Apr 10, 2025

8 min

Private Equity or Venture Capital? Find out wich finance career is right for you in this article!

If you want to succeed in the competitive interview process at a top-tier venture capital firm, thorough preparation is essential. It’s especially important to build a strong understanding of industry trends, market dynamics, and the firm you’re applying to, while also showing why you're a great fit for the team.

Solid technical knowledge of venture capital is a must and often one of the most challenging parts of the interview process.

To help you prepare effectively and know exactly what to expect, we’ve put together 21 common VC interview questions along with sample answers. You’ll also find proven tips to structure your preparation and boost your chances of landing your dream job in venture capital.

👉 Want to learn more about venture capital in general? Then check out our article “Your Guide to Starting a Career in Venture Capital.”

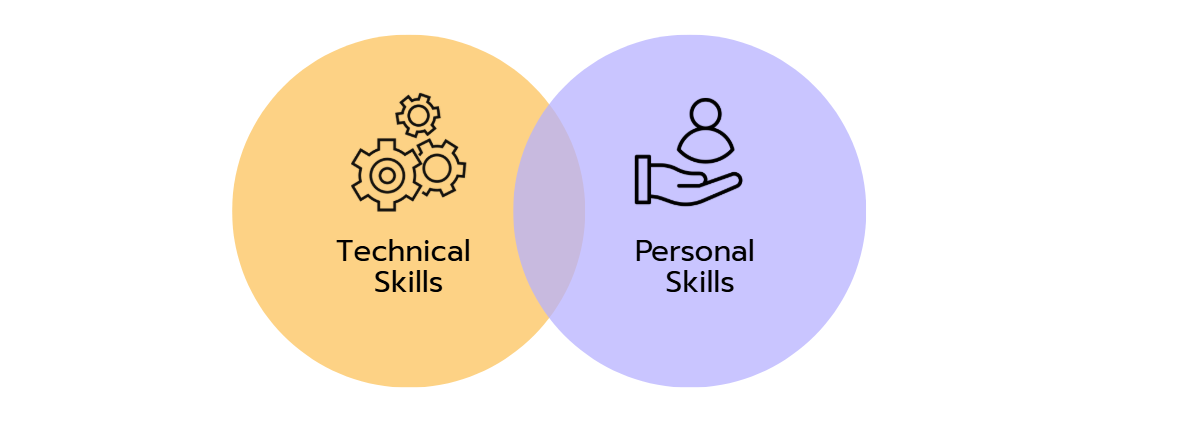

Venture capital interviews assess both your technical knowledge and your personal strengths like mindset, communication, and the ability to work in a team. In the end, it’s the mix of hard and soft skills that determines whether you’re a good fit for the firm.

Technical Skills

In the technical part of the interview, the focus is on whether you understand and can confidently apply the core principles of venture capital. You should be prepared to discuss topics like:

Personal Skills

Beyond your technical know-how, VC interviewers put a strong emphasis on your personal fit. They’re looking for traits such as:

👉 Want to boost your networking skills? Check out our article on networking in investment banking for more tips.

Here are some of the most common technical questions in VC interviews.

Q1: If you had to prioritize five key provisions in a venture capital term sheet, which would they be and why?

The interviewer wants to know whether you understand the key deal negotiation points and can differentiate between investor protections and founder incentives.

Sample answer:

"The five key provisions I would prioritize are:

Q2: How does a change in the pre-money valuation affect investor ownership compared to the post-money valuation?

This question tests your understanding of startup valuations and cap table calculations.

Sample answer:

“The pre-money valuation reflects how much a startup is worth before new capital is invested. The post-money valuation is the sum of the pre-money valuation and the investment amount, showing the company’s total value after the funding round.

What matters most to investors is how much equity they receive for their investment—and that depends directly on the pre-money valuation.

The higher the pre-money valuation, the smaller the ownership percentage investors receive for the same investment. Conversely, a lower pre-money valuation means a larger equity stake, since the company is valued more cheaply.

Sample answer:

An investor wants to invest $5 million.

Q3: In what specific situations would you advise a founder to opt for convertible debt over a SAFE or priced equity round?

For this one, the interviewer wants to see if you know the different financing instruments and can customize your advice to a startup’s context.

Sample answer:

"I would recommend convertible debt when the startup seeks immediate funding but is uncertain about its valuation. Another scenario would be when it wants to delay equity dilution until a later funding round."

Q4. How would you evaluate the health of a SaaS business that has high growth but declining net dollar retention?

Such a question will come up in VCs that deal with SaaS startups. They want to know if you can determine the health of a business by looking beyond surface metrics and identify risks beneath strong topline numbers.

Sample answer:

"This is a concerning pattern that I would look at carefully. High growth coupled with declining NDR might mean the company is acquiring customers but not keeping them or expanding them effectively.

So, I would analyze customer acquisition costs, churn rates, and cohort analysis to determine if growth is sustainable despite declining retention. For the cohort behavior, I’d want to see if the retention issue is affecting all customers or specific segments. Looking at gross retention separately from expansion revenue would help me isolate whether the problem is churn or lack of upsell.

If customer acquisition costs are steady or rising while lifetime value falls, the unit economics are deteriorating. I’d also want to look at product usage metrics and NPS scores to determine if there's a product-market fit issue or implementation/onboarding problem. A declining NDR is a leading indicator of future growth challenges, so addressing it would need to be a top priority."

Q5. How might the interests of existing investors, founders, and new investors differ when deciding between convertible notes and equity financing?

This one explores your knowledge of financing instruments and the implications for cap tables and control.

Sample answer:

"Existing investors might prefer equity for clarity on ownership and governance, while founders may favor convertible notes or SAFEs to defer valuation discussions and minimize dilution if the company grows before conversion.

New investors might push for notes if they want downside protection or equity if they want immediate influence."

Q6: What metrics would signal to you that a company has strong product-market fit even if revenue is still modest?

What the interviewer wants to see here is whether you can identify early signs of traction beyond financials.

Sample answer:

"The key metrics include high user engagement, strong retention, rapid organic growth, positive NPS, and evidence of word-of-mouth referrals. All of these show product-market fit, even if revenue is early-stage."

Q7: How would you value a pre-revenue startup?

The main concepts being tested here are early-stage valuation methodologies and risk assessment.

Sample answer:

"I’d use methods like the scorecard, Berkus, or risk factor summation. My focus would be on team quality, market size, technology, and comparable transactions, rather than financial metrics."

Q8: What is the definition of a cap table and do you know how to build them?

This question is testing your technical knowledge of equity structures and practical experience with equity modeling.

Sample answer:

"A cap table is a spreadsheet or tool that tracks the ownership stakes, equity dilution, and value of each shareholder in a company. I’m comfortable building and updating cap tables in Excel or specialized software to reflect new investments, option pools, and conversions."

Q9. Apart from comparables, multiples, and DCF, what other valuation methods do you know of?

This one evaluates your breadth of valuation knowledge and creativity in applying different frameworks.

Sample answer:

"Other methods include the venture capital method, First Chicago method, Berkus method, scorecard method, and real options analysis."

Q10. If you invest $3M in a startup at a $12M pre-money valuation, and there's a 15% option pool expansion as part of the deal, what percentage of the company will you own post-investment?

This question checks your ability to perform cap table math and understand the impact of option pools on ownership.

Sample answer:

"The post-money valuation is $15M ($12M + $3M). With a 15% option pool included, the investor owns $3M / $15M = 20%. However, if the option pool is created pre-money, the founder’s stake is diluted before the investment, and the investor still gets 20% of the post-money."

Q11. Why is IRR a preferred way of measuring performance by VC firms instead of return percentage?

Here, the interviewer wants to see if you understand why time-adjusted returns matter in fund performance.

Sample answer:

"IRR accounts for the time value of money and the timing of cash flows. This is crucial in VC where returns are realized over many years. Return percentage ignores when returns are generated."

Q12: What performance metrics would you present to limited partners when raising a second fund if your first fund is only 3 years into its investment period?

Here, your knowledge of VC fund operations, LP relationships, and fund management are put to test.

Sample answer:

"I’d present metrics like DPI (distributions to paid-in), TVPI (total value to paid-in), IRR, portfolio company progress, markups, and unrealized value, progress toward exit strategies, along with qualitative updates on key investments."

Q13: Revenue and profit, which do investors value more?

With this question, the interviewer wants to see if you know how investment priorities change across different stages and business models

Sample answer:

"Early-stage investors usually prioritize revenue growth and market traction over profit, as scale and market share are critical. Later-stage investors focus more on profitability and sustainable margins."

Q14: What specific expense patterns in a startup's P&L would concern you, and what might they indicate about the business?

The interviewer is checking if you can spot financial red flags that may indicate deeper business issues.

Sample answer:

"Excessive burn relative to revenue, high customer acquisition costs without improving LTV, or uncontrolled headcount growth could signal unsustainable operations or lack of product-market fit."

Q15: How do valuation methodologies typically evolve from seed stage through Series C and beyond?

What’s being tested here is your understanding of how valuation methods adapt as companies scale.

Sample answer:

"At seed, qualitative and heuristic methods (scorecard, Berkus) are common. Series A/B use comparables and the venture capital method. By Series C+, DCF and public market comps become more relevant as financials mature.

Generally, early-stage valuations focus on potential and market size, while later stages incorporate revenue and profit metrics. In later stages there’s increased scrutiny on financials and scalability."

Q16: How does a change in the option pool allocation affect the relationship between pre-money and post-money valuations?

For this one, you want to demonstrate your knowledge of the mechanics of dilution, investment terminology, and negotiation tactics.

Sample answer:

"Increasing the option pool pre-money dilutes founders and early investors. As such, it lowers the real pre-money valuation and benefits new investors by giving them a larger share for the same investment."

Q17: How do the rights of SAFE holders compare to convertible note holders in downside scenarios or in the case of an early acquisition?

This question tests your grasp of the legal and practical differences between these instruments in adverse outcomes.

Sample answer:

“SAFEs (Simple Agreements for Future Equity) and convertible notes are both tools that allow investors to fund startups early, before a formal valuation takes place. However, their treatment in negative scenarios like insolvency or an early exit differs significantly.

Convertible notes are typically considered debt instruments. This means investors often have the right to be repaid and are prioritized over shareholders in the event of bankruptcy. In the case of an early sale of the company – before the note converts into equity – investors may also have the option to either get their money back or convert into shares at a pre-agreed price. As a result, convertible notes provide stronger downside protection in unexpected situations.

SAFE holders, on the other hand, usually have no repayment rights because SAFEs are considered equity-like agreements. Conversion into equity typically only happens upon a specific triggering event, such as a new funding round. If an exit or insolvency occurs before such an event, SAFE investors are in a weaker position, often receiving nothing and ranking below other creditors in legal terms.

In summary, convertible notes offer more security in downside scenarios because they are formally classified as debt. SAFEs are simpler and more flexible for startups but offer less protection for investors in crisis situations.”

Q18: Which term sheet provisions would you be willing to compromise on, and which would be non-negotiable when investing in a competitive deal?

Here, the interviewer wants to see your sense of deal priorities and where you draw the line on risk.

Sample answer:

"I would be open to negotiating terms like board observer rights or minor anti-dilution terms. However, non-negotiables would include liquidation preference, major protective provisions, and clear vesting schedules to align interests."

Q19: How would you assess whether a deep tech startup has an appropriate level of IP protection before their Series A round?

This question checks whether you understand the strategic importance of IP in deep tech and can evaluate its sufficiency before significant scaling.

Sample answer:

"I’d review patent filings, freedom-to-operate analysis, inventor assignments, and competitive IP landscapes to ensure that core technology is protected and there are no obvious infringement risks."

Q20. Explain how you would calculate the post-money valuation of a startup raising $5M at a $20M pre-money valuation with an option pool expansion.

This question tests your understanding of cap table mechanics and dilution effects, which are fundamental to structuring equity deals.

Sample answer:

"The post-money valuation equals pre-money valuation plus new capital invested, so it's $20M + $5M = $25M. However, with an option pool expansion, we need to account for additional dilution. If the option pool expands by, say, 5% post-money, we'd create new shares equivalent to 5% of the post-money cap table.

This dilutes existing shareholders but not the new investors since this expansion was factored into the pre-money valuation. The post-money remains $25M, but ownership percentages shift, with the new investor getting $5M/$25M = 20% of the company."

Q21: How would you structure liquidation preferences in a term sheet, and what are the trade-offs between different structures?

This question tests your knowledge of term sheet structures and how investment terms impact founder and investor outcomes.

Sample answer:

"I would approach liquidation preferences based on stage, market conditions, and company quality. Standard structures include: 1x non-participating (investor gets investment back or converts to common), 1x participating (gets investment back plus pro-rata share of remaining proceeds), or participating with a cap (typically 2-3x).

The key trade-off is downside protection versus founder alignment. Non-participating preferences align investor and founder interests in pursuing large outcomes, while participating preferences create misalignment at certain exit values. In today's market, I'd typically recommend 1x non-participating for most Series A/B deals to maintain founder motivation while providing reasonable investor protection."

To pass VC interviews, prepare by doing self study, practice with mock interviews, and work with expert interview coaches. Here’s what you need to know about each of these tips.

Do Self Study.

Take some time to study how venture capital works. Generally, venture capitalists have three main tasks including selecting startups to invest in, assisting them after the investment, and raising capital for the fund. Understand how they go about each of those generally and at a firm level.

Besides technical questions, practice answering other types of common questions in venture capital such as:

👉 In our Case Library, you’ll find examples of technical interview questions and practice cases.

Practice with Mock Interviews.

Doing mock interviews helps to articulate what you have learned and develop confidence. So, organize several mock interviews with peers and improve based on the feedback they provide. For each mock interview, take it as seriously as the actual one to get the most out of it.

👉 Check out our Meeting Board and connect with like-minded people to practice together.

Hire an Experienced Interview Coach.

After doing mock interviews, take it to the next level with an interview coach. If there’s anything you’ve missed so far, you can be sure that a good coach will spot it and provide personalized feedback.

Working with a professional and experienced coach is like doing the VC interview itself but with a chance to improve. So, it increases your chances of landing your dream job at a reputable VC firm.

👉 Check out our Coach Overview to find the right experts who can take your interview prep to the next level.

You will most likely encounter technical questions in VC interviews. These will mostly test your knowledge of cap tables, key metrics in the industry, accounting, valuation, different types of funding, and due diligence in startup selection.

Prepare thoroughly through self study, mock interviews, and sessions with interview coaches to maximize your chances of landing the job. Read about the firm, understand their portfolio, stay updated on the markets, and develop the ability to spot trends. Once you do all these, you should be ready to ace the process. Best of luck!