Common Terms of Business

The Blue Ocean Strategy, developed by W. Chan Kim and Renée Mauborgne in their book Blue Ocean Strategy (2005), turns traditional business thinking upside down. It focuses on tapping into undiscovered markets – the "blue oceans" – where companies can operate alone and avoid competition. The result? More growth and higher profits.In contrast, the "red ocean" refers to the already overcrowded market space where competition is fierce, and companies are constantly striving to outdo each other. This often leads to declining profits and limited growth. 🌊The Blue Ocean Strategy represents a shift away from this destructive competition towards a more constructive and creative form of market development. It encourages companies to go beyond the industry's conventional boundaries and create new markets, making competition irrelevant.

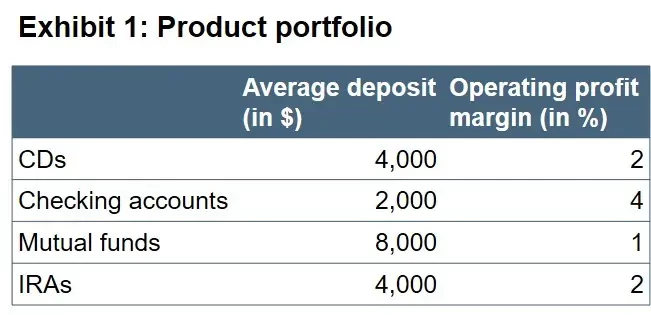

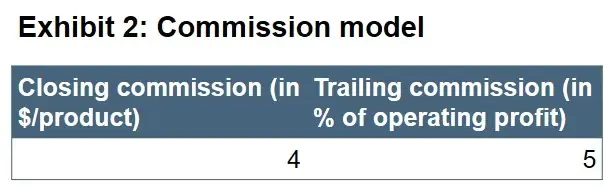

Retail Banking Profitability