Useful Business Analysis Tools

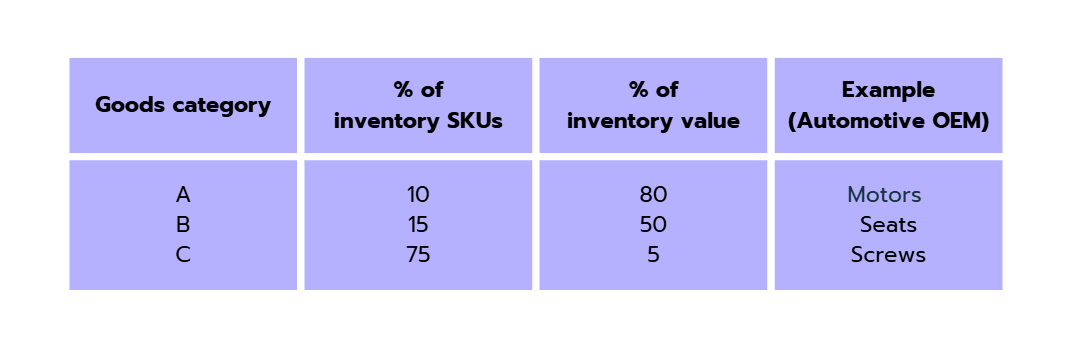

Pareto's 80-20 principle is a general rule of thumb that describes an unequal distribution between causes and effects. The principle states that 80% of overall results are driven by 20% of inputs. For example: 80% of work requires 20% effort, 80% of a project requires 20% of the time, and 80% of revenue comes from 20% of clients. When analyzing case problems, the Pareto rule can be utilized to diagnose big issues that might be caused by a much smaller problem. On the other hand, problems that seemingly look huge might result in only a small issue.