyers will often insist that all major shareholders or partners sign, or at least provide written consent, to ensure a minority owner cannot swoop in later and tank the deal. Third parties like brokers, lawyers, and M&A advisors do not sign the LoI, as they are not legal parties to the actual sale.

Advantages and Disadvantages of a Letter of Intent

Like any deal tool, a letter of intent comes with genuine benefits and real limitations to both parties. Below is a quick overview.

Advantages and Disadvantages of a Letter of Intent for the Seller

Pros of a LoI for the Seller

Cons of a LoI for the Seller

Vets whether a buyer is serious or worth the time

Prevents the seller from entertaining other offers

Gets a written record of agreed-upon terms before spending money

Buyers can use due diligence to aggressively grind the price down

Reveals major deal-breakers or disagreements on price or structure early

Can make inexperienced sellers feel the deal is already done

Builds deal momentum as the buyer commits to moving forward

High risk of lost time and money if the transaction collapses

Advantages and Disadvantages of a Letter of Intent for the Seller

Pros of a LoI for the Buyer

Cons of a LoI for the Buyer

Secures exclusivity, protecting the buyer from being outbid during investigation

The seller can still walk away before the final agreement as its not a legal guarantee

Establishes a clear timeline and expectations for due diligence

Vague or inconsistent LoI language creates massive friction later

Identifies major financial or operational flaws early

High risk of lost accounting and legal fees if the deal fails

Speeds up final contracts by giving lawyers a solid framework to draft the definitive agreement

Key Takeaways

A Letter of Intent is a written document that outlines the terms of a deal including purchase price, payment structure, due diligence requirements, exclusivity and confidentiality clauses, and closing conditions. It gets buyers and sellers on the same page before either party commits significant time, money, and energy to the full deal process. Used well, it allows for negotiations, reduces misunderstanding, sets clear expectations, and creates a structured path toward closing.

An M&A letter of intent is generally not legally binding regarding the actual sale of the business. However, certain clauses, specifically confidentiality, exclusivity, responsibility for transaction expenses, and governing law, are fully legally binding on both parties.

Let's Move On With the Next Articles!

Customer Acquisition Cost (CAC)

Key Figures & Terms

Customer Acquisition Cost (CAC) is often seen as a marketing metric in business. But for finance professionals, it’s a measure of capital allocation efficiency as it reveals the average cost a business incurs to win a single new customer. This makes CAC a valuable business metric for assessing if a company’s operating model or growth strategy is sustainable in the long-term. So, it shows up in profitability analysis, financial modeling, valuation, investor reporting, and M&A due diligence.

Read on to understand how to calculate CAC, its importance, factors that affect it, and sample interview questions.

Customer lifetime value (CLV or LTV) is one of the most important business metrics. It estimates the total net revenue a company can expect from a customer over the course of their relationship. With such data, CLV helps companies identify their most valuable customers, make cash flow projections, and assess long-term business sustainability.

Read on to understand how to calculate CLV, its limitations, ways to improve it, and what interviewers are likely to ask about it.

Churn Rate: What It Is, How to Calculate It, and How to Keep It Low

Key Figures & Terms

The Churn rate is a core KPI for any subscription or recurring-revenue business. It reveals the percentage of customers or subscribers who discontinue their relationship with a business during a given period. With those numbers, a company can figure out the causes and make strategic adjustments to increase customer retention.

Read on to learn how to calculate churn rate, how it impacts revenue, what causes it, how to reduce it, and what questions interviewers ask about it.