The Time Value of Money – An Intuitive and Financial Explanation

The time value of money reflects the principle that money today is worth more than the same amount in the future because it can be invested and earn interest. There are two ways to explain this concept:

- Intuitive Explanation: People prefer to have money now rather than later because it involves less risk. For example, would you rather have €100 today or in a year? Most would choose today, as future payments come with uncertainty, like inflation or the risk of default.

Financial Explanation: If you have €100 today, you could invest it at a 2% interest rate and have €102 in a year. To find the present value of €102 in one year, you divide it by 1.02, which gives you €100. This shows how future cash flows are discounted to their present value.

Calculating Net Present Value (NPV)

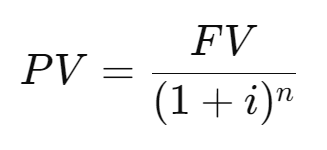

NPV is calculated as the sum of all discounted future cash flows. The present value (PV) of a single future cash flow is given by the following formula:

- PV: Present value of a future cash flow

- FV: Future value of the cash flow

- i: Discount rate or interest rate per period

- n: Number of periods between now and the future cash flow

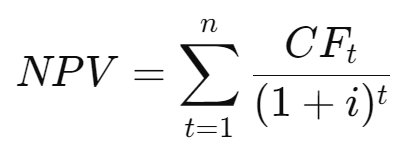

The Net Present Value (NPV) is the sum of all these present values (PVs) for the project's future cash flows:

- CF_t: Cash flow in year t

- i: Discount rate

- n: Number of periods

If the NPV is positive, the discounted cash flows exceed the initial investment, indicating the project is profitable. A negative NPV suggests that the project will result in a net loss.

Example of NPV Calculation

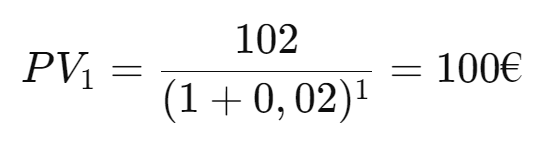

Let’s say you receive €102 in one year and €102 in two years with a discount rate of 2%. The present value of the first cash flow is:

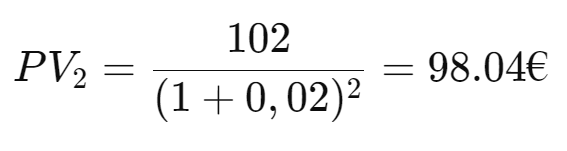

The present value of the second cash flow is:

The total NPV of this investment is the sum of the present values:

Applying the NPV in Case Interviews

In case interviews, it is unlikely that you will need to perform a complex NPV calculation, as such calculations can be time-consuming. However, there are some useful shortcuts and concepts that you can apply to argue effectively and efficiently.

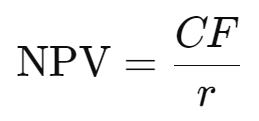

NPV for Infinite Cash Flows

For infinite cash flows (perpetuity), where a company or investment generates constant profits over an indefinite period of time, a simplified NPV formula can be used:

Here, CF stands for the constant annual cash flow and r for the discount rate.

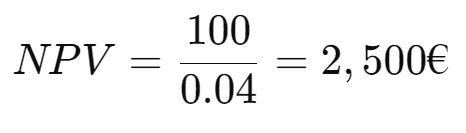

Example: A company generates € 100 per year and the discount rate is 4%:

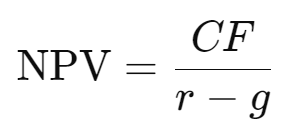

If the company grows at an annual rate of 2 %, the formula is as follows:

Where g stands for the growth rate.

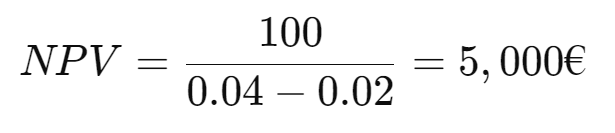

Example calculation:

💡 Prep tip: In case interviews, you don't have a calculator to hand. To calculate the simplified version of the NPV calculation in your head, you should be able to do the basic types of calculation. Use our mental math tool to brush up on your skills!