Types of Cases

Pricing plays a crucial role in a company's profitability as it directly contributes to it. For this reason, establishing optimal prices for products or services is of great importance. Business consultants therefore assist their clients in developing pricing strategies.A case study on pricing is an analysis focusing on the pricing of a product or service. It can stand alone or be part of a broader case, such as entering a new market.

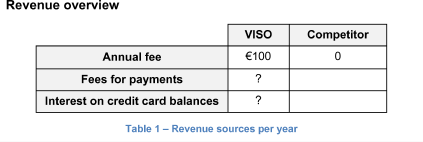

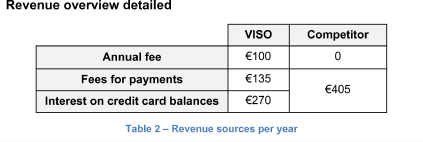

VISO

i